Preparing For A Better Economy

SDM’s Industry Forecast Study indicates the economy is the No. 1 factor that will affect sales over the next three years, and that the No. 1 challenge to security businesses is increasing sales. A byproduct of the rotten economy is that it’s forcing security businesses to shift their plans and market focus, which then changes the game for other integrators.

“Companies have retooled from residential into commercial, so it’s more competitive. There are more people in a tighter space than there were before,” describes Ed Bonifas, vice president of Alarm Detection Systems Inc., Aurora, Ill., and president of the Central Station Alarm Association. “It’s not just that the economy’s bad; the business is being shared by a larger group of people. Some of our volume drop is tied to margin erosion that comes just from being in a more competitive market.”

Furthermore, dealers and integrators relied a great deal in 2009 on a healthy backlog of jobs from 2008. But now that backlog has been either greatly reduced or diminished going into 2010.

“It’s a tough market here in Chicago, from the perspective that companies aren’t spending money that they had been spending in previous years,” Bonifas describes. But he is quick to point out that not all cities or regions are experiencing such pressure. Texas is one state, he says, where he thinks the demand for security systems and corresponding spending are holding up well.

Another is the Pacific Northwest, which is served by Aronson Security Group. Mike Kobelin, vice president of sales for the Seattle-based integrator, said the company’s sales were up 10 percent in Oregon and flat in Washington, although that was primarily due to needing more people in that market, he said. Kobelin also is chairman of PSA Security Network which represents more than 200 security integrators.

“In Oregon and Washington I feel the opportunities were there. We could have gone up in Seattle but I think we need a few more people there. I think other competitors of ours in the Northwest had good years. We had some good glimmers of hope overall,” Kobelin related. He says, however, that Aronson’s national accounts business was down 30 percent due to the cancellation of construction of some large data center facilities.

“We are really very bullish on 2010. We feel that we’ve restructured our sales group to capture the market opportunities and we are expecting sales increases in all three of our groups, of minimum 10 percent,” Kobelin says.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

PRICING FLUCTUATIONS

With less demand in the residential market, one would have expected pricing discounts along with that. The SDM Industry Forecast measures pricing of traditional residential systems and mass-marketed systems. In the mass market segment, the average price of a residential system declined $50, to $348 in 2009. In the traditional market, however, the average price of a residential security system increased approximately $100 to $1,738. A large percentage of respondents expect no change in these average prices in 2010 — most think residential installation prices will neither increase nor decrease.

Most companies also did not increase rates for monitoring or other recurring fees last year, according to the survey. As many as 60 percent of survey respondents indicated they did not implement a rate increase. The average monthly monitoring fee for residential customers is $26; for non-residential customers, $37; and for remote video monitoring customers, $83.

POSITIONING FOR A COMEBACK

Nearly six in 10 survey respondents indicated they think information technology/networking expertise will have much more influence on their sales in the next three years. Confirming this statistic is John Rose, president of Marietta-Ga.-based NEIS, which helps place security talent.

“The person who installed a system at a home or business two years ago is not the same person installing it today,” Rose says. “I helped hire a project manager…I had to go outside the security business to the IT business. I found a 28-year-old DeVry University graduate with two years in the security industry. He has MCSC, Cisco certification, and other security software certifications. But he can troubleshoot a Lenel system in Dubai on his PDA.”

According to the Industry Forecast, 62 percent of companies employ between one and five people in the field of IT or MIS.

“So while they say hiring is slow — and probably in the last 90 days we’ve gotten a lot busier — the qualifications are different,” Rose admits. “Whether it’s a sales person, project manager or a technician, they have to have all the certifications and they may even have to have security clearance. They have to embrace technology because their clients have embraced technology. The technicians have to grow in the business because that’s really where the rubber is meeting the road,” Rose describes.

Although the SDM Forecast Survey doesn’t ask respondents about spending on training, for the first time in 2009 it asked companies if they had increased or decreased their employee count. The results were that about half remained at the same level, approximately one-fourth increased staff and one-fourth decreased. The data will be more meaningful in coming years when there is a history of comparable data available.

In general, security dealers and integrators place a high value on their employee base and do everything they can to retain it.

“Our own company has now gone 40 years in a row [without] anybody being laid off,” Bonifas says, adding that Alarm Detection Systems’ body count is down because of attrition and not replacing people as quickly as usual. “We had technical people from our lock shop cutting the grass, just to keep the talent that we’ve pulled together over the years. It’s a way for a company to stay poised for when the economy takes off.”

Bonifas further states that each security company needs to implement their own strategy for staying profitable. “With an 8 percent drop in business, if you do everything you used to do with all the people you used to do it with, you’ll certainly lose money.”

2009 Industry Revenue: 7.8 PERCENT DECREASE

Not Seeing Past the Darkness: THE ECONOMY RULES ALL

The three factors security dealers and systems integrators predict will most significantly affect sales by their companies over the next three years

Greatest Challenge: STIMULATING SALES

The three factors security dealers and systems integrators feel will be major challenges to their companies in the next three years

Strongest Non-Residential Markets: EDUCATION, COMMERCIAL & RETAIL

Strongest Residential Markets: EXISTING HOMES, MULTI-UNIT

Dealers and integrators indicate the one residential market segment where they expect the highest rate of growth for their companies in 2010.

Revenue Breakout by TYPE OF SERVICE

Revenue Breakout by TYPE OF PRODUCT

RMR: Average Monthly Monitoring Prices

Dealers and integrators were asked: What is the average monthly monitoring price of the systems your company currently monitors for a...?

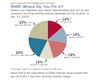

RMR: Where Do You Fit in?

Dealers and integrators were asked: Approximately what will be your company’s recurring monthly revenue, generated by this location, on Dec. 31, 2009?

RMR: Rate Increases Were Minimal

Dealers and integrators were asked: By what percentage have you increased the recurring revenue rates charged to your customers during the past year?Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!