State of the Market: Video Surveillance 2017

The video surveillance market is on a steady course of growth for now and into the foreseeable future. With a slight uptick in growth this year and not many surprises on the horizon, steady as she goes seems to be the safe bet.

As the price of cameras continues its downward trend, dealers and integrators are able to offer customers more options and broader solutions. Integrators such as Sonitrol of Evansville’s Chris Dingman seek to strike a balance between cost and quality of cameras to give customers the best solutions for their budgets and needs. PHOTO BY WWW.DANIELKNIGHTSTUDIOB.COM FOR SDM

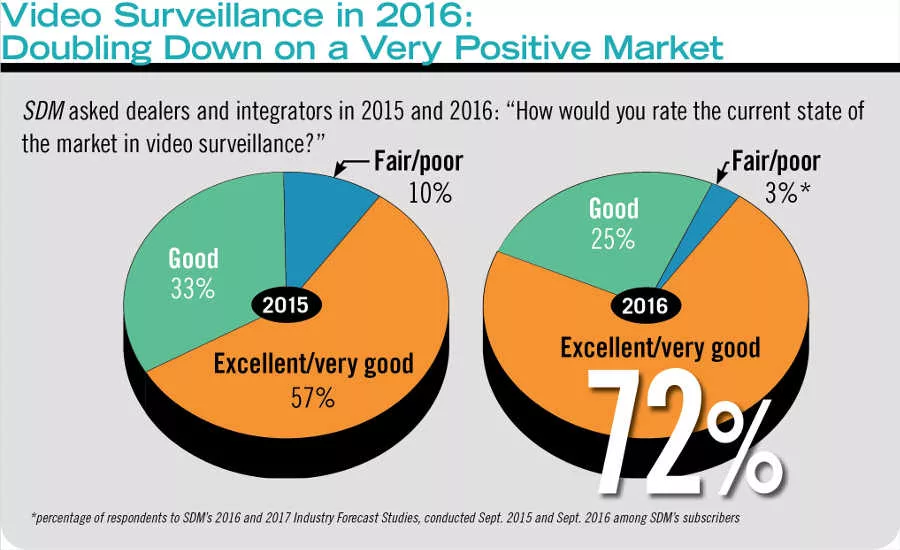

In 2016, 97 percent of respondents to SDM’s Industry Forecast Study deemed the state of the video surveillance market to be either good, very good or excellent. The positive got notably better, and the fair/poor decreased to a sliver.

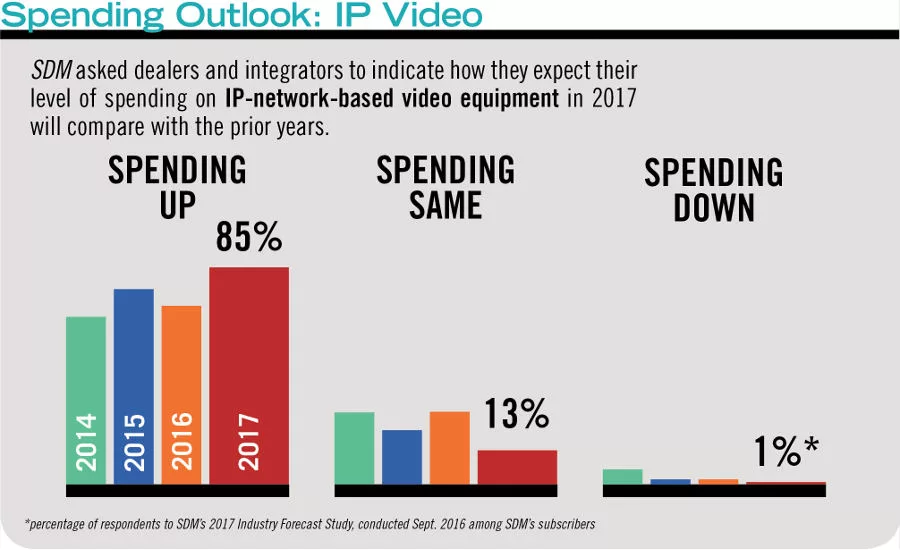

Seventeen in 20 respondents to SDM’s Industry Forecast Study expect their spending on IP-network-based video equipment to increase this year compared with 2016, not only rebounding from the previous year’s dip, but making 2017 the highest spending year yet in the category, if expectations come to fruition.

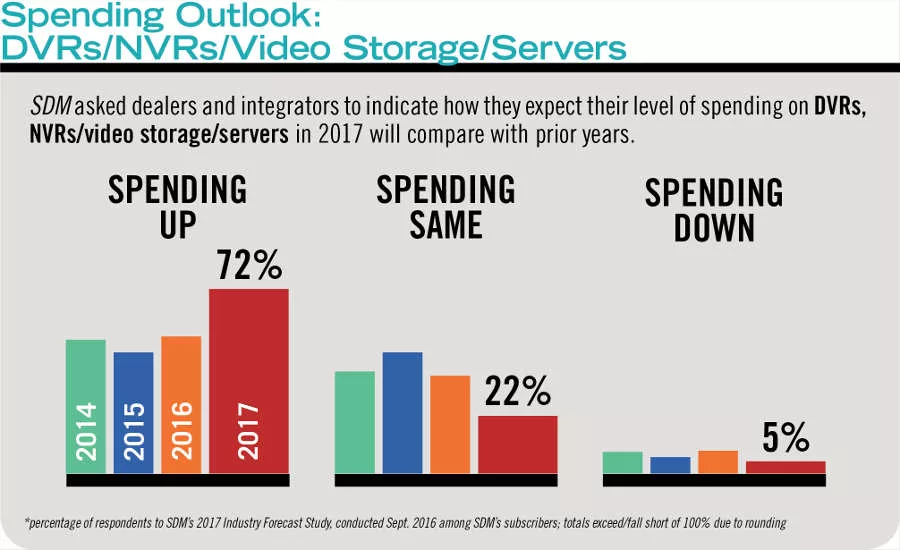

The number of respondents to SDM’s Industry Forecast Study indicating they plan to increase their spending on video storage/servers rose to more than 50 percent last year. For 2017, however, nearly three in four plan to increase spending in the category.

Sonitrol of Evansville's Chris Dingman (right) and security consultant Andrew Beitler visit a customer's business. Dingman says the company is able to meet customers' expectations thanks to lower equipment costs improving technology. PHOTO BY WWW.DANIELKNIGHTSTUDIOB.COM FOR SDM

In 2017, 96 percent of respondents to SDM’s Industry Forecast Study expect the state of the video surveillance market to be good, very good, or excellent. This compares with 89 percent who expected the same a year ago.

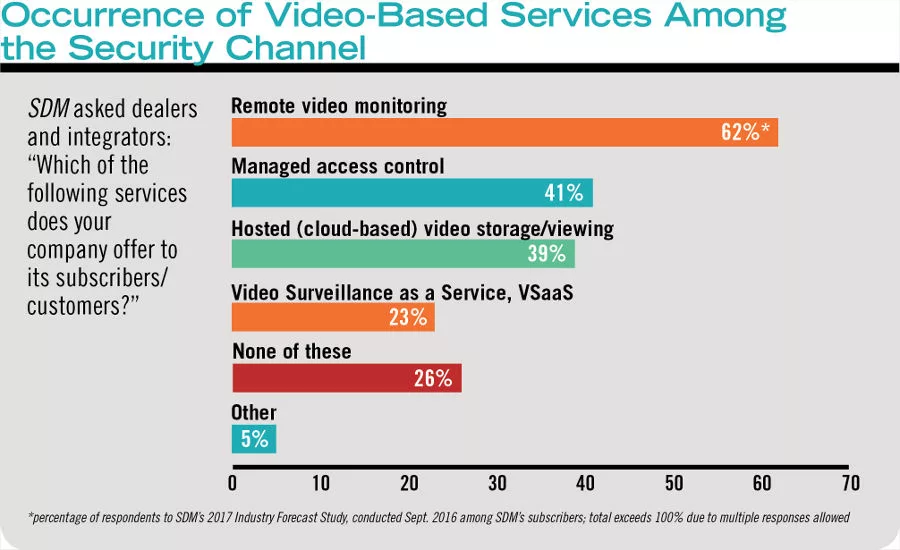

Underscoring the market’s opportunity for dealers and integrators to generate more RMR, video accounts for three of the top four post-installation services offered by respondents to SDM’s Industry Forecast Study.

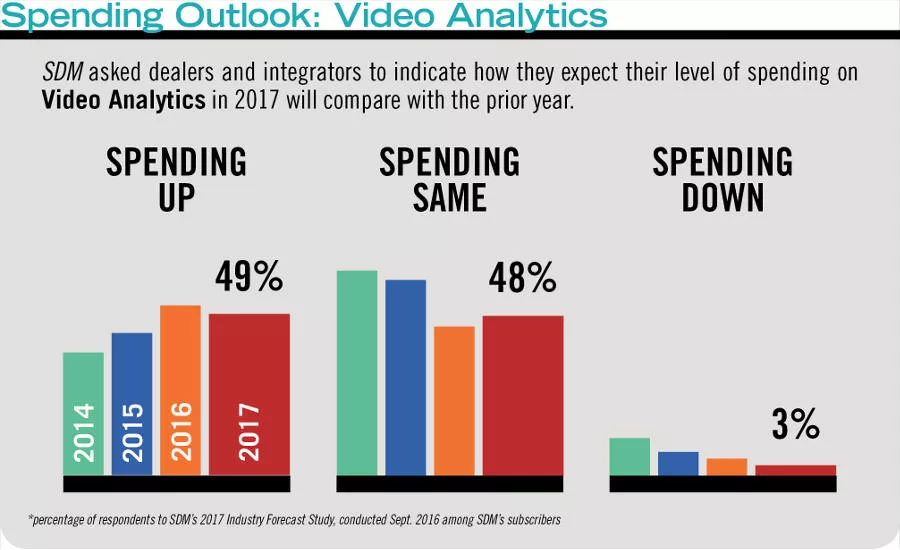

Video analytics appears to be in a holding pattern this year, with no more than a 3-percentage-point change in any buying category in SDM’s Industry Forecast Study.

PHOTO BY WWW.DANIELKNIGHTSTUDIOB.COM FOR SDM

Thanks to improving technology, integrators are able to offer solutions that cover more space with fewer cameras. Shown here is the perspective of a camera Sonitrol of Evansville installed for a customer overlooking the counter area. PHOTO BY WWW.DANIELKNIGHTSTUDIOB.COM FOR SDM

It was the story of 2016: growth — sometimes stellar, sometimes slight, but mostly steady. The state of the video surveillance market is one that will continue to see growth due to several factors, but each company that SDM interviewed for this exclusive annual article reported growth.

Some of the factors that have been and will continue to play a large role in the steady growth of the video surveillance industry are: increased awareness of cybersecurity threats and the need for more secure solutions; savvier customers who understand the products and solutions better than ever and know what they want; a resurgence of video analytics as the technology gains a larger field of practical applications; increasing features and decreasing prices of video equipment; and the increasing acceptance of technologies such as cloud and wireless.

As the industry is now past the analog/IP tipping point and the majority of installations are IP, upgrades and communications grow increasingly easier and more efficient, offering plenty of opportunities to security dealers and security integrators. Those who are committed to being on the cutting edge of this technology and who are well-versed in the language of cybersecurity will succeed in this new market.

Even in light of the incoming presidential administration, those in the industry can anticipate trends toward increased funding for infrastructure rebuilding, which could include electronic security upgrades to transportation, homeland security and other sectors. (See related story, “2017: Year of Transition & Immense Opportunity for Security,” on page 55.)

Each of these factors bolsters the overwhelming sentiment expressed by security professionals that the state of the video surveillance industry is strong, and will continue to grow.

“This industry is going to be and always has been indicative of what the market and consumers have done. I don’t think we’re a fast-paced industry by any means. So I don’t think anything is going to catch us by surprise, and in six months it’s not going to be any different,” says Tom Cook, vice president of sales, Hanwha Techwin America, Ridgefield Park, N.J.

“I think there is going to be a focus on cybersecurity (see related story, “Cybersecurity Meets Security,” on page 58); there is going to be a focus on analytics; there is going to be a focus on the expansion of megapixels,” Cook says, adding that he doubts there is going to be anything that comes out of the woodwork that no one foresaw.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

Brent Edmunds, president and co-founder of Stone Security, a security integrator based in Salt Lake City, says, “We felt like 2016 was another strong year for video surveillance. The larger IP systems seem to be maturing nicely, and customers’ understanding of what the possibilities are with video surveillance is clearer.”

Scott Schafer, executive vice president, Arecont Vision, Los Angeles, says his company is looking forward to an excellent 2017 because the multi-megapixel camera segment will be even more important; customers are moving faster to single-sensor cameras and multi-sensor panoramic cameras to replace PTZ products; and the value proposition of open systems is more accepted in the security community. (See related story, “Increasing Standards Versus Shrinking Privacy,” page 62.) He says there also is a pent-up demand for security systems by retail, bank and government end users because these segments were more impacted by economic challenges and they all reduced investment in new security systems in the recent past.

Larry Newman, senior director, sales, Axis Communications Inc., Chelmsford, Mass., says, “Axis will continue to perform well in 2017.” Newman attributes this projected success in part to Axis’ investing a substantial amount of its revenues into research and development every year: “Axis has also broadened its focus to include three different segments of the market. In the past, our products primarily served the enterprise portion of the market; now we have offerings to meet the physical security needs of small and medium business, as well.”

Sean Murphy, regional marketing manager, Bosch Security Systems Inc., Fairport, N.Y., says, “We expect to grow again in 2017 at a rate that will outperform the market. This will be fueled by new product releases as well as continued focus on how our video products integrate with intrusion detection, access control and communication technology to create complete solutions for end users.”

Keith Drummond, senior director, IDIS America, Coppell, Texas, says, “We will be entering our third year of operations at ISC West 2017, and doing so on a steady growth trajectory.” Drummond says IDIS is enjoying more interest and installing more solutions than ever. “I fully expect that to continue into 2017.”

Jennifer Hackenburg, senior product marketing manager, Dahua Technology USA, Irvine, Calif., says, “Performance is expected to be highly accelerated in 2017, with no sign of slowing down.”

Keith Jentoft, integration team, Videofied (a Honeywell Security and Fire company), Vadnais, Minn., says in terms of quantity, 2016 was a good year.

“I think 2017 is going to be more of the same,” he says. “The IP camera market is getting more and more competitive. But managing those cameras, video management systems, how do you feed that to the customer — that’s becoming more and more important.”

Jentoft warns that a falling price point means companies have to sell more cameras to stay on the top line. “Our products have become less expensive with better features, and it’s been a big deal.”

Falling prices are at once a boon and a burden to the video surveillance industry. On the one hand, falling prices mean companies such as Videofied must sell more units; but on the other hand, it also means companies that might not otherwise have been able to afford installing a system now can, or they might purchase more cameras than they would have been able to several years ago for a more effective system.

“Maybe I couldn’t afford a $10,000 solution,” Jentoft says, “so I wasn’t in the market; but a $500 solution, I’d love to buy one.”

Schafer explains the benefits of dropping prices in terms of meeting customers’ needs: “New low-cost products and lower cost, value-added designs have provided a superior ROI at the same price, and even more value at a lower price. Either way, the customer wins.” He explains that the ability to drive solutions for every kind of business allows companies to deliver solutions that were not possible before. “Systems integrators can replace their end users’ old systems with a more robust solution, requiring fewer cameras, gaining much more usable data for the same price that their old system cost them. They get a better solution at a lower cost that provides a better way for security employees to do their jobs.”

Sonitrol of Evansville seems to have struck a good balance in this regard: “We were presented with a special award from our manufacturing partner for selling the most cameras within our Sonitrol National Dealers Association,” says Chris Dingman, operations manager, Sonitrol of Evansville, Evansville, Ind. (featured on this month’s cover). “We have also worked closely with 3xLogic and Sonitrol to test new technologies for verified video solutions. We try to find a balance between cost and quality of cameras to give the customer the best solution that meets their expectations and budget.”

Cook attributes the success of his company and others like his to new methods of going to market. He says well-established companies are beginning to change their tactics and approaches to the market, while companies that weren’t traditionally market leaders are setting the pace for how to go to market. “They’re different approaches: one is from technology, one could be by price, one could be by working directly with the end user, and technology — staying competitive with technology.”

Much of it comes down to learning to stay on that competitive treadmill, as Cook calls it. “Thirty years ago there were 10 video vendors — that was it. Then there was 100; you had anything and everything. Everybody had camera this, that, whatever. But now the competitive treadmill has changed.

Cook says learning to stay with the industry’s price points is going to be crucial to a company’s gaining market share.

Another characteristic of the evolving market, Cook says, is a race to the cutting edge of technology. As the market shifts to quicker, faster-paced requirements, the companies that are investing in R&D to support the security industry are the ones that are going to be leaders. “That’s what’s going to mold the landscape,” he says.

Drummond sees this as a time for the industry to make strides. “For a variety of reasons, our industry has been shaken up and continues to be,” he says. “Mergers and acquisitions have married technologies that were once merely complementary, and the most creative and innovative players in our industry have stepped up their game, delivering genuinely powerful, more capable, and more useful technology to the market today than we’ve seen in a long time. From market-driven solutions that make existing technology easier, faster, more powerful and more affordable for end users, to banner, one-off breakthroughs in specifications, the business case for upgrading or moving forward with fresh, modern technology is starting to make itself.”

In 2015, Drummond says those at IDIS were still having conversations regarding the place IP networked surveillance, higher resolution and analytics would have in the industry. “In 2016, these [conversations] changed markedly, and we began to talk about next-generation surveillance as a foregone part of any modern surveillance mix.”

Along with this pivot to the future came very real concerns about security, particularly cybersecurity, Drummond says, as current events and popular culture made the risks inherent in an ever more connected world more understandable — and scary — than ever. “We’ve had some uncomfortable discussions regarding everything from the provenance of some popular offerings in our industry, to the basic risks certain technologies can make us more vulnerable to, and I think we’ve been challenged to be smarter and savvier about the future of next-generation technology in the process. That can only mean good things in 2017 and beyond.”

These talks might be uncomfortable, but they are discussions all companies must have in an ever-changing industry.

Brandon Reich, senior director surveillance solutions, Pivot3, Spring, Texas, agrees. “Modern systems integrators need to be educated on the best ways and solutions to meet their customers’ surveillance and IT expectations. Being knowledgeable about new innovations and IT requirements can help integrators sell infrastructure, which allows them to keep the hardware sale rather than losing server sales to a customer’s internal IT department.”

Integrators are tasked with ensuring surveillance customers can benefit from the best practices and solutions proven in the world of IT, Reich says. “The interest in new technologies is growing at a rapid rate. Now is the time to for today’s leading installers to ensure the expertise within their own organizations to help exceed customer expectations.”

The video surveillance market may not be “your grandfather’s video surveillance market,” or even your father’s — no longer is it simply a straightforward video surveillance install. Now it is video plus analytics; now it is video plus IP networks; now it is video stored remotely; now it is video plus access control — and security professionals agree that the future is just as bright as ever.

Whether Washington increases infrastructure spending is yet to be seen, but increased spending in the video surveillance industry seems a safe bet, and security dealers and integrators must continue to strike a balance between cost and quality, offering the solutions consumers want along with the peace of mind that their information is secure.The state of the market continues to be strong, and security professionals don’t anticipate any changes in that regard any time soon.

MORE ONLINE

“State of the Market: Video Surveillance” presented here is part one of a six-article series to be published throughout the year. The series will also address the topics of Security & Monitoring (March 2017), Access Control (April 2017), Fire Alarm (June 2017), and Connected Home (August 2017). Each article will feature additional content that is available online only at www.SDMmag.com/StateoftheMarketSeries.

A New Administration & Its Possible Effects on the Video Surveillance Train

Every company is affected by mandates and regulations, but what effect do these factors have on the security industry? Larry Newman, Axis Communications Inc., believes escalations in mandates and legislation affords the industry more opportunities to provide security solutions to the market.

“The physical security space itself is a relatively recession-proof business because when the economy is very strong people are willing to spend money to protect what they have,” Newman says. “When the economy is difficult people are still willing to spend money to protect what little they have. Certainly the state of the economy, as well as events in the global theater, are having an impact on our industry. Every day we’re facing more mandates and legislation regarding cybersecurity, privacy, compliance and life safety that we have to address. We’re expected to deal with a wide range of issues from perimeter protection around a water treatment facility, to monitoring environmental compliance at a petrochemical processing facility, to protecting personal data sitting on servers in a hospital or retail store or financial institution.”

Also on many minds is the question about the incoming presidential administration. Tom Cook, Hanwha Techwin America, explains that having a Republican president generally means some changes for the industry as opposed to having a Democrat president.

“Anytime we’ve had a Republican in charge of the White House, we’ve seen more spending from different verticals,” Cook says. “I don’t know if there is additional money spent in the security industry, and I’ve never charted it, but what I see is a shift of dollars. So a Republican Party or president will spend more in the government sectors or the government-supported sectors such as corrections — you’ll see a lot more grant and bond money go to corrections, military, or government-affiliated outfits.

“We’ll see less possibly to state and local and education. Grant money might be lower in education, which could affect school district funding — security products for school districts and education.

“So if I look at the public sector, I think it’s a shift of dollars. [In the past eight years] we saw a weakening in the corrections; we saw maybe a weakening in airport grant money that was government money. Now we might see that strengthening up and see a little less in education.”

Overall, however, government regulations and economic changes don’t seem to disrupt the security industry as much as they might disrupt other industries, experts say.

2017: Year of Transition & Immense Opportunity for Security

The 115th Congress convened on January 3, 2017, and the swearing in of a new president on January 20 signaled new opportunities for the industry to take shape through policies, legislation and funding.

While thousands of bills will be introduced, knowing where to look and how to take advantage of these opportunities will be important. Knowledgeable transition watchers know that more than 3,600 key political appointment jobs will be filled over the year by the White House, some requiring Senate confirmation. These officials, especially at the lower levels below the Cabinet, will be making critical decisions on program funding and policies that will impact the $4 trillion-plus federal budget. Congress will extend the Fiscal Year 2017 funding to April 28, 2017, and will then turn to funding decisions for Fiscal Year 2018 budget (the first budget of the Trump administration), which begins on October 1, 2017.

At the federal level, Congress has promised in this transitional period to go back to what is called “regular order,” which means more oversight and input into the Executive Branch (government agencies) on spending priorities. For the last eight to 10 years government officials made most of the decisions about what projects to fund, what policies to implement and who receives contracts.

Although the new administration has yet to detail the kinds of programs or projects that could lend themselves to opportunities for the industry, trends for 2017 can be anticipated. These trends will require direct interaction between the Congressional committees and subcommittee that have funding and oversight jurisdiction linked to the department or agency. For example, the new Trump administration has already broadly announced that billions of dollars will be requested for infrastructure rebuilding, which could include electronic security upgrades to transportation, homeland security and the like. They have also indicated strong support for law enforcement, military build-up, cybersecurity and other areas that will include electronic security and monitoring capabilities. We can expect to see these new funding objectives in the fiscal year 2018 and perhaps into the rest of the Trump administration through January 20, 2021.

One “small” example of the new Congressional impact can be found in a U.S. House Oversight and Government Reform Report, released by Chairman Rep. Chaffetz (R-UT) on December 6, 2016, titled, “State Department’s Failure to Protect our Diplomats.” The 178-page study reviewed the lack of proper funding for security at U.S. embassies around the world and recommends very specific changes be made. The report highlights the need for long-range building plans and requirements for “infrared cameras at all U.S. Embassies and Consulates.” The report also discusses the lack of camera security and the need to upgrade or purchase these devices. Additional information can be found at: http://bit.ly/2jKXexx.

The State Department is just one agency that will be refocusing its priorities based in large part on Congressional interest and involvement in the next four years with support from the administration. How much funds and what types of issues will be reviewed are questions yet to be resolved. However, the opportunities are immense. — Contributed by John Chwat, ESA Director of Government Relations

Near-Future Drivers of Growth

The market’s steady growth can be expected to continue, but what factors might accelerate growth in the near future even beyond what we see today? Alessandro Araldi, Honeywell Security and Fire, offers several suggestions, including the rise of IP video, integration of video into new sectors, the increasing popularity of mobile cameras and the improvements made in video analytics.

“There are things that could lead to accelerated growth in the years to come; I think analytics is one of those things, and specifically with analytics, deep learning.”

Araldi explains that several companies are working in that space and providing underlying technology for deep learning that can be applied to video analytics. “That is going to transform what you can do with video, because today, for example, when you have an incident, you have to go back and basically review hours and hours of video until you identify the moment when the incident happened,” he says. Deep learning, he explains, promises quick searches that pinpoint exactly when an incident happened, as well as being able to search for different criteria.

Tom Cook, Hanwha Techwin America, says Hanwha Techwin is working with companies in the banking sector that want it. “We partnered with FST, a facial company, but there are more requests for analytics and those type of things for identification than I’ve ever had,” Cook says. “The market leaders are definitely looking and acquiring companies or developing products for those requests.”

Cook says the drive toward higher resolution is a result of more and more people trying to use camera systems for better recognition. And while analytics and facial recognition have improved dramatically, it still isn’t at 100 percent. “Human nature expects 100 percent guarantee: If I buy something it should be 100 percent working. Most analytics aren’t. They’re 90 percent — 95, who knows.” For facial, Cook says 85 percent is extremely good.

“So I don’t know if it’s accepted yet from an end user standpoint,” Cook continues, “and it’s a mentality thing. We’ve become a society that expects perfection even though we’re not perfect. If I’m going to buy something, I want it perfect.

I don’t want 90 percent.”

Cook doesn’t see this as something that should scare integrators away, however. “From the standpoint of services, the integrator would be wise to jump on the analytics bandwagon. Analytics are not going to be 100 percent, but being the dealer who understands it and allowing the customer to pay for a service with the ability to tweak the analytics, to make it better, to upgrade it, to modify it for the customer’s need or to make suggestions — I think jumping on that would allow the integrator to be successful in growing their business and their expertise a bit with the end user.”

Another factor is the rise of mobile cameras. “If you think about a VMS today, the cameras that feed the video into the VMS are mostly static, stationary cameras,” Araldi says, “but more and more we see mobile cameras, whether these are moving cameras or simply cameras in mobile phones, eventually providing video feeds to a VMS, so that could make for a much richer set of information.”

Cameras and video technology are also being embedded into other devices, Araldi says, such as the digital ceiling. “As buildings are getting retrofitted with LEDs, people are using the lighting fixtures to embed a whole bunch of sensors in there, which then enables many different uses, including the ability to track people in the building, and therefore organize the real estate and reduce operating costs. You can imagine embedding even sensors and cameras into lighting fixtures.”

Along that same vein, Araldi says that beyond integration with access control, “we see integration of video with access and intrusion, and eventually with entire building management systems.”

The final factor is the cloud. Araldi says he sees video being stored in the cloud for SMBs, and then over time it might make its way into the enterprise itself. Araldi says the cloud enhances the value of video because it allows companies such as Honeywell to deploy new features and functionalities for hundreds of thousands of customers and to integrate more easily with other applications.

Cook adds, “I think people are accepting the cloud, and I think the big companies are smart enough — they’ve already offered cloud products and you’ll see more and more of that, and more acceptance of it; they’re not as scared anymore. So I think the dealers that are positioning themselves to offer cloud services … are putting themselves in a good position.”

Araldi adds, “These are some of the key trends we see. It is difficult to say, ‘In two or three years because of this trend we’ll see growth rates spiking to 20 or 30 percent’ — nobody can tell you that — but these are the things that are going to drive the growth for years to come.”

And while these are not the biggest growth factors now, Araldi says they are actually not that futuristic. “They are possible today and they are starting to happen. So those could drive further adoption and growth of video.”

Cybersecurity Meets Security

It’s no secret that one of the biggest concerns for businesses of any size is cybersecurity. And with all the attention it has been receiving in the past few years, it is no longer a footnote; it is a primary concern, and that includes the video surveillance market.

“Cybersecurity seems to finally have found its way permanently into the discussion in the video surveillance world,” says Brent Edmunds of Stone Security. “Physical security integrators that don’t learn more about cybersecurity will fall behind very quickly. This is a major concern for 2017 and beyond.”

"Cybersecurity seems to finally have found its way permanently into the discussion in the video surveillance world."

Some hackers are finding out that cameras are the least secure connected devices out there and are starting to exploit vulnerabilities for denial of services attacks, as evidenced in the recent Dyn DDoS attack.

Due to this and other malicious attacks, governments both in the U.S. and globally announced they would be taking a very hard line on video and demanding very stringent requirements for cybersecurity.

Cybersecurity poses a problem to many dealers and integrators who lack the proper training and skillset to tackle the issue, says Alessandro Araldi, Honeywell Security and Fire. “Many integrators are increasingly relying on the manufacturers not just to provide the necessary technology, or tools, but also to train them and bring them up to speed on what cybersecurity means, and basically how to install and deploy these video solutions on a network in a way that minimizes any cybersecurity risks. It’s not just about the cameras themselves, but about the connectivity of the camera, the recorder, the VMS — then any other system that might be connected,” he continues. “So you actually need to know what you’re doing when you’re deploying the systems, above and beyond what the manufacturer makes available to you, to make sure you close any port that could be exposed to external attacks.”

Making this all the more imperative for dealers and integrators, Scott Schafer, Arecont Vision, explains that the integrator’s role necessitates he or she become knowledgeable in this area. He says systems integrators can accomplish this through a three-pronged strategy: “First, their employees need to become conversant in the subject. Since many systems integrators are the trusted advisor to their end user customers, they need to show their clients that they understand the seriousness of cybersecurity and how they can help their customer. Second, they need to better understand the importance their customers are placing on cybersecurity and the solutions their company can deliver to mitigate potential problems. Third, systems integrators need to choose products from their product vendors that meet their customer needs for cybersecurity.”

Keith Drummond, IDIS America, says dealers and integrators should be ready for these questions, even the uncomfortable ones, and move past the canned answers we’ve seen in the past. “Real talk regarding the origins and risk inherent in some offerings, and a respect for the validity of customer concerns is going to matter a lot,” he says. “Being prepared to answer those concerns and put them in the context of price, quality, origin, performance, and risk of various offerings in terms of talking about and crafting solutions for customers will be paramount.”

Jeff Burgess, CEO of BCDVideo, Northbrook, Ill., offers a caution, though. “All we can do as a manufacturer is try to incorporate mechanisms within your build to make it harder to hack; however, some cybersecurity solutions impede system performance, such as drive encryption. We tested a number of these and the outcome was 40 percent degradation in system performance. That was too cumbersome on the system.”

Burgess explains that BCDVideo is releasing a two-factor authentication application that will come standard on its servers. Two PIN codes are added to the Windows Server login — one as a primary password, the other a randomized PIN generated by the paired smartphone app, giving integrators an added layer of security.

Tom Cook of Hanwha Techwin America advises dealers and integrators to use manufacturers as a resource. “The integrator is in the front line because the IT guy is going to come back to him and say, ‘Hey, how is this protecting my network? What are the things in this product?’ And they’re going to come right back to [the manufacturer]. So we’re going to take the lead.

“This industry needs to be smarter at [cybersecurity] because we are putting product on the people’s networks that have the capability of being hacked, and either you better make sure it can’t or you better tell them how to protect it so it can’t.”

Per Björkdahl, steering committee chair, ONVIF, says that while he doesn’t believe cybersecurity has become a standardized concept, it has become more and more of a demand from the user organization that the different products being deployed must be able to support a number of standardized features.

“The concept of cybersecurity consists of the three factors of people, products and processes. Unless you get all these together you cannot really provide this secure system because you can spend millions of dollars on securing your system, and then your password is compromised.”

Increasing Standards Versus Shrinking Privacy

As the security industry moves toward more connected, more open technologies, the necessity for standards has increased and likely will continue to trend toward openness and interoperability.

One reason having standards is important, says Per Björkdahl, chair of ONVIF Steering Committee, is it allows an end user, an integrator or a designer to be able to create multi-manufacturer or multi-vendor types of systems. “It’s a bit of a drawback if you have to go to one manufacturer to fulfill all your needs,” Björkdahl says, “and it also puts the end user in an awkward position to be locked in with one manufacturer. There’s also a bit of an issue for the VMS manufacturer; they have to support all the different models and manufacturers.”

Further complicating things, Björkdahl explains, “If you take a VMS company that maybe supports 200 manufacturers, and if you say on average, they might have about 50 camera models each, you very quickly realize that thousands of individual drivers need to be maintained. And if you can put that trust onto a standard, say [ONVIF’s] Profile S in this case, you actually free up a lot of resources that can be used for other useful developments of VMS.”

Björkdahl says it is becoming more or less expected that you can interface easily with any system, and therefore, the need for standards is going to increase.

One area Björkdahl says standards in the video security industry generally are desired is for the quick retrieval of information in a uniform format. “There is a higher and higher concern that you should be able to retrieve data from all the different systems in a logical, quick manner for forensic work, for what happened in Paris, for example — and the law enforcement people want to get hold of the video material very quickly and they want to have it in one format.”

Still, he doesn’t see this as a regulations issue; he says so far addressing these things to get a bigger or more homogeneous interoperability in export formats has been a job for standardization organizations, not for regulators or legislators.

“It’s a little bit controversial to ask for easier access to video material for the government. It’s a little bit 1984. While everyone understands that it actually helps in the bad situations, there’s always this mistrust — if there is too much information, what would happen with it? If it’s used or stays dormant, then fine. But if some looney gets his fingers onto that; what will happen with all that information?”

In Europe, for example, Björkdahl says the governments are restricted from allowing too much collection and storage of data. “But, on the other hand, I think the general impression by people is the benefit of having it is starting to be significant; their tolerance [of data collection] is improving.”

Sentiments toward the collection of information do seem to be shifting generationally, however. Björkdahl says, “It will really be interesting to look at the kids and how they look at this; what integrity means to the average 15-year-old is not the same as what it means to the average 45-year-old.”

The Evolving Customer

Although cameras will continue to be king because they are the backbone of any video surveillance solution, those in the security industry explain that customers have a more discerning eye than ever before in regard to weighing cost versus quality, and a greater understanding of the benefits that aren’t necessarily on the spec sheet.

“Customers are more educated and informed than ever before as to the value of a solution that offers everything needed for full flexibility and scalability, including seamless integration of existing and new technologies, even mixes of analog and IP networked solutions across multiple sites and to meet varied requirements,” says Keith Drummond, IDIS America. “They know what a low total cost of ownership is versus simply the cheapest product and they are ready to see and hear those numbers.”

Drummond calls these customers more value conscious and explains they want to know that they are getting features that actually increase their efficiency, performance, and ability to keep their assets safe and secure — not just drive up pricing. “They absolutely understand how ease of installation and use, and a lack of unnecessary license or maintenance fees, mean more money invested in the surveillance mission itself. That level of education and greater priority placed on value vis-à-vis new technology, even next-generation technology, has most certainly changed the game,” Drummond says.

According to Drummond, the industry is looking for “less flash and more cash.

“After a period of overwhelming ‘breakthrough technology,’” he continues, “the industry is savvier than ever about needs versus wants, and they are not spending money on new, flashy features and technologies they cannot fully utilize or monetize (through lower cost of ownership, cost avoidance, or operational/efficiency improvements).”

Drummond attributes this caution to a rash of products with big promises and few results. “There have been too many technologies that have delivered more in terms of marketing than they did in terms of performance, and the market is asking more questions, educating themselves more fully, comparing and contrasting offerings, and prioritizing both performance and value. We’re seeing a greater focus on the fundamentals of video surveillance and the ways next-generation technology can improve them: increasing resolution, increasing agility, increasing storage capacity, and ease of installation and use. And that’s what we’re focusing on internally.”

Wireless Technology Comes of Age

One driver of the expanding video surveillance market is the proliferation of wireless. A company that would like to install perimeter cameras but finds the installations too cost-prohibitive might take another look as prices decline, and the ability to install wireless cameras is allowing for just that, says Keith Jentoft, Integration Team, Videofied (a Honeywell Security and Fire company), Vadnais, Minn.

“Wireless technology is just making it easier and less expensive to put eyes in different places and have video. If cameras cost nothing, but it’s $3,000 to run wires out to the perimeter, it still doesn’t work, and with long-range, battery powered wireless, you don’t even need power cables.”

Jentoft says that customers who wouldn’t have considered putting a system in when the installation would have cost $10,000 would definitely put a camera system in if the cost to do so was in the hundreds, which is a much more realistic price point when installing wireless cameras.

The move to completely wireless cameras and the lower costs of cameras are dramatically increasing the number of applications, he adds. “Even on a Wi-Fi camera, you need power wires, and it’s the trenching of any wire that really drives up the cost.”

Jentoft says the industry is embracing wireless to a greater a degree than ever, and explains that Honeywell’s acquisition of Videofied is an example of a major player in the video surveillance market purposefully moving toward wireless. “Honeywell bought Videofied in March [2016], and while Videofied might have been a niche player, Honeywell definitely isn’t. Pushing Videofied [wireless] technology throughout their intrusion solutions was a key goal of that acquisition.

“People want eyes. Everyone is expecting video; it’s something that has changed in our culture. You expect to have video of an event, and now you have to explain why you don’t have it. And now that it’s inexpensive to put it there, you are seeing a lot of it go out.”

The Continuing Migration to IP

Alessandro Araldi, vice president global product management, Honeywell Security and Fire, says IP video continues to grow by double digits, whereas analog continues to decline double digits. “When you combine the two, we see the industry as a whole growing in the mid-to-high single digits,” he says. “We continue to see that as a trend for the years to come primarily because video — if you think about security as a whole, and then going beyond security to what we call connected building — we see video as being connected as a key to that.”

Larry Newman, Axis Communications Inc., says, “Twenty years ago Axis invented the IP camera and set off on a mission to shift the market from analog to IP, to the benefit of the end customer by offering more scalable systems with better features and higher quality. Twenty years later we are getting close to that goal, where the enterprise market is fully converged, and small and mid are not too far behind. That also means that the growth in IP cameras is decreasing, but still at a healthy level.

Sean Murphy, Bosch Security Systems Inc., says this continued migration is driving growth in the IP video category, while sales of analog systems are declining. “Bosch continued to strengthen its IP video portfolio in 2016 with new HD cameras for low-light environments, offering on-board video analytics as standard on more of our IP cameras, introducing cyber-secure IP cameras for mission-critical applications, and enhancing our Bosch VMS with new capabilities.”

Keith Jentoft, integration team, Videofied (a Honeywell Security and Fire company), says the increasingly competitive IP camera market means video management systems — how you feed that information to the customer — are becoming more important.

One thing is clear: dealers and integrators need to be well-versed in IP cameras and networks. Dealers and integrators can make a lot of money if they know what they are doing, Araldi says, and to do video well, they need to have a lot of IP expertise. “The traditional security dealer or systems integrator that maybe came from the access control or intrusion side are having some challenges, and basically they need to upgrade their knowledge and add new talents to become people who have those networking and IP capabilities,” Araldi says.

But don’t count analog completely out, says Dan Clinton, vice president, Clinton Electronics, Loves Park, Ill. “HD over coax offers a tremendous opportunity for dealers and integrators who have installed analog coax-based systems in the past. Since HD over coax is an ideal retrofit situation, dealers and integrators can tap their existing installation base and offer them an HD upgrade plan that allows them to keep their coaxial cable. By reusing existing coaxial cable, the installer significantly cuts down installation time and cost.”

So while there will continue to be a demand for analog for the foreseeable future, the market has certainly shifted to predominantly IP.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!