For What Its Worth

Right now is one of the best times to sell an alarm company that the industry has seen in recent years. After a period of declining values in the early part of this decade, average selling prices have picked up significantly. Alarm companies, which are typically valued in multiples of their recurring monthly revenues (RMR), commanded multiples in the range of 34.4 to 45.5 in 2005, according to estimates from Barnes Associates, an investment banking firm that specializes in the security industry. Although that’s less than what was seen in 1999, when the largest companies were sold at multiples above 50, it’s an improvement from 2003, when values bottomed out at 28.9 to 36, depending on the size of the company.

More importantly, many industry observers believe today’s selling prices more accurately reflect the true value of a company than during either the boom or bust years.

“As most players in the industry remember, there was a large correction, which occurred when the last wave of big buyers retreated from the market,†notes Barnes Associates founder Michael Barnes. “The withdrawal was the result of both larger forces affecting all businesses and the poor results that these buyers actually realized from the acquisitions relative to the prices they paid. These results have been analyzed – some would say forgotten — and support for the industry and players who want to grow through acquisition has resumed.â€

Another factor that has caused values to rise is simple supply and demand. “There’s increased demand on the part of buyers to gain greater mass and there’s a diminishing supply of alarm companies to be bought,†notes Ron Davis, managing partner for GraybeardsRus of Long Grove, Ill., a firm that works with sellers of alarm companies in evaluating exit opportunities.

The number of security M&A transactions reached an all-time high in the first quarter of this year, according to “Q1 Security Industry Review,†published by USBX. The market for security technology companies is now in full swing, as high-growth market segments are showing signs of development, the report states.

Michael Jones, president of ProFinance Associates Inc., a San Diego-based investment banking firm that specializes in the alarm industry, echoes those comments. “There are more buyers with more access to capital today than two or three years ago,†Jones emphasizes. “That creates competition and multiple bidders, and attractive companies are appropriately bid up.â€

One thing hasn’t changed much over time, however. Larger companies continue to command higher prices than smaller ones. “It takes effort to absorb a company,†Davis notes. “Also, buying a larger company provides greater mass and penetration, and that’s what every buyer is looking for.â€

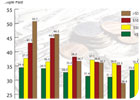

Barnes Associates estimates that the average multiple for companies with RMR of less than $50,000 was 34.4 in 2005, while companies with $50,000 to $100,000 RMR were sold at an average multiple of 36.1 and companies with $100,000 to $500,000 were sold at a 37.2 average multiple. For the largest companies with recurring monthly revenues above $500,000, Barnes estimates that the multiple for 2005 was 45.5.

This chart illustrates the average valuations of alarm companies, based on a multiple of recurring monthly revenue (RMR) paid to the seller. The averages for each year – from 1999 through 2005 (estimated) – are separated into categories based on the RMR size of the company, beginning with businesses with less than $50,000 in RMR and ending with businesses with more than $500,000 in RMR. The information was first presented by Michael Barnes as part of an Industry and Market Overview, at the Barnes Buchanan Mallon Conference in February 2006.

MOVING FORWARD

Although many industry buyers and sellers have learned and moved on from the price inflation and subsequent disillusionment experienced in the first half of this decade, the excesses of that period have had one long-lasting effect. Companies that are up for sale are scrutinized more closely than ever.The close scrutiny that today’s transactions receive seems to be having a stabilizing effect on the industry.

Barnes cautions, that if major players such as ADT or Protection One do not resume buying or if rising interest rates cause capital to begin to dry up, values could begin to decline.

Sidebar: Average Valuations of Alarm Companies in 2005

- Size of company

- Multiple of RMR

- Less than $50,000 RMR

- 34.4

- $50,000 to $100,000 RMR

- 36.1

- $100,000 to $500,000 RMR

- 37.2

- Greater than $500,000 RMR

- 45.5

Source: Barnes Associates, St. Louis, Mo.

Sidebar: 7 Tips for Getting the Best Deal for Your Alarm Company

- Make sure you have signed contracts for all of your customers and that your contract has been reviewed by an attorney familiar with the alarm industry. According to Tony Smith, president of Security Finance Associates Inc., Pasadena, Calif., contracts are “the most important thing†in determining the value of an alarm company.

- Document your company’s attrition rate, or the percentage of customers who leave the company each year. “A good level of attrition is below 12 percent,†notes John Mack, CEO of USBX Advisory Services of Los Angeles, an investment banking firm that does a lot of work with security companies. “Very good would be below 8 percent. The zone of concern is between 12 percent and 14 percent, and above 14 percent is a problem.â€

- Demonstrate that you have excellent customer service. If you have mostly affluent customers but a significant number leave each year, potential buyers may assume that poor customer service is to blame.

- Standardize on a limited number of alarm or fire panels. The easier it is to manage the equipment that a company has deployed, the easier it will be for the purchaser to absorb that company.

- A strong management team can get the company where it needs to be — and may even strengthen the deal. If the purchaser is buying your company as a means of entering a particular geographic market, the management team could be particularly important, as the buyer will want to retain key performers. Even if the purchasing company is simply expanding within a market in which it already operates, management is likely to retain some technicians and service personnel. “The buyer usually wants at least a few people coming with the deal who are familiar with the account base,†Smith notes.

- Factor in the effect of post-closing adjustments. The amount of money the seller ultimately ends up with depends not only on the selling price, but also on any post-closing adjustments agreed to by the buyer and seller. Michael Barnes, founder of Barnes Associates, offers a hypothetical example. “One deal may trade at a 38-multiple of the RMR but have post-closing adjustment provisions that will reduce the price for every dollar of RMR attrition that occurs over the six months following the transaction,†he says. “The same deal may trade at 36 times RMR without any post-closing attrition adjustment terms and actually yield the seller more money.â€

- Make sure your company is set up as a subchapter S corporation, rather than a C corporation. Buyers generally prefer to buy only the assets of a company, rather than the company itself, because in so doing, they avoid assuming liability for installations made by the original owner. But, as Eric Pritchard, a partner in Philadelphia-based law firm Kleinbard, Bell & Brecker, explains, the sale of assets of a C corporation subjects the seller to double-level taxation. “If you sell the assets in a C corporation, you pay federal income tax on the capital gains involved with the sale of assets to the buyer and the shareholders pay income taxes again on the distribution of the net proceeds to the shareholders.†With the sale of assets of a subchapter S corporation, in contrast, he says, “you only pay capital gains on the sale to the shareholders.â€

Pritchard notes that if a company is set up as a C corporation, it is possible to convert it to a subchapter S corporation, but the process takes about 10 years. The benefits could be worth the wait, though, particularly now that the rules about subchapter S corporations have changed, making them even more attractive.

“Previously, subchapter S corporations were limited in the number of shareholders you could have,†notes Mitch Reitman, principal of S.I.C. Consulting of Fort Worth, Texas, a firm that provides accounting and financial services to alarm companies. “Now you can have up to 100 and all the members of a family are considered one shareholder — even grandfathers and grandsons.â€

Another positive change is that non-voting shares of stock can now be issued in subchapter S corporations, enabling owners to retain control of the company and also reward valuable employees with shares of stock, Reitman says.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!