Click here to see the rankings

The 25th annual SDM 100, which looks at the 2014 financial performance of the 100 largest security companies, bore only slight changes year-over-year. SDM 100 companies, which earn their revenues from the sale/installation, leasing, service, hosting and monitoring of electronic security systems, collectively grew their recurring monthly revenue (RMR) by 3.8 percent in 2014 to reach $670 million. This followed a 3.3 percent hike in 2013.

“2014 was one of the best bounce-back years since the recession. Sales were stronger in virtually all categories versus 2013,” notes Beltsville, Md.-based ASG Security, ranked No. 10. “We would characterize the market as better than average. Security systems sales were driven considerably by greater awareness and demand for connected home services. In the commercial sector, there was stronger spending in private and public projects across ASG’s geographies.”

ASG Security recorded $10.02 million RMR, a 14.5 percent increase.

Approximately nine of every 10 SDM 100 companies grew their RMR during 2014. Several dealers cited the increased demand for connected home products — along with the interactive services that control them — as the reason for growth in their residential base.

However, the increasing level of competition and cost-cutting pressure in the residential market is negatively impacting businesses — primarily the smaller-sized SDM 100 dealers.

No. 9-ranked Guardian Protection Services experienced “significant competition” in the residential market, fighting through on several fronts including adding new dealer partners to its authorized dealer program. “In an effort to increase market penetration and combat this competition, we remained committed to developing and expanding an array of sustainable lead-generation programs. Our new construction channel continued to perform well in 2014 as the number of builder partners increased from the prior year and mortgage rates remained favorable,” Guardian relates. The company grew RMR by 12.3 percent in 2014, ending at $12.9 million.

Protection 1, ranked No. 6, says that although it has seen a decrease in television advertising by new entrants in the residential market, overall it still remains at a more elevated level than in prior years. “While this does not seem to be translating into market share growth, it is continuing to educate customers and bringing innovation and greater awareness. Existing customers seem more interested in upgrades than they have in previous years,” the company notes.

Although several dealers termed their residential performance “average,” “weak” and even “dismal,” Security Force Inc. had the opposite, experiencing the highest level of growth in its home technologies department in the company’s history. With a 41 percent increase in RMR last year, Security Force moved up from No. 57 to No. 46 on the SDM 100.

Companies that weighed in on the active market segments seem to agree that business in commercial markets outpaced residential. Some of the lucrative areas noted by the dealers were national accounts, education, freight/transportation, energy, healthcare, warehousing, corporate office space, and — a newer opportunity — medical marijuana, noted by Sonitrol Pacific, No. 40.

“Tenant build-outs with our large property management and developers is up, showing occupancy rates are increasing,” says SMG Security Systems Inc., ranked for the first time on the SDM 100 with RMR of $390,339.

The fire protection market also provided generous sales and service opportunities in 2014, as did upgrades from analog to IP technology in video surveillance systems.

“The market vacillated between steady and declining performance in 2014,” says Supreme Security Systems Inc., which experienced a very slight drop, less than 1 percent, in RMR year over year. “Residential was generally down the entire year while commercial exhibited sine wave activity.”

Security Equipment Inc. feels that “end users are embracing systems integration on a much larger scale,” a factor that contributed to the company’s $14.3 sales volume in the non-residential market last year.

A positive force in some of the dealers’ results last year was an active construction market. This affected both residential and commercial sales.

“The new construction market advances and loosening of the budget purse strings in the commercial arena contributed to an overall increase year over year,” comments Ackerman Security Systems. Ackerman increased its RMR last year by 16.5 percent to $3.1 million.

Post Alarm Systems also benefited from gains in the construction market, as well as from an increased level of crimes in its operating territory. “Building market increased and with that our sales increased. Crime rate went way up which increased security sales,” the company notes.

Considering the technologies that had an impact on sales, video-based services continue to dominate — although one dealer mentioned weaker sales due to outside competition. “Fire, access and security were strong. CCTV was weak for us as we have seen technology companies doing more of this,” says Habitec Security, which grew RMR by 2.5 percent.

For the majority, however, video surveillance both as a product and a service continues to proffer sales. Says Protection 1: “As it relates to the commercial and integrated systems business, we continue to see more and more interest for IP-based services, including video monitoring and managed services. Video verification and remote viewing, and remote video access via the cloud are of great interest to businesses as a way to reduce false alarms, increase speed of police response, replace costly guards and enhance business operations.”

This 25th annual edition of the SDM 100 marks a time of solid growth, especially considering the Great Recession in the not-too-distant past. It also marks a time of great change and tension among security dealers. Security is a significant concern of both homeowners and business leaders, which continues to drive sales; but businesses in other industries are faltering, and they see security as a way to boost their revenues, which puts increased pressure on security professionals.

“For the last several years we have had strong performance, so for us the market remains strong; but we have seen an increase in competition,” says Bates Security LLC / Sonitrol of Lexington.

For Bates Security and others, they have the advantage of very strong support from established vendors, and years of professional installation/service and monitoring experience — leading the industry to have great confidence in its ability to prevail over such challenges.

|

|

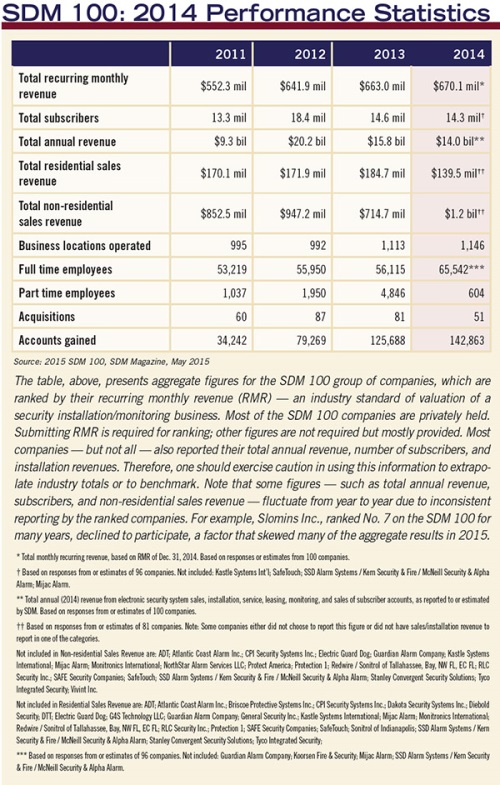

The table, above, presents aggregate figures for the SDM 100 group of companies, which are ranked by their recurring monthly revenue (RMR) — an industry standard of valuation of a security installation/monitoring business. Most of the SDM 100 companies are privately held. Submitting RMR is required for ranking; other figures are not required but mostly provided. Most companies — but not all — also reported their total annual revenue, number of subscribers, and installation revenues. Therefore, one should exercise caution in using this information to extrapolate industry totals or to benchmark. Note that some figures — such as total annual revenue, subscribers, and non-residential sales revenue — fluctuate from year to year due to inconsistent reporting by the ranked companies. For example, Slomins Inc., ranked No. 7 on the SDM 100 for many years, declined to participate, a factor that skewed many of the aggregate results in 2015. |

Key to Using the SDM 100

The 2015 SDM 100 ranks U.S. companies that provide electronic security systems and services to both residential and non-residential customers. This ranking is based on information provided to or, in few cases, estimated by SDM. Ranked companies were asked to submit an audited or reviewed financial statement, or a copy of their income tax return.

The main table, which begins on this page, ranks 100 companies by their recurring monthly revenue (RMR) of December 31, 2014. The company with the highest RMR is ranked as No. 1, and so on. For each of the 100 companies, the following information is provided, from left to right:

• Current year rank, which is based on December 31, 2014, RMR.

• Prior year rank.

• Company name, as used in the marketplace, and headquarters location.

• Amount of RMR billed on December 31, 2014.

• Percentage of RMR increase/decrease compared with December 31, 2013.

• Number of subscribers (recurring-billable customers) at year-end 2014.

• Amount of sales revenue from residential system installations in 2014.

• Amount of sales revenue from non-residential system installations in 2014.

• Total gross revenue in millions of dollars. This number represents total revenue in calendar-year or (the company’s) fiscal-year 2014 from security system sales/installation, service, leasing, and monitoring.

• Number of full-time employees.

• Number of business locations, including headquarters.

Note: An e following the figure indicates it is an SDM estimate.

To find a company by name, use the alphabetical index on page 82.

How to Purchase the SDM 100 Directory

Wouldn’t it be useful to have more information about each of the 100 companies ranked here? The 2015 SDM 100 Directory includes contact names, mailing addresses, telephone numbers, website URLs, branch office locations, product buyer names, installation data, revenue sources, and more. The SDM 100 Directory comes in Microsoft Excel format. To order the SDM 100 Directory, contact Heidi Fusaro at (630) 518-5470 or by e-mail to fusaroh@bnpmedia.com.

SDM 100: Its Purpose & Approach

The SDM 100 has been published since 1991. Its primary objective is to measure consumer dollars gained by alarm companies, in order to present an account of the size of the market captured by the 100 largest security providers. SDM 100 firms are ranked by their recurring monthly revenue. RMR is the revenue associated with the contractual agreement between a security company and its subscriber — derived from customer billing for services such as monitoring, contracted service/system maintenance, security-as-a-service/managed solutions, and leasing of security systems — and is typically the basis for valuation of a security company. RMR is the language of security company executives and is meaningful in comparative analysis among industry peers. Of the 100 security dealers ranked, 38 of them earned more than $1 million in RMR in 2014.

MORE INSIDE & ONLINE 25th Anniversary

This is a momentous year for SDM, as we celebrate the 25th anniversary of the SDM 100, a gold standard in the security industry today. It is a time to reflect on how the SDM 100 got started, how it changed and evolved, and its usefulness to the industry at large as well as those who observe, analyze and fund the security industry.

Readers will enjoy reminiscing through the article, “Looking Back on 25 Years of SDM 100 Reports,” on page 59 in this issue. It presents a historical perspective of the report and a specially designed infographic showing some of the first companies ever ranked.

In addition, all 25 editions of the SDM 100 from 1991 to 2015 (in PDF format) are available online at: www.SDMmag.com/25thSDM100.

SDM is proud of the positive impact that the SDM 100 has made on the security alarm industry. At the base of that pride is our gratitude to the companies who made it possible through their cooperation in sharing performance metrics.