State of the Market: Fire Alarms 2017

Fire detection insiders are literally “fired up” over last year’s market performance and the potential going forward. While still heavily code-driven, there are signs of technology innovations and changes pointing to more integration and opportunity than ever before.

Ace Garcia of United Fire Suppression works on a fire install. Vice President Brent Blankinship says fire system sales in the first quarter are higher than they have ever been in the history of his company. PHOTO COURTESY OF UNITED FIRE SUPPRESSION

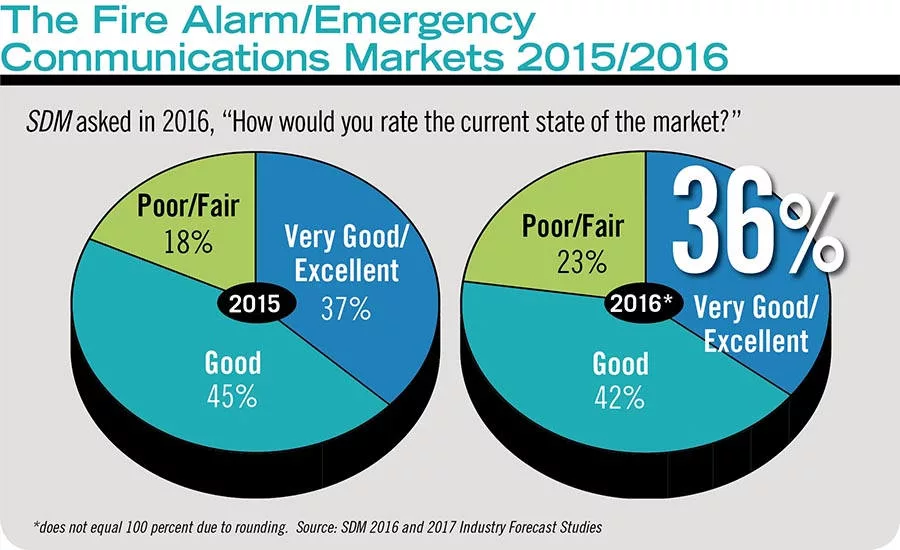

The fire alarm market outlook stayed relatively steady from 2015 to 2016 after a 10 percentage point jump in 2015 over 2014.

United Fire Suppression also increased its testing and inspection business in 2016. Above, tech Stacy Handy checks out a customer's system. PHOTO COURTESY OF UNITED FIRE SUPPRESSION

Roughly the same percentage of respondents think 2017 will be a good or excellent year for fire alarm sales as thought 2016 would be good, a characteristic of an inherently cautious industry.

Construction being up in 2016 and a general increase in code-driven business led to a positive outlook. PHOTO COURTESY OF UNITED FIRE SUPPRESSION

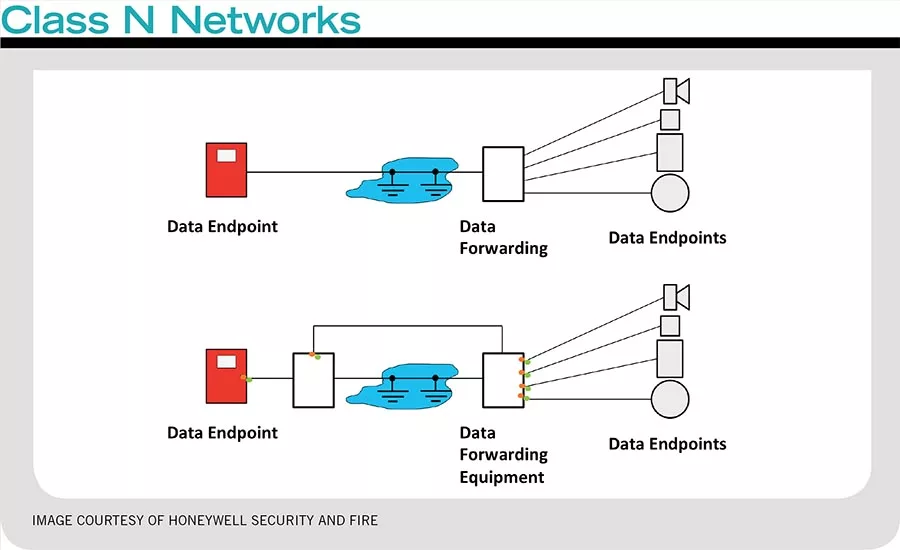

Allowing Class N networks was new for NFPA 72 in its 2016 edition and will potentially have far-reaching implications on the ability to integrate fire with other building and security systems. IMAGE COURTESY OF HONEYWELL SECURITY AND FIRE

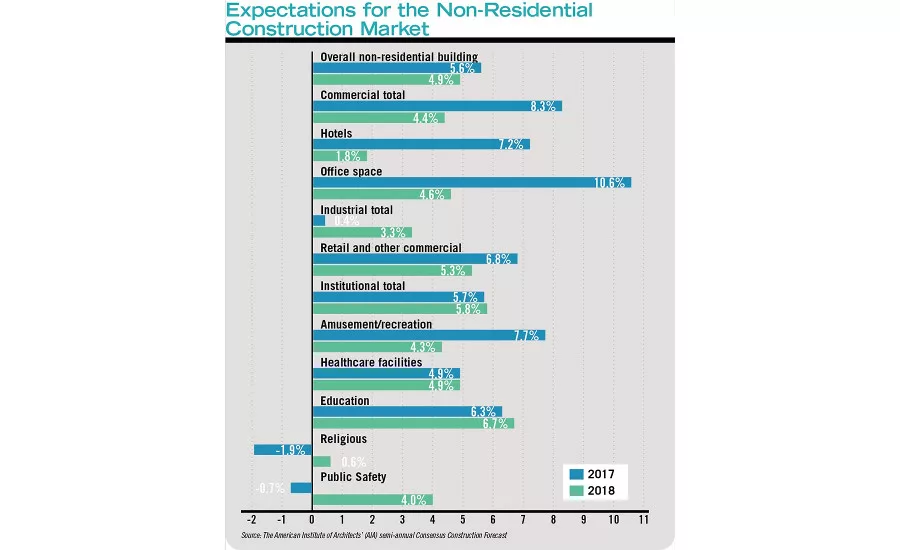

The American Institute of Architects’ (AIA) semi-annual Consensus Construction Forecast, a survey of the nation’s leading construction forecasters, projects that while spending will not equal the 2015/2016 gains, several sectors will stay steady and have positive growth.

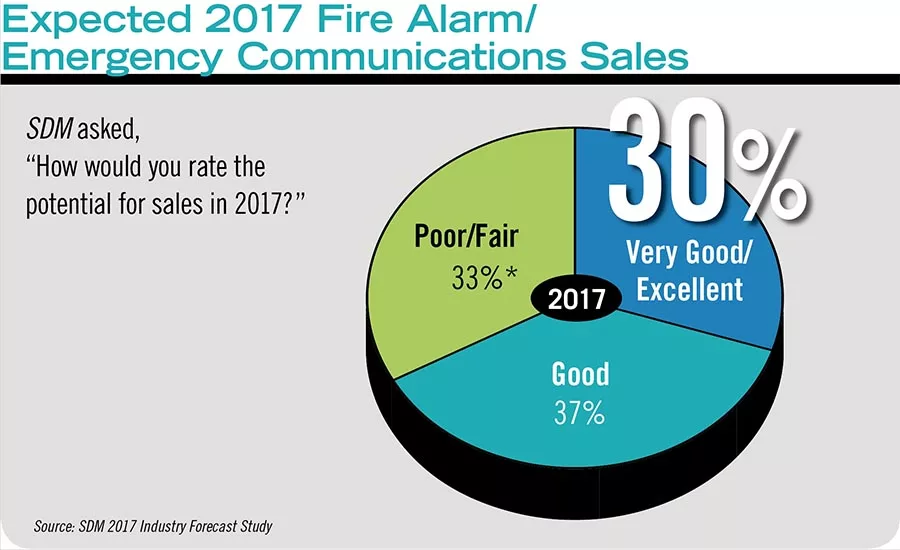

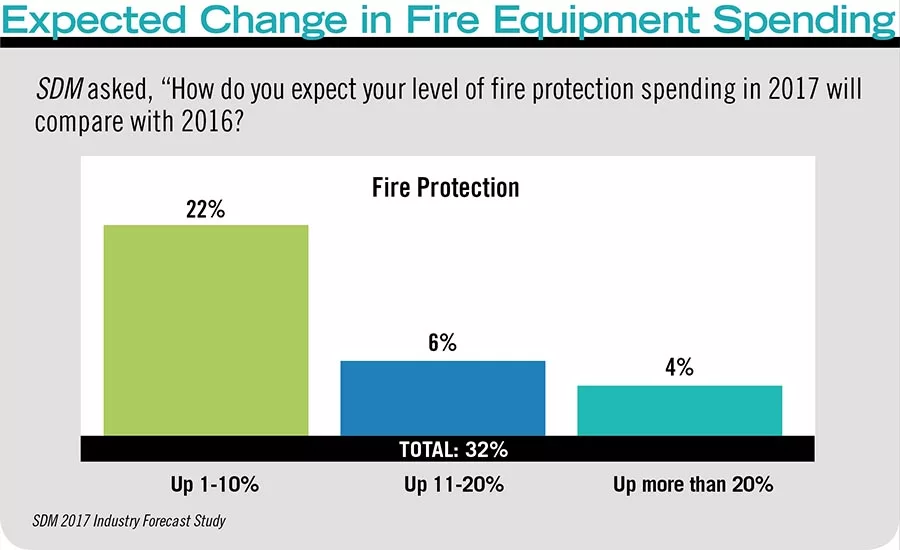

Thirty-two percent of respondents expect fire spending to be up in 2017, an increase of 5 percentage points over last year.

Anyone who thinks the fire alarm industry — with its restricting codes and standards and conservative outlook — doesn’t experience exciting changes, would be wrong. “Explosive,” “spectacular,” and “best year ever” characterized many of the responses to questions about growth in 2016 and the outlook for 2017 and beyond.

“Fire was explosive in 2016,” says security integrator Shane Clary, vice president, codes and standards compliance, Bay Alarm Company, Concord, Calif. “We had our most robust year ever in fire.” Clary attributes this in part to more aggressive marketing, but also to an improved economy overall.

Brent Blankinship, vice president and general manager, United Fire Suppression, Cabot, Ark., says his company made a concerted effort to go after more fire detection business, which paid off. “We have what I consider to be a few core businesses, but fire was up and I saw a shift away from some of the other sides towards fire.” Beyond sales, his company also increased its testing and inspection business, Blankinship adds. “I have four people that are doing nothing but selling fire alarm service and inspections.”

For many, 2016 was the continuation of a vastly improved 2015, Blankinship explains. In fact, numerically his fire detection business went down, but that was by intent. “From 2014 to 2015 we were probably up over 100 percent. That created issues for me because we had technicians that weren’t well trained and we were losing money on projects we shouldn’t have. In 2016 I actually brought the business back down by about 30 percent. Now in 2017 we are way up. Our sales in the first quarter are higher than they have ever been in the history of this company.”

SDM’s own research supports this assessment. The SDM 2017 Industry Forecast Study, conducted last fall, found that 78 percent of respondents characterized their 2016 fire alarm/emergency communications sales as good or excellent. This is compared with 82 percent in the 2016 study and 72 percent in 2015 (there was a 10 percentage point jump between 2014 and 2015). (See chart, this page.)

While characteristically cautious about predicting the coming year, the majority of respondents predict 2017 to be good or excellent. And 30 percent expect their equipment spending in fire detection to be higher this year. (See chart, page 87.)

John Garland, president of Garland Fire Systems, Hicksville, N.Y., says his business was up about 20 percent in 2016. “It was a little higher than the previous year. It was a good year last year. We have been growing every year.” He says he is aiming for the same level of growth in 2017.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

For manufacturers, 2016 ranged from “a good year” to record sales. Those focused on some of the hot-button changes such as carbon monoxide detection, and particularly new forms of communications now required as POTS phases out did best.

“It was spectacular,” says Brandt Phillips, commercial fire and security director of sales, Napco Security Technologies, Amityville, N.Y. “We had record growth, especially in the fire alarm cellular communication portion of the industry…. I can’t give percentages, but I can say it was an absolute explosion in 2016. The rate of adoption eclipsed anything we have seen in the past with any product line.” What’s more, he says, “I have every indication 2017 will be even better than 2016. We are releasing new products aimed at areas that have had issues with cellular. I would be shocked if we didn’t double the growth we saw this year.”

John Haynes, global director, Simplex product management, Tyco Fire Protection Products, Neuhausen, Switzerland, described 2016 as a “Goldilocks year — not too hot and not too cold. It was probably not as strong as 2015, but still positive.”

Potter Electric Signal, St. Louis, Mo., experienced double-digit growth in 2016, says Craig Summers, vice president of sales. He attributes much of this to advanced technology his company introduced, such as IP-enabled panels, and intelligent detection.

Doug Hoeferle, product marketing leader for hardware and edge devices, Honeywell Security and Fire, St. Charles, Ill., characterizes 2016 as a great year. “The fire business was very strong…. Our expectation for 2017 is we are feeling optimistic. We expect it to be better than 2016 but 2016 was much better than 2015 so I don’t know that it will grow quite at that level.”

According to a few market studies, growth in the fire industry looks to continue its climb. A Markets and Markets report on the global fire protection systems market, forecasts a CAGR of 10.1 percent between 2016 and 2022, resulting in a market worth $98.24 billion by 2022.

Another report, from Micromarket Monitor, which breaks the market down in several different ways, found that the North American fire protection systems market will reach $18 billion by component and $10 billion by service by 2020. The active fire protection systems market in the U.S. is projected to grow at a CAGR of 6.2 percent, while the passive market will grow at a healthy 12 percent GAGR to reach $13 billion by 2020, according to the same study.

Overall, there is a sense of excitement about the fire industry this year. With recent changes to codes and standards that require some new technology in various locations, an increase in new construction and hints at easing the way to more integration, the future looks very rosy.

“The fire alarm control industry is not as glamourous as consumer technology but that is not to say there isn’t innovation going on,” says Neil Lakomiak, business development director, Underwriters Laboratories (UL), Northbrook, Ill. “There is quite a lot; we are very excited about it and trying to help it get to market.”

DRIVING FORCES

At its core, the fire protection market is still and always will be code-driven. So much of the positive reports on sales can be attributed to new construction, renovations and upgrades that require new fire equipment.

Clary says new construction was one of the big factors in his company’s growth in fire last year. “We are seeing a bunch of new construction. We have a number of systems already sold that are for sites that are still a dirt lot.”

Construction is up in Arkansas as well, Blankinship relates. “I can tell the difference because it is code-driven, so if they are building we are putting in fire alarms. Our other business that wasn’t code-driven was down, which reinforces the theory that code-driven things saw an increase.”

“Fire was explosive in 2016. We had our most robust year ever in fire.” — Shane Clary, Bay Alarm Company”

According to research completed in late 2016 by Jones Lang LaSalle IP Inc., “Modest but steady growth across all sectors in Q4 capped off a record-setting 2016 for the construction industry.” Spending rose 4.5 times higher than end-of-2015 levels to nearly $1.2 trillion. The American Institute of Architects called 2016 “a chaotic year for non-residential building activity.” In an article on its website projecting more growth for 2017, author Kermit Baker wrote, “Construction levels surprised many on the upside this past year, particularly for most commercial categories. According to current estimates, spending on offices increased more than 20 percent in 2016, hotel spending was up about 25 percent, and even retail and other commercial facilities saw growth of about 10 percent.”

Existing facilities are also being upgraded. “The greater enforcement of code requirements and the greater embracing of the fire alarm and life safety changes to these fire alarm and building codes will continue to grow the fire alarm industry,” says Wayne Oliver, vice president of sales and marketing, Hochiki, Buena Park, Calif. “I see less tolerance for older, malfunctioning fire alarm systems than ever. This increases the opportunities for the negotiator sellers to provide a solution to these older failing systems.”

As facilities are built or renovated, the latest fire protection technology gets implemented, and today that means addressable panels and end points. While addressability is not new, it is now the standard, and a critical step toward increased functionality and integration.

“I think probably the biggest innovation [in technology] has been in the areas of addressable notification products,” Haynes says. “We recently launched addressable voice systems, which provide benefits both in terms of functionality and testing and maintenance. Every notification device has an address, which means any fault in the system we immediately get a trouble condition.”

Richard Roberts, industry affairs manager, Honeywell Security and Fire, St. Charles, Ill. adds, “In the past you could install three to four pull stations and a half dozen detectors all in one zone. It would be very difficult to find out which device actually went into alarm. The 2015 edition of the International Fire Code (IFC) requires all new systems to identify the specific type of device, its location or if it is an alarm, trouble or active condition. It doesn’t use the term addressable, but it is essentially that.”

This is one of several new requirements that have come into play with the most recent codes and standards that have expanded the market. For example carbon monoxide (CO) detection is now required in sleeping rooms, including hotels, dorms, and multi-family dwellings. One of latest locations to require these detectors is K-12 schools, already a booming market in many areas for security as well.

“There are new requirements in the IFC for CO detection for new schools that have a permanently installed fuel appliance or attached garage,” Roberts explains. California, Connecticut, Illinois, Maryland, New Jersey and New York all have laws requiring CO detection in K-12 schools, he explains.

CO requirements of some sort are currently in place in all but seven states, according to the latest information from Honeywell, and this is boosting business for dealers and integrators, Hoeferle says. “Integrators are going back and adding CO detection to those systems and connecting those sites to central monitoring stations and that has driven business as well,” he describes.

That is true for Garland’s business. “We are in New York and CO detection has become very important because it is required on new projects. We did a lot of upgrades, putting it in all new buildings.”

New York is one state that has been particularly aggressive in CO requirement adoption, Summers adds. “We are seeing significant growth in system CO detection, especially in areas such as the state of New York where they have adopted codes requiring more CO detection in existing buildings. Potter’s new addressable CO detector was developed with this market in mind.”

Another technology getting a lot of attention in K-12, campuses and elsewhere is emergency communication and mass notification, which is often (but not always) tied to the fire system. This technology is perhaps unique in that it may be one of the few fire and life safety-related technologies that are starting to be adopted outside code requirements.

“On the new construction side of the business, we see dealers and integrators leveraging our emergency communications to provide solutions above and beyond what code requires,” says Tim Baker, director of marketing, small and medium businesses, Honeywell Security and Fire, Melville, N.Y.

Lastly, dealers and integrators are seeing more need for testing and maintenance services, says Todd Jackson, senior director, sales operations, Tyco SimplexGrinnell, Westminster, Mass. “There are different needs for services than in the past. If their level of code adoption has changed, that will dial up what kind of services and coverage they need.”

All of this spelled opportunity last year and will continue this year, Baker says. “The biggest opportunity this year is around continuing to capitalize on code changes that are taking hold. CO requirements, low-frequency sounders in commercial sleeping spaces — even the move from conventional to addressable fire systems — provide great opportunities to provide customers with more effective life-safety solutions while helping them to comply with current codes and standards.”

LOOKING AHEAD

As enthusiastic as many are about the past year and what is to come in 2017, there is also a level of excitement about the possibilities a little farther down the road. With the groundwork being laid now by technologies such as addressability and network communications, could fire detection expect big changes like some of the other security technologies have experienced?

“I think it will catch people off guard,” says George Bish, chair of the ESA Standards Committee, Dallas. “They don’t expect it will affect fire, but it is. Fire has been in its own bubble and the same evolutions that those other industries have gone through will also hit fire. We just have to figure out how best to handle that because fire is more code-driven, but it will come. It will be gradual, but I think that with the 2016 [NFPA 72] standard that now allows for class N has opened the box.” (See “Pandora’s (Networked) Box” online at State of the Market: Fire Protection 2017)

It is already happening, according to Lakomiak. “We have seen new innovations. With our traditional customers we have begun to see more new products and systems from them with new technologies and we are also seeing new entrants into the market. Things like smart buildings, although not coming as fast as smart homes, we are seeing more companies that were not traditionally part of the fire alarm control industry get into the business. They are looking at smart systems and how to integrate fire, security, lighting, HVAC and leverage the data that is coming out of them. We are working with several startups that have very different ideas of what the future looks like. It is definitely a more connected future and a desire to integrate more building systems together.”

“In 2017 we are way up. Our sales in the first quarter are higher than they have ever been in the history of this company.” — Brent Blankinship, United Fire Suppression

However, Lakomiak acknowledges it won’t necessarily be easy, precisely because of the codes and standards in place around fire. “The fire industry has generally moved fairly slowly and there are a variety of reasons for that. It is very code-driven and when you have a code cycle every three years, that is the cadence you are on. Even across those three years you rarely see huge jumps in technology. There has been a tendency to feel comfortable with the performance of these systems, which has proven out over the course of time. What will be the catalyst for change in the fire alarm industry is data and the ability to get smarter about not only detecting but potentially even preventing fires. Think about a day where you don’t have worry about detecting fire if you can prevent it in the first place. There will be interesting products and services in the coming years that will attempt to do just that.”

The recent merger between Tyco and Johnson Controls is already having an impact on the way SimplexGrinnell and Tyco Fire Protection Products think about fire, Haynes says. “We have products on our roadmap and ideas about connected buildings in the future. We have a number of building blocks on both sides of the companies so there is active work underway to integrate that. We are going through the process of seeking voice-of-the-customer input, so I think it is very likely to see some innovations along those lines in the next few years.”

Honeywell’s Hoeferle also sees this as the path forward. “I absolutely see fire as part of the smart building. I don’t know when, but fire systems are sort of a grudge purchase and what we have seen with the emergency communications systems is people look to leverage what they already have when they are trying to do something else so they don’t have to buy a separate system. If you have a hotel room, you have a smoke sensor in there; but there are other needs that can be addressed in that room. What is the humidity or temperature or other information that could feed into other systems? Maybe they don't want to buy two sensors but they have to have a smoke detector, so why wouldn’t you add all the smarts into it? I think it’s kind of exciting to think about how those systems can work together in the future to save lives or money or make people more comfortable — all those things a connected system could do.”

Hoeferle adds that Honeywell’s top tier detectors look for elements of CO in the air, have a photoelectric smoke chamber looking for smoke particulates, thermal for temperature and IR that looks for light changes to see a flame. “There is a lot of data and value there and I feel like it is trapped and could easily be used in a broader context,” he says.

“The technology we have now is amazing,” says William Burke, division manager of electrical engineering, NFPA, Quincy, Mass. “A smoke detector goes off and instead of telling the fire alarm system ‘I see a fire,’ it activates five different devices that do other things…. There are a lot of things happening with central station type systems where … rather than just have one alarm, more and more are going to ‘it is a fire on the third floor on the east side of the building and I think it is the HVAC unit. There are point-to-point and multi-point distribution systems. I expect to see that more and more.”

Blankinship sees wireless playing a larger role in the future of fire detection, as well. “As that technology evolves and you can actually do a full wireless system, I can see that making a change. I think you will start seeing more wireless. When we still have to have notification devices wired there was a limitation and they didn’t do much good. Now that you don’t have to wire horn/strobes I see it making a push, particularly in historical buildings.”

Video is another promising technology that could have a major impact on the fire industry, Bish says. “We are still trying to figure out how to best use video. Being able to put one camera in a large area and see smoke that is only four feet off the ground before it even reaches a detector [is exciting]…. It is currently being utilized but still on the high end. I see it coming down into the everyday supplemental systems because video is everywhere now.”

An emerging fire detection technology is also in the works from UL, Lakomiak says. Multi-criteria detectors can detect the type of smoke and the material that is burning (for example, plastic versus a piece of toast). “There is a four-year effective date to bring products into compliance with the latest requirement,” he says. “By May 2020 companies selling products with the UL mark need to comply with the upgraded standard.”

“We are seeing a faster adoption in jurisdictions and much more forward-thinking AHJs in general.” — Brandt Phillips, Napco Security Technologies

Many in the codes and standards arena point to technology changes already increasing, much as they are in the rest of the industry and the world. “Technology is forcing the codes and the acceptance of technology to speed up,” Bish says. “We don’t have a choice. The lifespan of the equipment being made … is no longer the five to 15 years. As the ability and the technology changes, we have to change the codes to keep up with it, but at the same time make sure we don’t lose sight of our No. 1 priority, which is life safety.”

As technology speeds along, new products will hit the market a lot faster, Lakomiak predicts. “Let’s say the runway from new product development was 18 months to two years, when you get to the point where it is a year or less, I think if the industry is prepared to understand that, it will help. There will need to be some consideration for how we develop codes, possibly. Most people want to avoid preventing a new technology from getting to market if it will save lives. We have realized that ourselves and upped our game as a testing and certification organization.”

Technology changes are and will continue to happen, Bish says. “People need to stay up with technology and just realize that the new technology keeps coming at us faster. If you don’t stay up with what today is cutting-edge technology as a businessperson, you will be behind the curve, because it will be mainstream before you know it.”

Check out more SDM State of the Market Reports

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!