State of the Market: Access Control 2016

It was a very good year for access control, with most reporting double-digit growth. But market forces for change are definitely in the wind, such as unification, big data, cybersecurity and so much more.

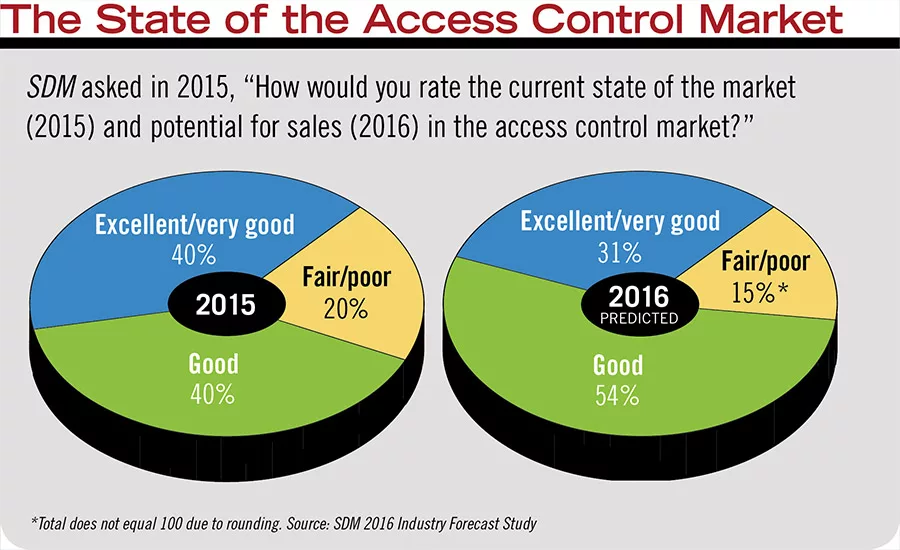

A whopping 80 percent of respondents said the access control market was “good” or “excellent” in 2015 and even more — 85 percent — think it will be at least as good in 2016.

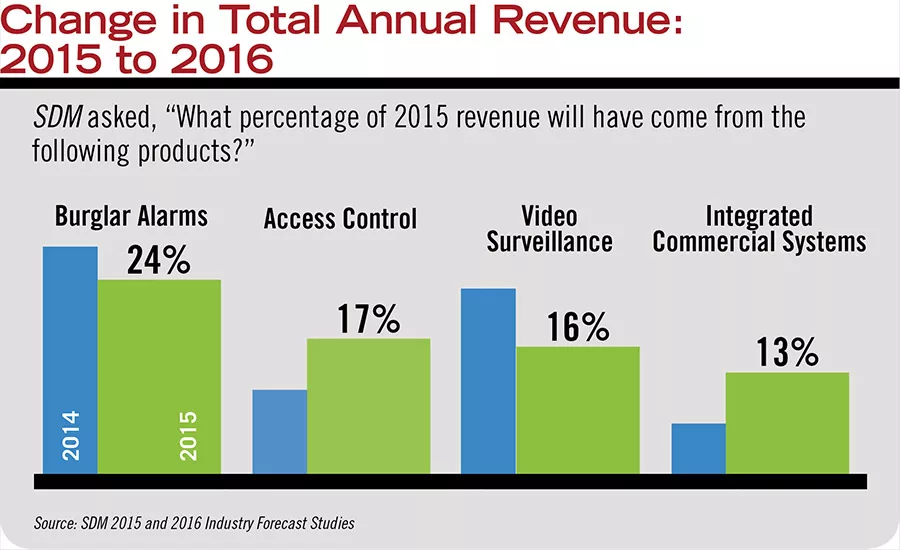

Both access control and integrated systems increased in share of revenue reported in 2015.

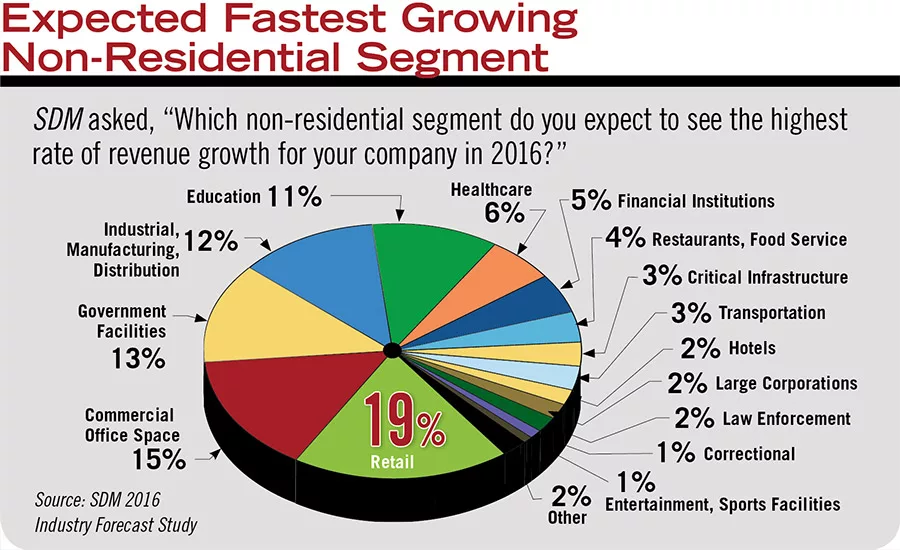

Retail, commercial office space and government facilities top the list of expected fastest growing markets in 2016.

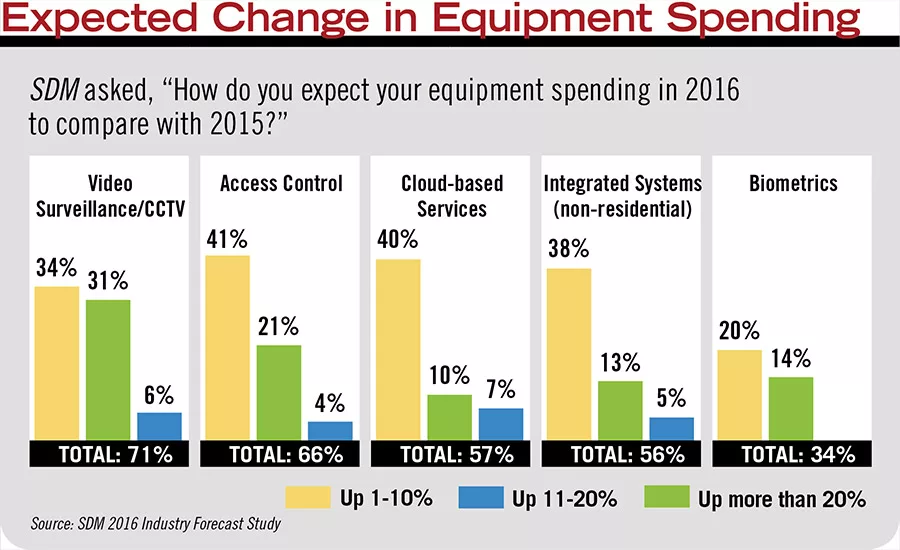

Some take-aways here are that access control spending will be high next year, cloud-based services (including access control and other SaaS) rose sharply over 2015 (it was 39 percent total last year), and biometrics rose modestly (from 29 percent total last year).

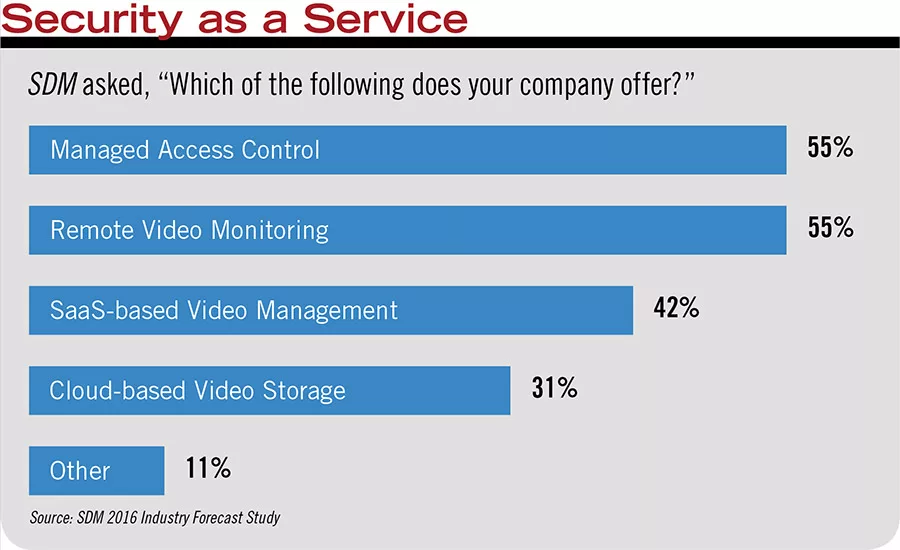

Managed access control is tied with remote video monitoring as the most common service-based offering from SDM’s subscribers participating in a study.

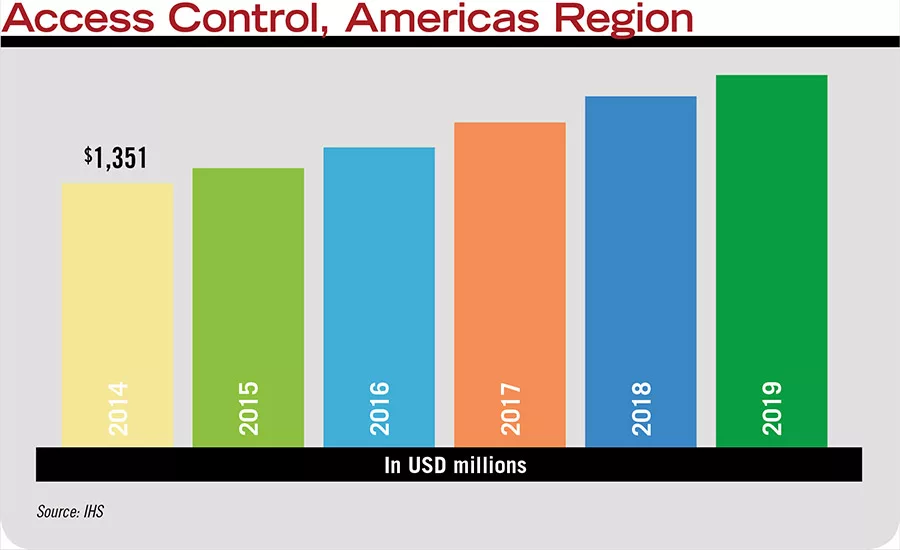

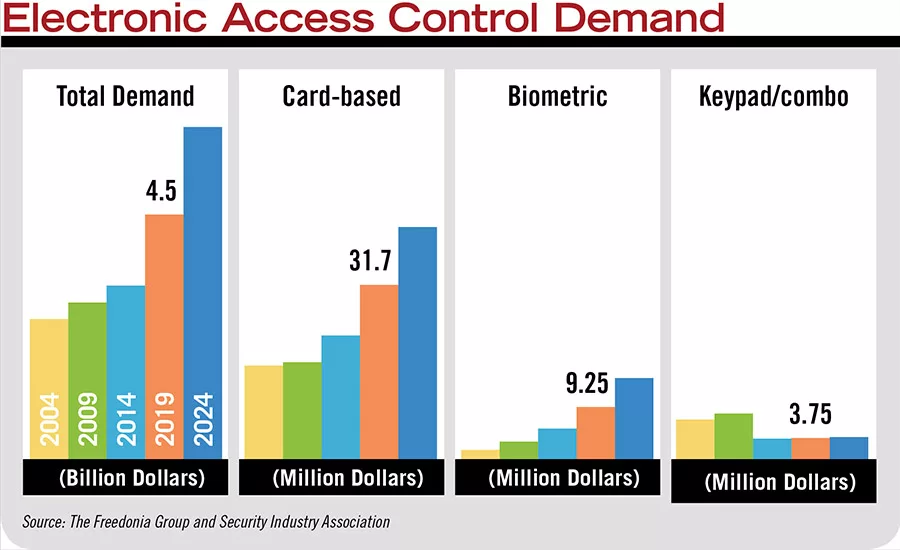

The U.S. access control market topped $1 billion for the first time in 2015 and is predicted to grow to nearly $2 billion by 2020.

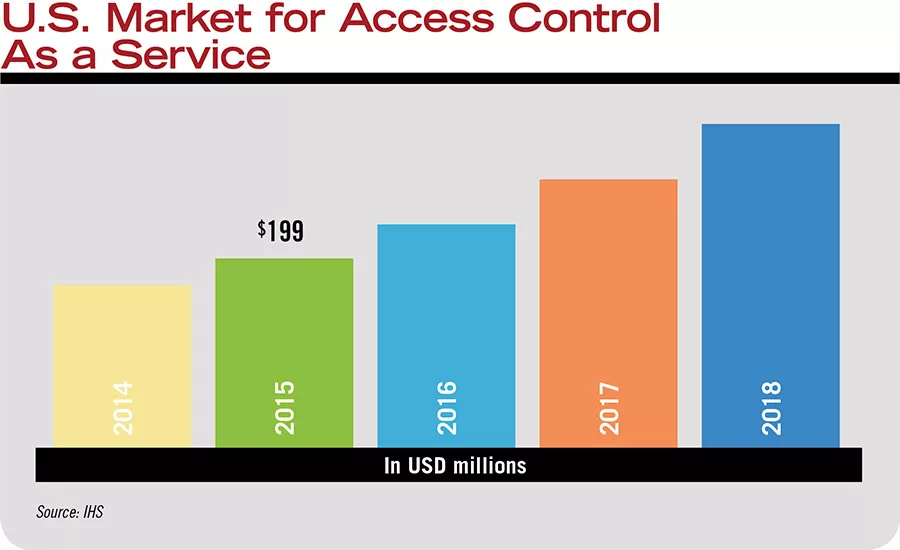

The U.S. market for access control as a service is predicted to rise sharply through 2018, more than doubling in revenue.

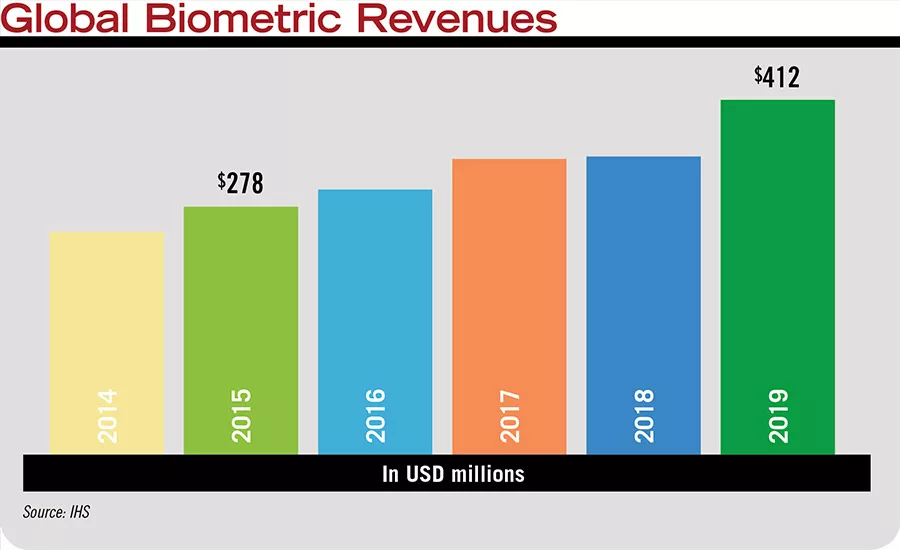

The worldwide biometric market is predicted to grow to more than $400 million by 2020.

A study on the electronic security products conducted last fall by The Freedonia Group in conjunction with SIA found in 2014 that card-based access systems accounted for 71 percent of demand and are expected to continue that demand going forward. Sales of biometrics held 18 percent of demand in that year and are expected to see faster gains; and keypad and combination devices are expected to decline.

Are Biometrics Finally Going Mainstream?

The Disruptive Face of Competition

Are Biometrics Finally Going Mainstream?

Biometrics have had a recent upswing in popularity that, although they haven’t pulled out of the “niche” category quite yet, is definitely something to watch.

“Biometrics are still considered an emerging sector, but we are experiencing rapid market adoption and increased velocity of market deployments,” says Anthony Antolino, chief marketing and business development officer, EyeLock, New York, N.Y. “When combined with strong market research from the CIO community, the long-term outlook is impressive by any measure.”

Particularly as more and more people start to focus on the gaps in cybersecurity and identity fraud, they are starting to look at biometrics with fresh interest, says Mohammed Murad, vice president of global business development and sales, Iris ID Systems Inc., Cranbury, N.J. “We started out providing technology for … back office IT protection. Now we have moved to the front office as customers have realized the technology works well and is non-contact.

“Integration points have also become easier, which is always key to getting mainstream applications to adopt. We are plug and play. We are building a product that can replace a card reader, work with a card reader or have a card reader built into it.”

In fact many mainstream access control manufacturers have started offering OEM relationships or partnerships with a host of biometric solutions.

“We are working with all of them,” Murad says. “Our technology has been integrated with almost every single access provider available today.”

Keri’s Dennis Geiszler says his company will soon be introducing its own private labelled biometric reader. “Biometrics is breaking into the mainstream a little more and it is an opportunity for us.”

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

Another reason biometrics may be surging of late is a renaissance in the technology itself.

“Every year for the last 25 years biometrics was going to take over access control,” recalls Gary Staley, national sales director/founding partner, RS2 Technology, Munster, Ind. “It is finally doing well because the product got better, and a lot faster. I have been around for 30 years and I just saw the first [biometric] technology that truly impressed me. It has finally gotten to the point where processing speeds and times are fast enough to do it with face only or finger only as opposed to card first.”

Over the last year there has been a dramatic shift toward contactless and frictionless options like the Morpho Wave fingerprint reader or Stone Lock facial recognition, says Tyco’s Jason Ouellette. “The market really likes frictionless. It likes the notion of having confirmation of who you are without having to think about it as you approach the door. Usability and convenience really sells.”

OSS’s Jim Coleman says convenience is definitely making a difference in client interest. “In the past every so often we would have projects where the demand for higher security required biometrics. But what we are seeing now is clients that are interested in using biometrics not just for security but for convenience. The cost is still high and until it comes down more I don’t think it will become too widespread. But more people like that convenience and are willing to pay a premium for it. And it is way cool.”

Research firm IHS backs up the empirical evidence that biometrics are on the rise. The company predicts global biometric revenues will rise from $278 million in 2015 to more than $400 million in 2019. (See chart, this page.) SDM’s own research shows that more than one-third of respondents plan on increasing their spending on biometric products in 2016, including 14 percent who predict increasing spending by more than 10 percent.

“What is interesting here is that as biometrics has started to become more accurate, with faster throughput and the price has started to go down it is starting to meet end users’ expectations,” says IHS’s Alexander Derricott. “It is starting to come into its own…. We are looking at an overall biometric market that is expected to grow about 10 percent over the next few years globally.”

Murad also credits the smartphone industry with making biometrics more mainstream in the past couple of years. “Since fingerprints have been included in mobile devices people are now starting to think, ‘How can I make this work in my workplace?’ It opens up a whole new conversation.”

Antolino agrees. “The proliferation of biometrics on smartphones, largely led by Apple, has helped take biometrics out of the shadows and into the mainstream consumer technology. As a result, value chain stakeholders realize they need to assess all biometrics to determine which is relevant to their case and meets their usability, security and cost guidelines.”

Canadian integrator Marc-Andre Bergeron of Marcomm Systems Group says biometrics has become a trend. “Whereas four or five years ago they were not part of an overall strategy, we are now seeing them being integrated by the powers that be right into the software so you can actually deploy a proper solution. It’s trendy. You see it on CSI.”

Overall the picture for biometrics in the near term looks rosy. “People lost a bit of trust in biometrics for a little while but products now are far better,” Derricott says. “The price premium is going down, they are accurate and a good proposition, especially if you are looking for a system that doesn’t require you to get something out of your pocket. Yes, there are issues to be solved, but everyone I have spoken to has a fairly positive outlook on how this will develop. People are talking about it.”

While it may be a great time to be in the access control market, it is also a challenging one. Competition is changing and consolidation on both the manufacturer and the integrator side seems to be increasing at a rapid pace.

“Market channel convergence is an important area of consideration,” says David Price, marketing manager, Camden Door Controls, Toronto. “The borders between distinct low-voltage markets, including security, locksmith, door hardware, automatic door, IT and electrical contractor channels seem to become less distinct by the day.” Price adds 2015 was marked by “consolidation on a massive scale — large conglomerates buying other large conglomerates.”

Galaxy’s Rick Caruthers sees this as a potentially disruptive force, on both sides. “We are seeing big video manufacturers buying access companies, where that wasn’t the case before. That is something we are watching. It could have a similar impact to 10 years ago when a lot of the big companies were pulling a lot of things into conglomerations. It does disrupt the channel a little.”

A recent merger demonstrates this disruption, says Richard Goldsobel of Continental Access Control. “Johnson Controls and Tyco are now together and it is another ripple in the integration market. To me the issue is when you have the big companies that have their own access products and their own integration channel and then they merge, who is going to win [on the integrator side]: the Johnson Controls or the Tyco integrator? As the market continues to mature in that way, on the integrator side will there will be new regionals that merge and become national? That will be interesting.”

Jay Slaughterbeck of Strategic Security Solutions acknowledges there is more competition today. “A lot of the national organizations have come to our market. A new class of national integrators are coming and trying to ramp things up…. Competition and build-outs of new business make things a little tougher.”

IT integrators that are trying to push into the security space may find access control a tougher business than they expect, says Jim Coleman of OSS. “We see some competition from folks in the IT industry that traditionally put in switches and servers and think, ‘Why not cameras?’ But we don’t see as much IT competition on the access side, because it is a little trickier. When they try their hand in the world of electrified door hardware and life safety codes, sometimes they get their fingers burned.”

SSD’s David English sees this happening with new entrants, wherever they come from, if they don't have the right experience. We just see more and more companies coming in and saying ‘me, too’ on security. We have lost quite a few projects like that, only to find that they don’t understand and have heavily underpriced and underbid it. They can’t manage an installation for access control from a camera system. We lose jobs on the front end, then get called in after the fact. That is a challenge, but we are getting better about talking about it up front and helping the client understand that you don’t just grab somebody because they say they have access.”

Particularly for the independent integrator, there is a shift starting in the need to differentiate what they do. “The challenge to the integrator today is competing with multi-regional and national companies that keep expanding and growing,” Caruthers says. “For the small, independent companies, they will still have plenty of opportunities to be more personal in a market space than the big ones might.”

RMR is a great differentiator, 3xLOGIC’s Matthew Kushner says. If the cost per door comes down to a relatively low price, these master RMR dealers or integrators could start subsidizing the lock. Here is my Nostradamus prediction: Hardware will continue to come down and the cost to secure a door will continue to come down. Innovation at the threshold will take advantage of all the volume of activity taking place in wireless and cloud and when it hits a price point where someone could subsidize a door price with an RMR model, that could be a risk to some integrators.”

AMAG’s Kurt Takahashi sums up market competition this way: “From the local regionals…it is about driving RMR and differentiating themselves from the big guys. The super regionals will try to grow to compete with the nationals, and the nationals will succeed or fail based on how they integrate with each other.”

With all the excitement over new technologies and integration trends, including cloud, IoT, mobile devices and more, there is one thing that could put a damper on all this progress: cybersecurity.

“We continue to see requirements from end users where they don’t allow IP-related products in unsecure parts of the facility,” says Jim Hoffpauir, president, Zenitel USA, Vingtor-Stentofon, Kansas City, Mo. “Today the requirements for that and encryption haven’t hindered the market. It is not a requirement where we are losing business, but we do see it will have to be addressed in the future.”

While many of the hot trends are coming up from the consumer space, the level of cyber security on those products in that space is “a little sketchy,” says Jim Coleman of OSS. “If you are doing serious security, which most integrators are, and you have clients who are serious about protecting their premises and it is the cloud, how is that information protected? You have to be knowledgeable about encrypting the information when it is stored and when it is in motion. If you are using mobile devices and those aren’t secure — whoa. All of a sudden it could be a huge liability. More than most, when it comes to cybersecurity, our industry needs to eat its own dog food. Many successful integrators started some time ago before cybersecurity was a strong concern. Their processes — like how often to change equipment passwords — are probably a little long in the tooth and in need of review.”

Cybersecurity may be one reason the government has not jumped on many of these newer technology trends, speculates Daniel Prochnow, president, Securityhunter, an integrator that almost exclusively operates in the federal space. “The government is much more careful about the protection of its systems and has much more sophisticated cybersecurity. When we install security systems there are all sorts of processes and protocols we have to go through…. The federal government is ahead of most commercial companies on cybersecurity.”

Prochnow thinks that these types of protocols and procedures will make their way down to the commercial space as more and more cyberattacks happen.

“Every time you have an edge reader or panel you have created vulnerability,” says Scott Sieracki of Viscount Systems. “At some point in time the IT department will finally realize that having a separate system should go away and their IT authentication engines should be the decision makers on who can get into the building before they even come close to the network. That changes the game.”

Jason Ouellette of Tyco adds, “Cybersecurity gets to buying trends. Now that products are IP-centric all the way to the edge, that is the cybersecurity world and our products need to comply with standards and the integrators need to understand what parts are being used. Do they need to Swiss cheese the firewall in order to make their integration work? They need to know the vulnerabilities and how manufacturers are performing their own susceptibility tests and providing cybersecure products.”

More and more, manufacturers in the access control space are stepping up to the plate. Genetec, for example, is focusing on the “security of security” in the coming year, Palatsoukas says. “A big part of the message is about educating the market and helping to bring integrators along and learning from those talking to IT about cybersecurity. There are a lot of smart integrators ramping up. It is not going to happen overnight, but it is something we are working very closely with them on to make sure it becomes part of every conversation when it comes to access control.”

At the end of the day, cybersecurity should be the foundation that end users and integrators start with and build off of, says Mark Duato of ASSA ABLOY. “The old saying is the chain is only as strong as its weakest link. Today IT professionals understand security threats start with cybersecurity and they are investing heavily in making sure those are in place. We need to be able to provide the best overall value in supporting that and leveraging what they already have as their standards.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!