State of the Market: Fire Alarms 2018

With a strong economy, plus a healthy new construction and retrofit market, business remains steady in the fire space, with a few new opportunities, but also some notes of caution

With the security industry dominated by swift change, the fire alarm market can be a “safe haven” for many security dealers and integrators who either specialize or include fire detection in their stable of offerings. Code-driven and mandated, fire is more of a “sure thing” as long as you maintain quality business practices, a respectful relationship with the local authority having jurisdiction (AHJ), and a continued showing of value to your customer as to why they should choose you over a competitor.

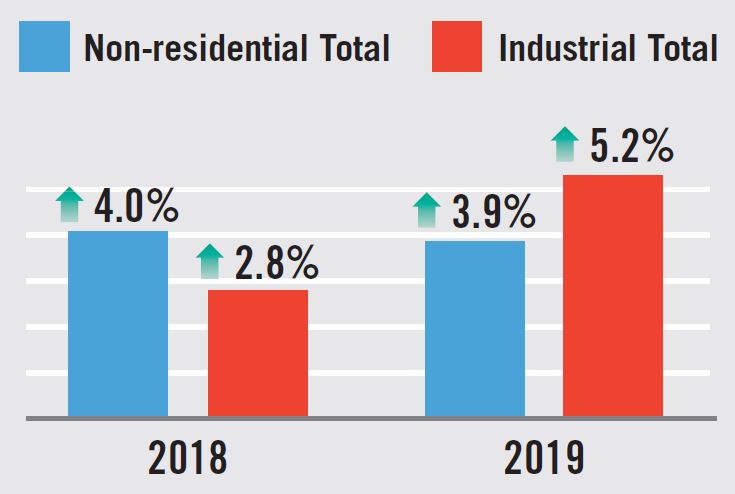

Accordingly, nearly everyone interviewed for this article reported that 2017 sales were at least steady if not significantly higher than 2016. Why wouldn’t they be? In an economy that is staying strong, with a projected commercial construction growth rate of 4 percent annually through 2019 (see chart on page 81), there is much to be satisfied about.

The American Institute of Architects (AIA) in January 2018 projected a “modest pick-up in the growth rate and another solid performance in 2019,” citing five main factors for optimism in the building and retrofit market: rebuilding and repairs from natural disasters; tax reform implications for construction; a possible infrastructure package; strong consumer and business confidence levels; and leading economic indicators for the construction sector. That is good news indeed for the fire detection market.

“We’re continuing to see further improvement in commercial construction starts, spend on R&D, and a general optimism about the state of the economy,” says Neil Lakomiak, director of business development for UL’s Life Safety Technologies business, Northbrook, Ill. But it isn’t all the economy, he adds. “We perceive the fire alarm industry in 2017 performed slightly better than 2016. This is, in part, based on the increase in the number of new products that were submitted to us for UL testing and certification.”

New technologies are definitely a part of the story, particularly when it comes to communication paths, says Judy Jones-Shand, vice president, marketing, NAPCO Security Technologies Inc., Amityville, N.Y. “NAPCO performed well in the traditionally stable 2017 fire market; it is, in fact one of our fastest growing market segments. We introduced several new products for fire alarm system dealers and integrators.” One of the hottest items was the company’s universal dual path cell and IP-based fire communicator line, due to significant and fast changes in the communication side of the business, she adds.

Potter Electric Signal, St. Louis, Mo., noted “very strong double-digit growth” in 2017. Dave Kosciuk, executive vice president and general manager, fire and security division, attributes this in part to the economy and overall construction market and in part to technology advancements Potter released. “Our products are all IP-based,” he says.

Honeywell also reported “another strong year,” according to Samir Jain, general manager, Honeywell Fire Safety Division, Americas, Honeywell Home and Building Technologies, Northford, Conn.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

“Fire is a great industry compared to security,” he says. “The difference is it is so code-dependent. We love that you have to have a fire system. You don’t have to sell on having it, just which one to buy; and it has a good RMR model to it.”

And integrator Red Hawk Fire & Security, Boca Raton, Fla., experienced strong double-digit growth, says Senior Director of Marketing Michael Lohr. These impressions are in line with responses to SDM’s 2018 Industry Forecast Study, conducted in November 2017. When asked about the current fire alarm and emergency communications market in 2017, 78 percent of respondents said it was “good” to “excellent,” with 40 percent placing it in the “very good”/“excellent” category (up four percentage points from the previous year and significantly higher than the 67 percent that predicted it would be strong). In addition expected spending on fire equipment also rose 10 percentage points over last year, with 43 percent expecting to spend more in 2018. But this number could also indicate increased costs along with an increase in sales.

Along with the optimism there is an underlying sense of caution in the fire market, in part tied to fears that the economy may not continue to be as strong as it has been (despite no indications of this yet), along with margin pressure and other possible dampers.

“We did more work in 2017,” says integrator Jeff Bradshaw, president, Intercept Control Systems Inc., Edgewood, Wash. “But it looks like the jury is still out on whether we made the same amount of money. Costs have increased. A lot of projects have been in the works for a handful of years and it is a dance to keep up with current pricing.”

Industry Drivers & Opportunities

From standards and codes, to the obsoleting of copper phone lines and a sudden interest in in-building communication, there are definitely some important drivers in the fire alarm market this year. But nobody wakes up one morning and decides to buy a new fire detection system.

“Obviously the fire side of the business is code-driven,” Lohr says. “End users are buying what they have always bought — smoke detectors and heat detectors.” However, he notes, there is more emphasis on carbon monoxide (CO) detection now.

According to the National Conference of State Legislatures, “As of March 2018, a majority of states have enacted statutes regarding carbon monoxide (CO) detectors, and another 11 have promulgated regulations on CO detectors.” In addition, 14 states require them in hotels and motels and five in schools.

This is an issue that the National Fire Protection Association (NFPA) is trying to bring to national attention (see “What’s New With NFPA 72?” on page 76) and will be an increasing business driver for any fire dealer or integrator that installs in facilities with sleeping rooms — “anyplace with a pillow.”

“When you talk about extended care or hospitals they buy every single product and service related to fire and safety,” Lohr says. “They just do. They have a huge responsibility to the patients and that is one of the biggest markets for us.”

Bradshaw, too, points to an increasing focus on some of these markets. “There is an aging population and a big need for quality, affordable housing for them. Retirement facilities are going up.”

Lohr and others also say technology updates such as wireless and addressable systems are another potential market boost. “Sometimes it is born out of frustration where an end user has had it with the zone system and not knowing which device is giving the problem,” Lohr describes. “That does drive retrofit business.” The new tax bill may help tip some of these types of customers over the top, he adds.

“It stands to reason that it would help sway some people’s decisions,” Bradshaw agrees.

Wireless is another topic coming up more often, says Eric Elsenbroek, director of global technology services, Anixter, Glenview, Ill. “The adoption of wireless systems will likely rise in 2018 as these systems become more flexible and robust. Traditional fire panels are now becoming available with wireless technology built in.”

Honeywell’s Jain agrees. “We have seen a big interest and wireless is a big differentiator,” he says.

Indeed, according Data Bridge Market Research, the global wireless fire market was $220 million in 2016 and is projected to grow at a combined annual growth rate of 8 percent from 2017 to 2024.

One of the newer developments is radio repeaters inside of buildings for first responders that want to use their own radios for communication. “This is a new adjacent space,” Jain says. “It is great for dealers to get in because it is so similar to fire, and we are launching an offering to help our dealers.”

Jain adds that this technology is starting to be required by some codes, but it is also something building owners want.

Shane M. Clary, vice president codes and standards compliance, Bay Alarm, Concord, Calif., says his company has started seeing an uptick in the radio amplifiers. “They have been in the code for several cycles, first starting with high rises. Now they are starting to drive to all buildings.”

UL, too has noted the emerging trend. “Revisions over the past few cycles to the IFC and NFPA 1 strengthened requirements regarding in-building signal strength coverage for existing public safety communication systems in both new and existing buildings,” Lakomiak says. “This is resulting in an increase in the number of buildings incorporating emergency radio communication enhancement systems. UL recently published UL 2524, ‘In-building 2-Way Emergency Radio Communication Enhancement Systems,’ to address industry requests for certified equipment.”

Perhaps one of the biggest boons to the fire industry both last year and moving forward was that phone companies such as AT&T and Verizon announced the end of support for copper phone lines, or POTS (plain old telephone service).

“The fire alarm industry has been transitioning more to IP and radio communicators as more Bell companies canceled POTS lines,” says Keith Daum, director product marketing, Anixter.

“We see the demand for commercial fire alarm cell/IP communicators to be here to stay and steadily rising for the foreseeable near future, since most of the millions of commercial fire alarms in the U.S. are currently communicating on old-fashioned copper land lines,” Jones-Shand adds. “Even though the traditional fire alarm market has often been one that is slower to embrace change or ratify new technologies, the switchover to cellular/IP is happening right now, with full compliance and sanctions of NFPA, UL and regional regulatory bodies. The rate of adoption and immediacy was hastened as phone companies are routinely ‘retiring’ countless thousands of POTS lines throughout the country ... every day.” (See “Making the Most of the Demise of POTS” on page 80 for more on this subject.)

Notes of Caution

There are more reasons to be excited about the fire alarm industry than ever. But there are also some notes of caution from dealers, integrators and manufacturers.

For example, while the POTS demise may be a driver for some customers, others see no need to change anything that isn’t strictly necessary. “It depends on the situation,” Lohr says. “If they have a fire alarm system that is 30 years old on a POTS line and they are looking to upgrade communications, that is one thing. But if they haven’t had any problems, they may think they are fine with the slave communicator.”

When it comes to fire detection, customers still need a good reason to change it out — it is almost never on a whim. “It is a great industry but sometimes people have a functioning system and no reason to change,” Jain says. “Copper lines are going away, but we have mostly addressed it. The actual system — the panel and devices — people say they still work. They are grandfathered in so there is no absolute need to upgrade. We do still see a demand to change out here and there. But nothing forces it to get changed.”

In fact, there may be more incentive not to change out systems, when it comes to fire and life safety codes, Bradshaw says. “There is an ‘If it ain’t broke don’t fix it’ attitude because many times if they do break down, now you have to bring the whole building up to code. There is more of an incentive not to change it because if they do, it will cost them.”

Another thing that hasn’t hit the fire market as hard just yet, but will as systems increasingly become integrated, is the issue of cyber security. “It’s not so much a problem on the older systems,” Lohr explains. “But on the newer ones it is. ... Newer smart systems are more vulnerable.”

Jain agrees, adding, “There is tremendous concern for cyber. If you think about what a fire alarm system is, it has to be working all the time. Cyber crime could come in and disable a fire alarm system by falsely turning it on, for example.”

Both NFPA (with its new Class N) and UL are addressing cyber security in their codes and standards. “UL’s aim is to help enable these new technologies,” Lakomiak says. “Cyber security is a growing concern as more products and systems become integrated and connected to the Internet and each other. UL’s work in this area includes supporting manufacturers, installers and end users in mitigating risk as they continue to innovate. One example is the new UL 2900-2-3 for cyber security specifically geared for this industry.”

This is one reason some integrators like Clary are still reluctant to go the IP route. “We have been asked, ‘Can you put it on our network?’ but we generally prefer not to. It is mainly because if something goes wrong there is finger pointing. Even if the capability is there, we would prefer not to do it.”

Perhaps the most nebulous cautionary note involves the economy. As things have been going along well for a few years now, some are starting to get a little nervous. “If you talk to our marketing department, 2018 is going up; so far every year has been up,” Clary says. “However, I’m always cautious. I have a doctorate in economics. Somewhere out there we will have a downturn. I can’t tell you when and I don’t think this year, but within the next five years. We can’t keep going up and up.”

It’s almost as if some in the industry feel it is too good to be true, Clary adds. However, he also stresses that there is nothing obvious to cause worry. “Our workload has not at this point leveled off. In fact, we are adding designers to keep up with the backlog.”

Kosciuk echoes some of these same sentiments. “The economy is what keeps me up at night. Because it is so robust now and there is a lot of construction going on, we are looking at that as our opportunity. If the construction market blows up or goes away that would impact what we are trying to do going forward.”

While the economy is a caveat for Bradshaw as well, that isn’t his immediate worry. Rather, he is concerned by some of the trends he sees in the industry, particularly ones that require more specialized knowledge. It is a double-edged sword, he says. “NICET certification requirements are a good thing because they weed out the chaff. But everything comes with a cost. I see us spending a lot more time in class and less time in the field. It will change the way we approach projects in the future as a result.”

Still, he too feels the slight hesitance to celebrate the strong market today. “I don’t know if it is a sense of caution. I think it is becoming so much busy work just to keep up with changing requirements, trends and codes. There is so much to do and it seems like there is a lot more work to achieve the same result. Yes we did more work, but it took a whole lot more work to do that more work. It is very management-intensive.”

Daum sees some of this from his perspective as a distributor. “The fire alarm category is not as volatile as others. The challenges continue to be education and margin pressure, based on other low-voltage technologies.”

2018 & Beyond

The fire alarm space may frequently operate on a parallel track with security, but it certainly doesn’t exist in a vacuum. Even with its restricting codes and more difficult sell outside of what’s mandated, fire companies are looking at many of the same future trends as security — from cloud to integration, mobile and more.

“Being an integrator we sort of look at fire alarms and security being tied together, which they are, but it is about a 50/50 split in our company,” Lohr says.

Lohr points to the recent Parkland, Fla., school shooting (where the shooter activated a fire alarm pull station to evacuate the students) as an example of why end users are increasingly looking at marrying fire, emergency communications, and other systems for greater safety. However, he acknowledges there are hurdles. “I do think we will see more and more integration, but it will be more of a push than a pull. The manufacturers are going to start pushing this out into the marketplace.”

The greatest integration in the fire market is happening between mass notification and fire alarm systems, Anixter’s Elsenbroek says. “The need for notification and strong intelligibility and clarity continues to drive demand. Strong intelligibility allows you to manage all audible and visual notifications for all fire and mass notification systems.”

Jain sees the ubiquitous mobile phone having a greater impact on the fire market going forward. “In the security alarm industry it is all smartphone based. You can’t do that in the fire industry because it is code mandated. But what you are seeing is people wanting to monitor their system [using their phone].”

He, too, sees integration on the horizon, but slower than hoped for. “We’ve been saying for four years or longer that systems are all becoming integrated. That is part of the reason [Honeywell] connected security and fire. We still think that is a vision for the future, but it is not moving nearly as fast. Yes, there are opportunities and people talk about the idea. But ... the value proposition is not as strong as people initially thought.”

Building automation and IoT are trends Mircom believes will impact the fire market in the future, says Michael DeMille, vice president, marketing and product management for the Ontario, Canada-based company. “Building automation and integration is an emerging request,” he says. “In some cases this is challenged by existing fire codes and standards.”

Chris Miers, regional marketing manager–fire for Bosch Security and Safety Systems, Fairport, N.Y., also sees a place for cloud in the future. “Cloud-based processing of data ... will allow for added benefits to a business. These benefits can include faster response to business needs, lower costs and the ability to scale easily.”

Those types of benefits are part of why Kosciuk is fairly bullish on 2018 and beyond, with Potter’s IP-based approach. “We see 2018 and the next five years having tremendous growth opportunity. ... Being able to integrate different control panels to the head end allows the end user to see multiple buildings locally or worldwide. Let’s say I’m a building owner or property manager with 100 buildings. I can see every single one, what is going on, if there are any maintenance issues and anything that you want to hook up through IP-based software. It’s really more about value-add information out of the system to help offset other expenses.”

Bradshaw agrees. “That seems to be a trend. Everyone wants everything IP. They are working on it, but to see a whole [fire] system IP might be a ways off. Everyone wants everything to be integrated, but in fire, not anything more than what has to be integrated by code.”

He adds, though, that his company does anticipate being very busy in 2018 and beyond. “There isn’t the stress we have all had from time to time making sure we have enough work. That hasn’t been a problem for quite some time.”

What’s New With NFPA 72?

One of the most influential codes in the fire industry is NFPA 72, a document that is updated every three years. Richard Roux, senior electrical specialist, staff liaison for NFPA 72 (National Fire Alarm and Signaling Code), NFPA, Quincy, Mass., says this is the final year of the cycle.

“This is the climax of the third year, the end of the process,” he says. “We will release the 2019 edition. It prints in September and then it will come out for the public to use.” While there are still a few items left to pin down at the annual NFPA Conference, to be held June 11-14 in Las Vegas, many of these changes echo the drivers those in the industry are hoping to see. Roux highlights the top four changes that are of “extreme importance” to the fire industry:

1. CO Detection. The standard for installation of CO detection, NFPA 720, is being retired. “For the past three years committees took all those requirements and properly placed them into NFPA 72, which has worldwide acceptance,” he says. “In 2005 there were 61,100 non-fire CO incidents fire departments responded to. From 2006-2010 the average per year was 72,000. That is why NFPA felt strongly that this obscure document (NFPA 720) needs to be moved to the more well-known NFPA 72. “This is the number one item on the list of changes,” Roux says.

2. Reducing residential false alarms due to cooking. Smoke alarms are required in nearly every house in the U.S., yet many don’t have them, Roux says. “The reason is smoke alarms are a big nuisance to a lot of people. There is new testing that will make detectors more resilient to cooking smoke. So as of January 1, 2022 all new smoke alarms will have to pass this new test.”

3. IP, PoE and Cellular Communications. Roux explains: “There is no automated means of communicating with the fire department. Very few fire departments want a call from individual buildings. You have to go through a monitoring facility. That worked fine for a while, but technology is changing now and fire alarm systems are sending old signals. The code has changed every three years to adapt to the new technology such as Poe, IT, Ethernet, and cellular. Now one of the final pieces in 2019 is a final adaptation to this to allow newer technologies to be that communications means between the fire alarm system in a building and monitoring stations.”

4. Class N (networks). Owners want to user Ethernet and the Internet of Things, Roux says. “They want a pull station to be a thing where they can use the PoE infrastructure. So we have made major changes in class N dealing with building infrastructures other than fire alarm system wiring.”

Roux concludes, “People who do alarm stuff need to be aware that the 2019 edition is hitting the streets. There are a lot of changes and they need to find out what they are.”

Aging Out

It’s not just the fire alarm systems that are getting older. Like much of the rest of the security industry, fire alarm dealers and integrators note the increasing difficulty in finding and training employees. But the fire industry has an additional battle — attracting younger employees to an industry that doesn’t often play with the newest, coolest toys and requires a lot more certification and knowledge to do it.

“One of the biggest issues I see is the loss of expertise of the people who are retiring,” says Red Hawk’s Michael Lohr. “With fire alarm systems you can have one that goes for 40 years without any problems, but then only a couple of people who know how to work on them and one is about to retire.”

Hiring new technicians to work on these systems is a constant battle, he says. “So many companies are competing for the same talent.” Then when younger technicians are faced with the older technology it can create a different set of problems. “We have a gentleman who was in the Battle of the Bulge and is still working for us at age 88,” Lohr says. “Another one just turned 80. We can’t depend on those folks being around forever. And the last thing a customer wants to hear is some 22-year-old kid scratching their head saying they have never seen this before because it came out before they were born.”

One tactic Lohr’s company is trying is to sponsor scholarships and apprenticeships at local high schools and colleges. “We are looking at that as a way to groom those folks.” However, he says, there is also the need to put some pressure on the customer to upgrade to technology that can be serviced more manageably, as well.

Shane M. Clary of Bay Alarm Co., says software compatibility can be a particular issue with older systems. “We have older systems that were put in 20 years ago or more. Who has the software for this? Who has a laptop that can even work with this system?”

Clary also sees the age issue happening on the code development side. “There are only a handful of us in the industry that are active with code promulgation and we are all in our late 50s or 60s. I am not seeing the industry putting in the resources to get younger people trained so that when we retire they can pick up the slack.” If that doesn’t happen, he says, it could cause bigger problems. “We could start seeing reductions in codes and stuff being pulled out of the code, and we could see the market share of fire alarm start to drop.”

Intercept Control Systems Inc.’s Jeff Bradshaw says he has found it easier to attract talent to the “techie” stuff like video and even access control than fire. But perhaps there needs to be a new way of thinking about it.

“Fire protection is regulatory driven and code driven and there is a lot more certification required and documentation that the other areas don’t have,” he says. “It is easier to get people here doing stuff they like messing with.” But, he notes, while fire is more work to become certified, it can command more money as a result.

Making the Most of the Demise of POTS

New ways of getting the fire signal from the protected site to the monitoring facility are a hot topic in recent years, with the phone companies stepping up their phase-out of copper phone lines, or POTS. This can be very good news for dealers who are able to take advantage of it.

“As telecom companies replace copper phone lines with newer technologies, fire alarm systems that use landline telephone technology and digital alarm communicator transmitters (DACTs) to monitor fire alarms system activity are being impacted,” says Bosch Security and Safety Systems’ Chris Miers. “With the approval to allow newer communication technologies ... to act as the sole path for fire control panel communications, as well as less stringent supervision requirements, there are new opportunities for dealers to upgrade existing fire panels installed in the market. Upgrading these systems to communicate over IP or cellular enables the end user to eliminate the costs associated with up to two dedicated telephone lines per panel, and creates a new recurring monthly revenue stream from data services plans for the dealer.”

This has been a popular path for NAPCO’s dealers, says Judy Jones-Shand. “Our communicators are based on the technology of our [intrusion radios] and they share the $100 trade-up incentive as well. ... Also our communicators are universal, so a dealer can use it with his or her favorite alarm panel brand and send alarm reports to his/her favorite central monitoring station without any special equipment.”

The opportunity for upgrades is only going to increase in pace, Jones-Shand says. “As of this January, telephone companies are no longer required by the government to maintain or keep POTS or PSTN lines working.”

The end of copper lines also has prompted opportunities for non-cellular alternatives, says Jim Burditt, vice president of sales, AES Corp., Peabody, Mass., which offers a mesh radio solution. “The degradation and removal of POTS lines are forcing alarm installers to seek an install alternative alarm communications equipment. The same is true with the sunsetting of cellular communications as carriers shut down 2G and 3G networks and installers are forced to replace equipment. These constant technology changes from public providers continue to frustrate alarm installing companies and have opened opportunities for AES where sunsetting has become a thing of the past.”

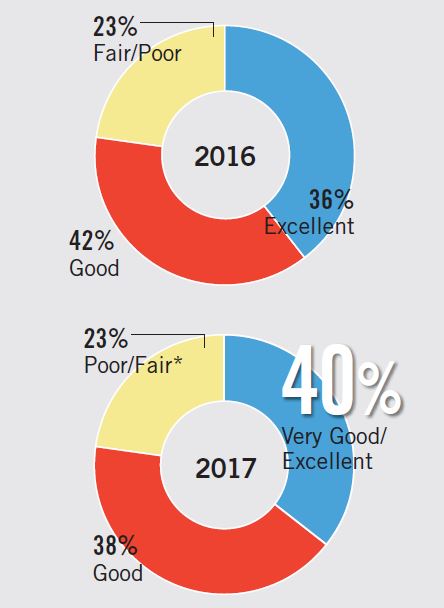

SDM asked, “How would you rate the current state of the market?”

Source: SDM’s 2018 Industry Forecast Study

The state of sales in the fire alarm market from 2016 to 2017 experienced a slight bump in the highest category.

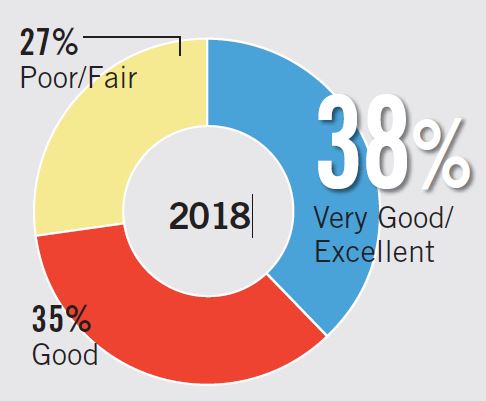

SDM asked, “How would you rate the potential for sales in 2018?”

Almost three-fourths of respondents (73 percent) have a positive outlook for 2018, even more than those answering the same question last year, of which 67 percent had an optimistic outlook for the fire alarm market.

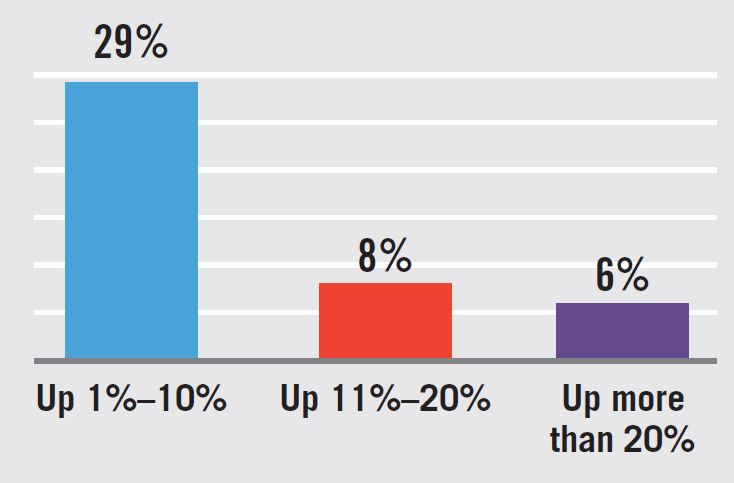

SDM asked, “How do you expect your level of fire protection spending in 2018 will compare with 2017?”

Forty-three percent of respondents expect fire spending to be up in 2018, a 10 percentage point jump over the previous year. This may reflect an increase in business, as well as possible price increases.

An aggregation of seven different research firms’ data, the AIA forecast projects commercial construction to stay strong, with a healthy average 4 percent growth through 2019.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!

")