SDM 2017 Security Industry Forecast: Envisioning Change

Results of SDM’s 2017 Industry Forecast Study, coupled with the industry’s outlook for 2020, is optimistic and exciting.

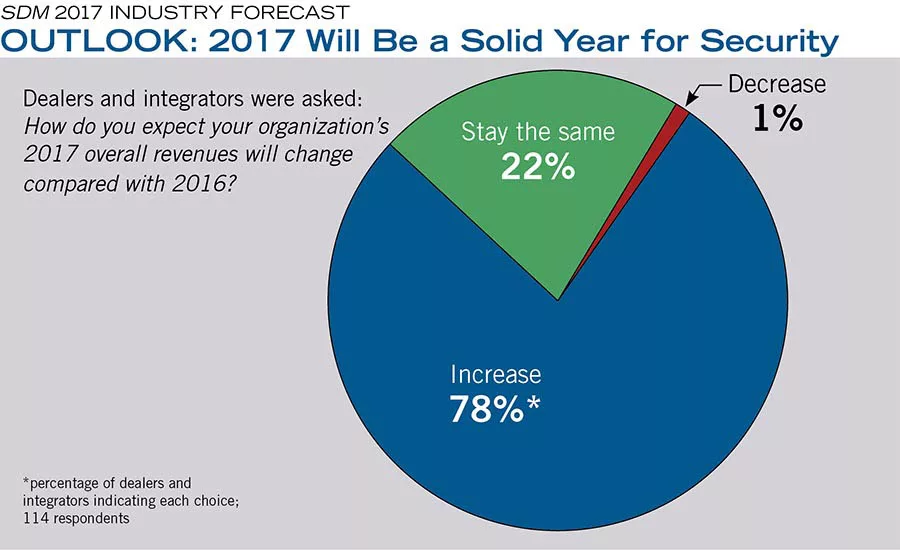

A very solid year is anticipated by respondents to SDM’s Industry Forecast Study. Nearly 8 in 10 (78 percent) expect their total annual revenues to increase. Among those dealers and integrators who expect overall revenues to rise in 2017, the expected mean increase is 17 percent.

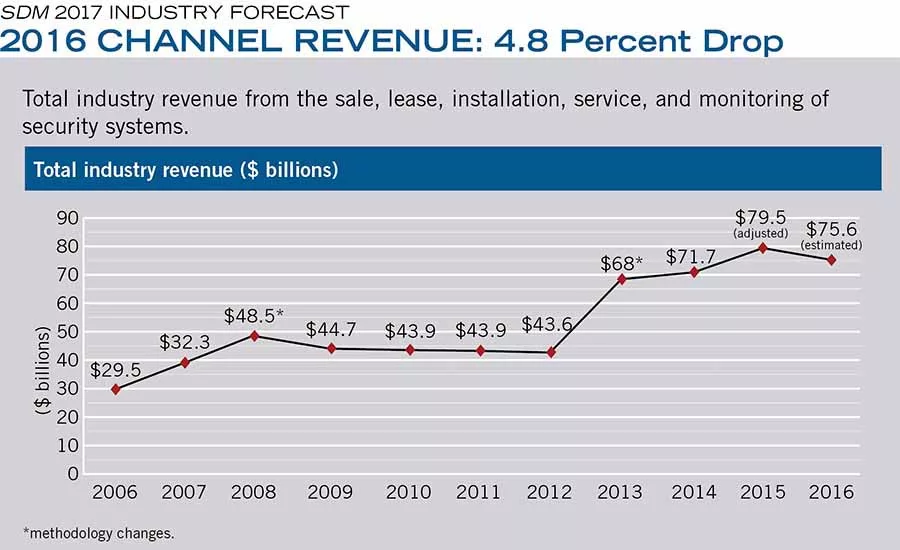

Whereas security integrators predicted one year ago that their 2016 revenue would increase, on average, 6.4 percent, that prediction did not materialize. The total size of the security installation channel in 2016 was $75.6 billion, a decrease of 4.9 percent from 2015’s adjusted $79.5 billion. This estimate is calculated across SDM’s entire circulation database, which is why it doesn’t necessarily reflect the results of the Industry Forecast Study. In the 2016 Study, two-thirds of respondents had increases in total annual revenue, by 16 percent on average.

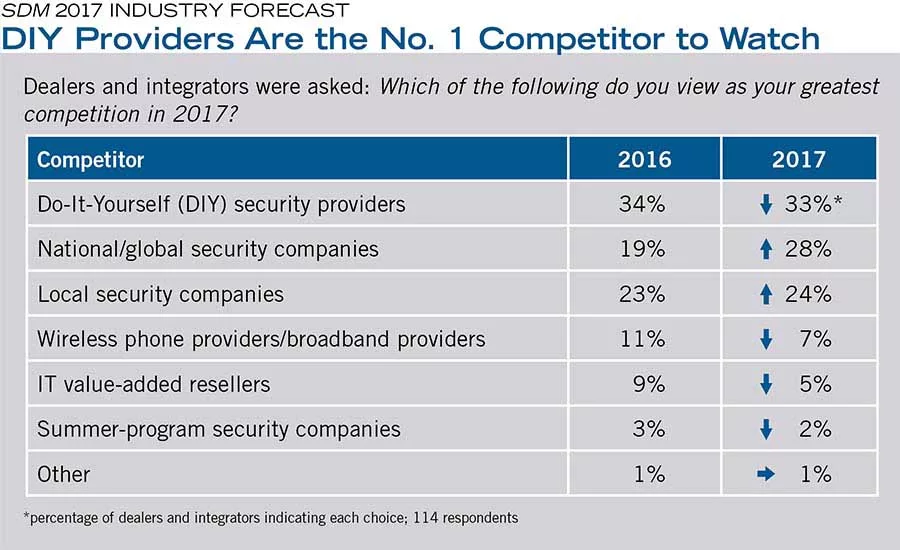

For the second consecutive year, SDM’s Industry Forecast Study respondents selected DIY security providers as their foremost group of competitors. However, respondents also indicated they are keeping their eyes on national/global security companies, many of which made news last year with repeated acquisitions.

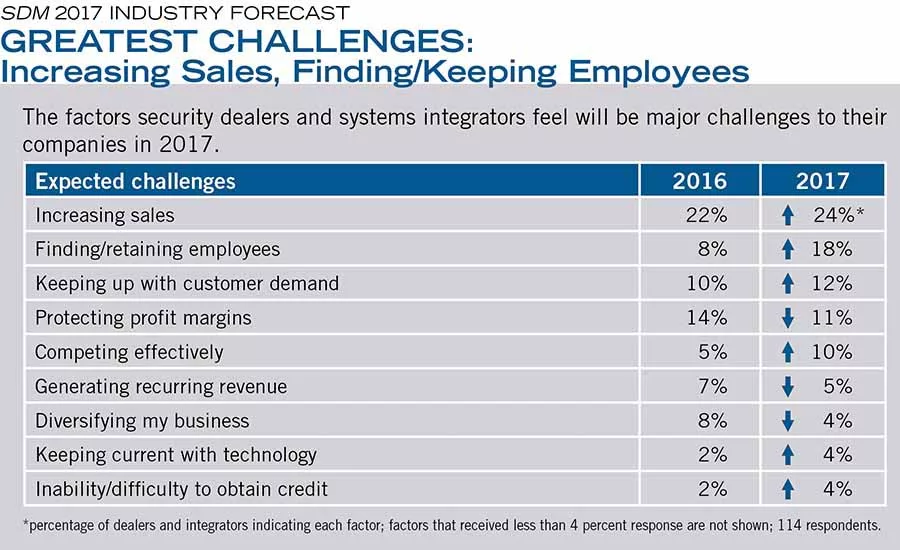

“Increasing sales” is the No. 1 challenge faced by dealers and integrators as they look out over the business landscape of 2017. The No. 2 challenge last year was “protecting profit margins,” but was replaced in this year’s study by the challenge of “finding/retaining employees” mentioned by 18 percent of survey respondents. This may reflect the fact that dealers and integrators think growth in security system sales could be hindered by a lack of skilled workers.

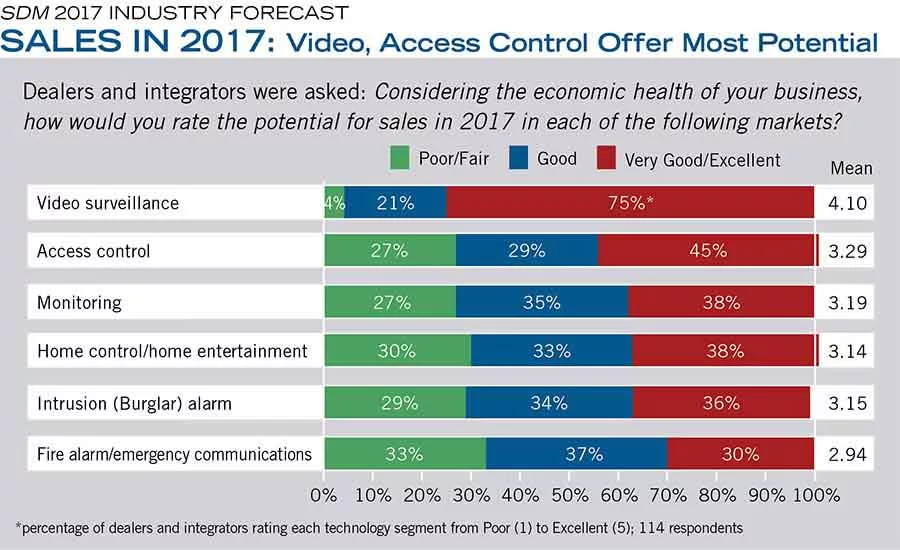

Dealers and integrators think video surveillance will be the most rewarding segment when it comes to producing sales in 2017. When asked to rate the potential for sales among various technology segments, they gave it an average rating of 4.10 out of 5. Following video surveillance was access control — a segment where many changes also are underway in technology — with an average rating of 3.29 out of 5.

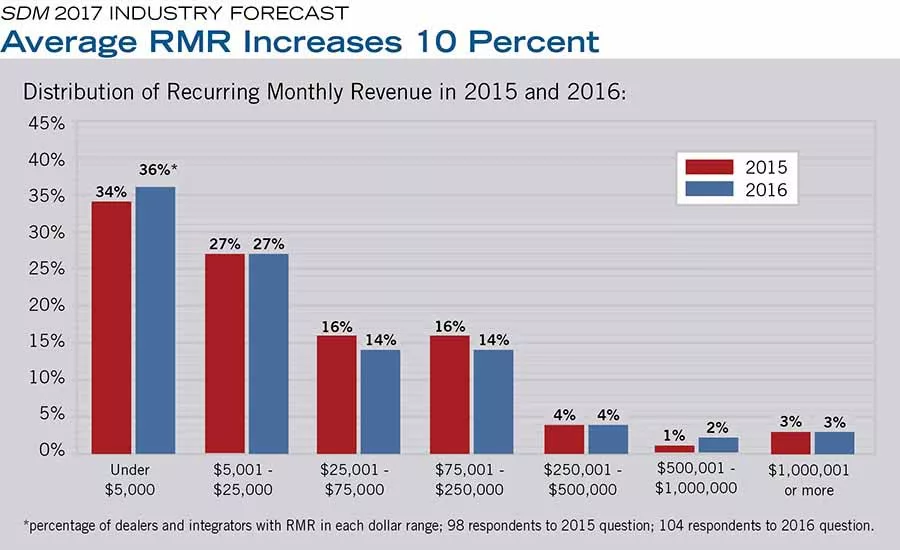

Among companies that generate recurring monthly revenue, 83 percent noted an increase in their RMR in 2016 over 2015. Average 2016 RMR was 10 percent higher than average 2015 RMR reported in the SDM Industry Forecast Study. This table shows the distribution of RMR in various dollar ranges, comparing 2016 with 2015.

The integrator channel expects its top three most fruitful segments in 2017 to be commercial office space, education, and retail. As security concerns in the stadium sector escalate, the segment “entertainment/sports facilities” grew from 1 percent in 2015 to 6 percent in 2016. For the first time in several years, the segment “utilities/critical infrastructure” dropped below 5 percent response.

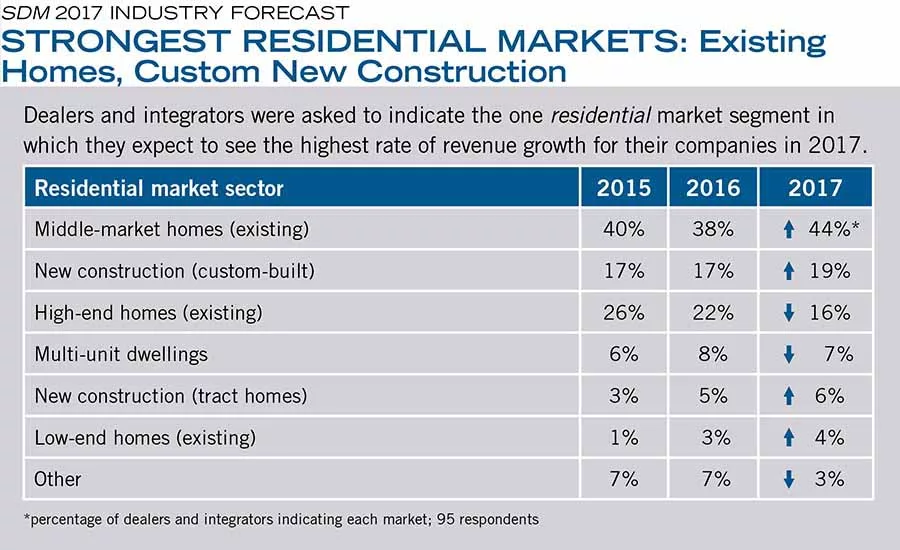

The results of SDM’s 2017 Industry Forecast Study indicate that the percentage of security companies that look to new home construction for sales is increasing — both in custom-built/spec homes and in tract homes. However, more than six in 10 companies still rely on existing homes for both new and add-on sales. There are 118.2 million households in the United States, according to the National Multifamily Housing Council.

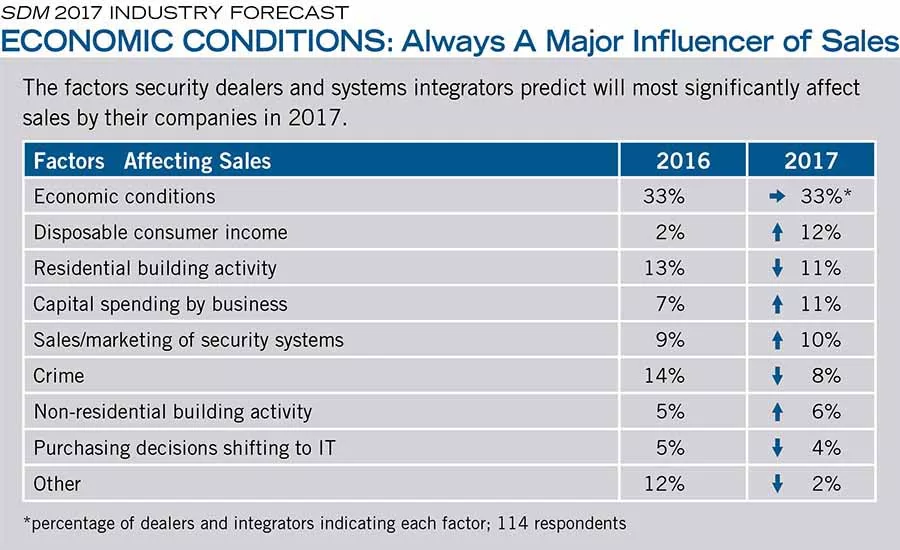

For at least the last 10 years, economic conditions have ranked as the top factor dealers and integrators think will significantly affect their sales — and this factor could have either a positive or a negative spin on sales, but most respondents anecdotally assign it to the negative. Although there have been many indicators of a stronger economy in 2016 over 2015, businesses still are cautious about their spending due to factors such as healthcare and taxes, which could significantly affect the economy in general.

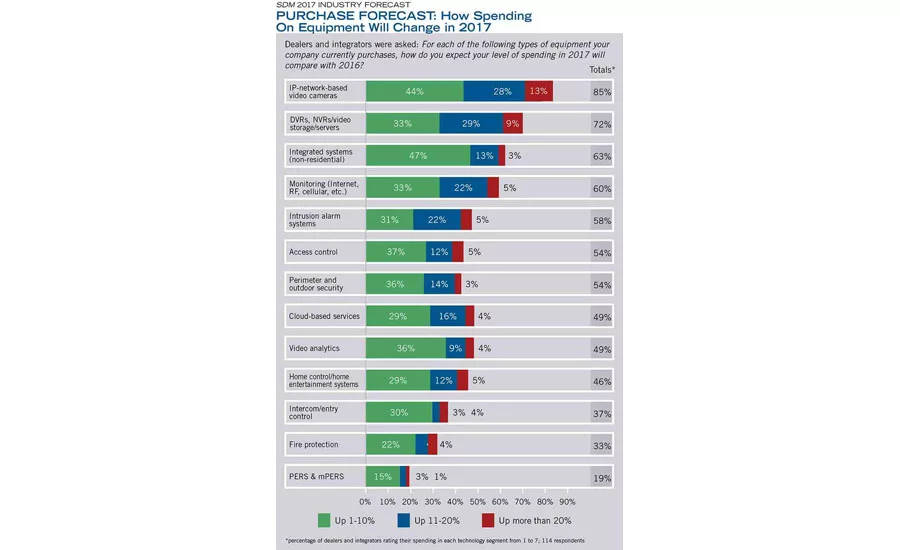

Dealers and integrators were asked to rate how their level of spending on equipment will change in 2017 compared with 2016. This table is based on a 7-point scale where 1/2 = down more than 10%; 3 = down 1% to 10%; 4 = no change; 5 = up 1% to 10%; 6/7 = up more than 10%. This table shows only the “up” responses. The top four categories with the most potential for growth in spending are IP network-based video cameras; DVRs, NVRs, video storage, servers; non-residential integrated systems; and monitoring.

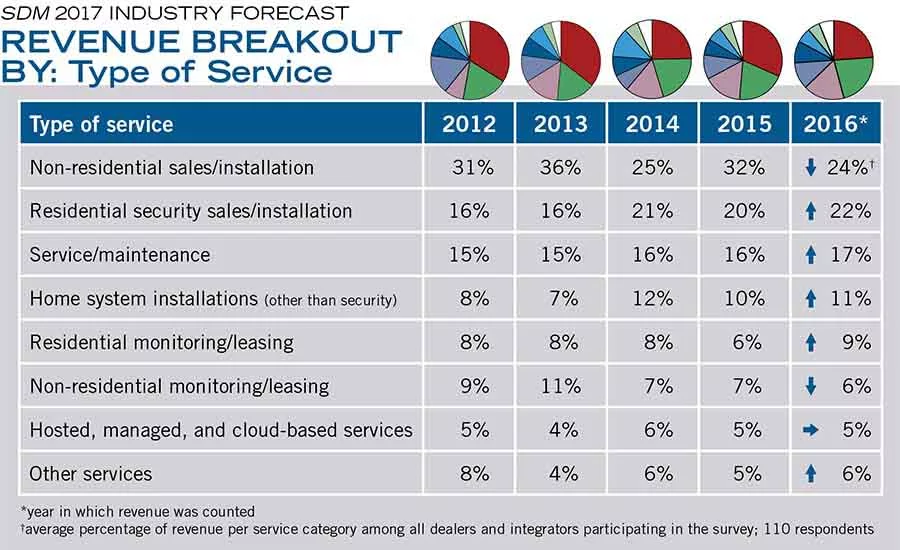

SDM’s Industry Forecast Survey tracks how dealers’ and integrators’ total revenue is distributed among types of services. Together, 46 percent of revenue comes from non-residential and residential sales/installation. The share of revenue from both residential installation and residential monitoring increased in 2016.

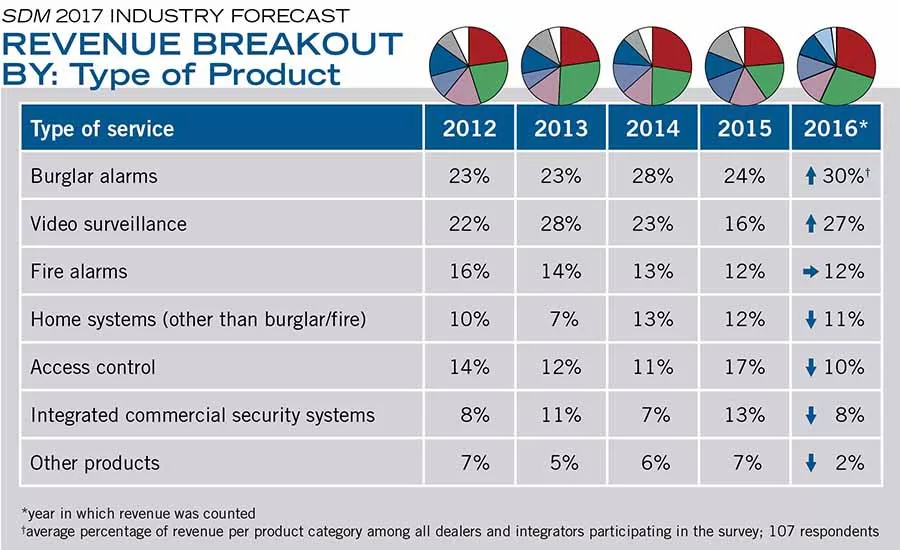

SDM’s Industry Forecast Survey tracks how dealers’ and integrators’ total revenue is distributed among types of products. The 2016 results show how the channel is diversified in its product offerings. Note the significant increase in portion of revenue from burglar alarms last year.

If the word “change” isn’t part of your security industry business plan this year, you’d better rethink it. SDM’s 2017 Security Industry Forecast Study showed that two-thirds (67 percent) of participating security dealers and security integrators increased their total annual revenues in 2016, and their average increase was 16 percent — a sizeable, but not unreachable growth rate. Roughly one-third (32 percent) stayed flat. But one area in which bigger change was substantiated was in recurring monthly revenue (RMR) measured by the study. More than eight in 10 security dealers and security integrators (83 percent) said their RMR rose in 2016 — by as much as 64 percent on average.

Anecdotally, there never has been such emphasis placed on growing RMR — but in 2017 it could materialize in some unusual ways. This month’s cover subject, John Campau, president and CEO of Comtronics, Jackson, Mich., looks at both traditional and non-traditional products and services for driving RMR.

“My dad always told me to embrace technology at Comtronics, and he was right. I am humbled to report that our $50 million annual revenue today is for products and services we didn’t offer when my dad passed away in 2008. The way we run our business today is 100 percent different from when I worked side-by-side with my dad 10 years ago,” Campau describes of the company he and his wife, Anne Campau, now own but which was founded in 1958.

SDM’s Industry Forecast Study, conducted annually since 1982, portrays the security channel as one still comprised mostly of small businesses: One fourth of respondents estimated their 2016 total annual revenue would be $250,000 or less; while slightly more than half of respondents estimated it would be between $250,001 and $2.5 million. Comtronics is actually quite large for a family business. With $50 million in annual revenue — about 10 percent of which represents security — Campau, at press time in early December, estimated total annual revenue from security would grow 10 percent in 2016.

He also estimated Comtronics’ RMR would grow 5 percent in 2016, and he forecasted 10 percent growth in RMR in 2017. “One incredible trend we have seen the past five years is that RMR is becoming a bigger percentage of our total security revenue,” Campau says. RMR comprised 45 percent of total security revenue in 2015, but about 50 percent in 2016.

In some areas, SDM’s Industry Forecast Study bears this out. Asked to break down their total annual revenue by the type of service offered, survey respondents indicated that revenue categorized as non-residential sales/installation fell from 32 percent in 2015 to 24 percent in 2016. However, both the residential sales/installation and residential monitoring categories increased slightly in share-of-revenue.

And although the percentage of revenue that security dealers and security integrators earned from hosted, managed, and cloud-based services stayed the same at 5 percent of total revenues, those are the types of services that many professionals such as Campau regard as the industry’s foremost change agents.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

“I see our future with more of a focus on cloud-based solutions, continuing the trend of being more service oriented — not hardware oriented — and with an increasing emphasis on lower price points with higher RMR,” Campau says.

John Wells, operations manager at Comtronics, says cloud services are one of the main reasons Comtronics closed its central station in 2016 and moved its subscriber accounts over to Lake Forest, Calif.-based National Monitoring Center (NMC), which offers I-View Now video verification and other cloud services. In addition, he says, “Alarmnet 360 is becoming more of a cloud platform. [Honeywell is] redoing the Total Connect apps to interface with more products, such as Skybell. So absolutely, we certainly see the cloud kind of taking over; in fact it already has,” Wells describes.

In addition to its security business, Comtronics operates 19 Verizon Wireless retail stores in Michigan — giving it platform for marketing its do-it-yourself security system offerings. While SDM’s study shows that respondents consider DIY providers to be their No. 1 competitor, some dealers have begun to think that if they can’t beat them, they should join them. Comtronics, which is a platinum-level Honeywell Authorized dealer, also has plans to launch its Honeywell-based DIY initiative with other Honeywell alarm dealers and with other cell phone dealers around the country, in a revenue-share arrangement. The switch to NMC, which has a national footprint and licensing in place, will help facilitate that plan.

Nearly 8 in 10 (78 percent) respondents in SDM’s study expect their total annual revenues to rise on average 17 percent in 2017.

At Comtronics, growth will come from a variety of initiatives. “Video verification will become a larger part of our business because the technology is here to stay, and because we include it with every video sale,” Campau says. “We will continue to identify our customers ‘pain points’ with a focus on delivering a better customer experience in 2017. We are opening our first security showroom next month that will include the latest products and services our industry has to offer. We will continue to leverage our 19 retail stores to sell alarm systems, with bundled offerings like $100 off a DIY alarm with purchase of a cellular phone. With all the integrated products available on the market today, we aren’t just selling alarms anymore; we are selling a lifestyle.”

For some security professionals, to position themselves for the future requires this type of thinking. For others, such as security integrators serving non-residential markets, changes may be more subtle. But one thing is certain: 2017 is sure to be categorized as a transformative year.

Check out 20 Visions for Security in the Year 2020

Check out SDM Annual Industry Forecast

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!