State of the Market: Video Surveillance 2016

Certain trends in the video surveillance market are revealing profitable opportunities. For example, Integrated Security and Communications’ Michael Thomas understands that because security systems are considered business-critical, regarding IT as a partner pays dividends.

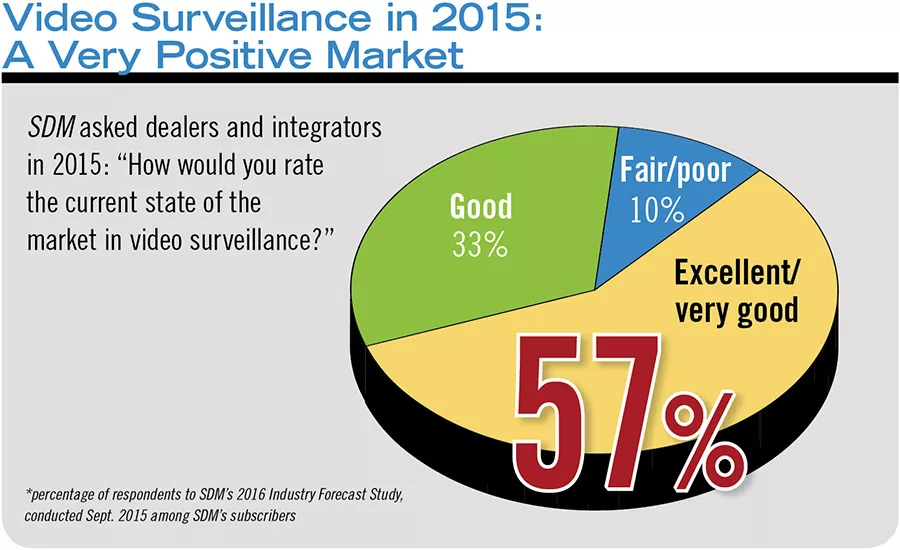

Nine of 10 respondents to SDM’s Industry Forecast Study deemed the state of the video surveillance market to be either good, very good, or excellent in 2015.

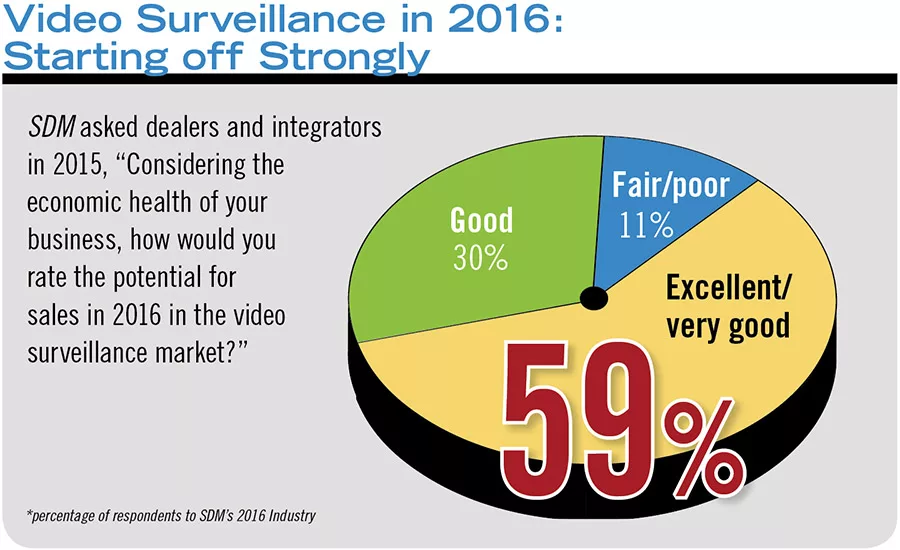

Looking ahead to 2016, 89 percent of respondents to SDM’s Industry Forecast Study expect the state of the video surveillance market to be good, very good, or excellent. This compares with 93 percent who expected the same one year ago.

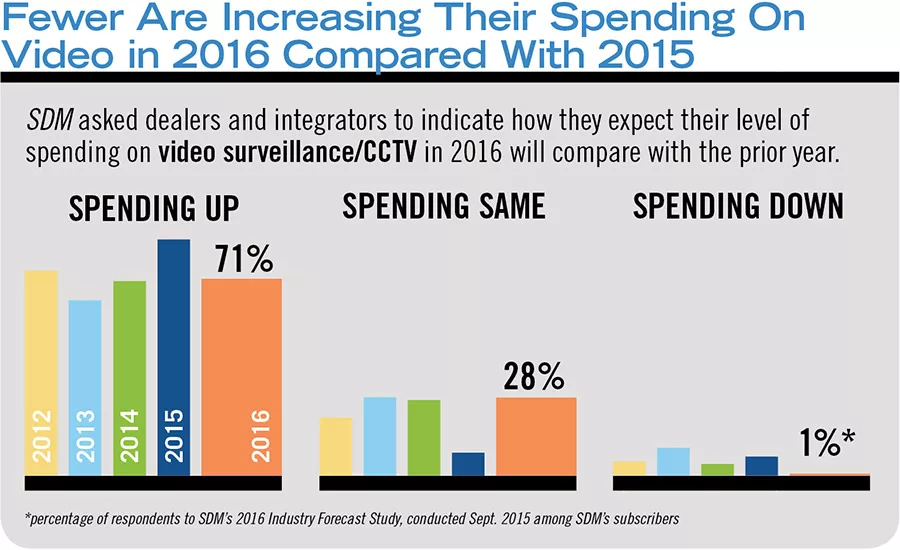

Of the 71 percent of respondents who note their spending on video surveillance equipment will increase this year, more than one-third expect that increase to be greater than 10 percent.

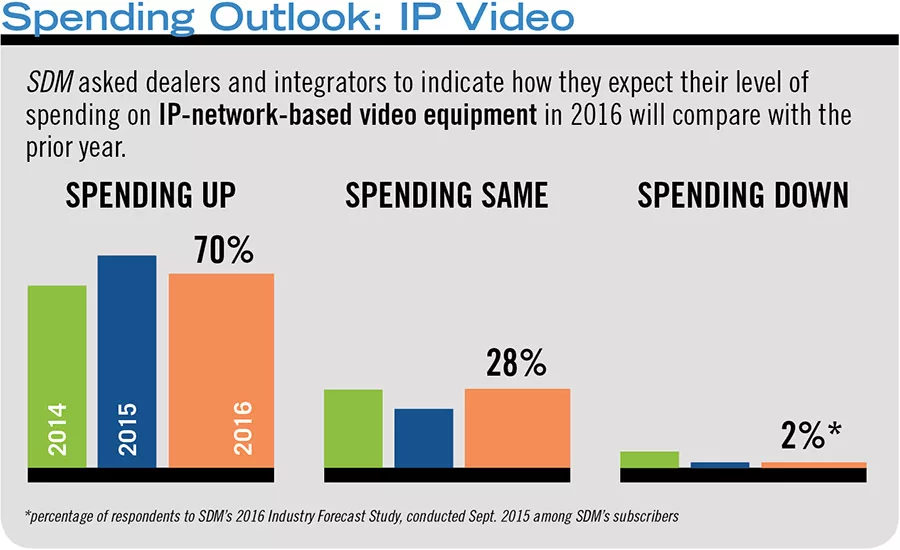

Seven in 10 respondents to SDM’s Industry Forecast Study expect their spending on IP network-based video equipment to increase this year compared with 2015. However, that is fewer than the percentage who indicated the same one year ago.

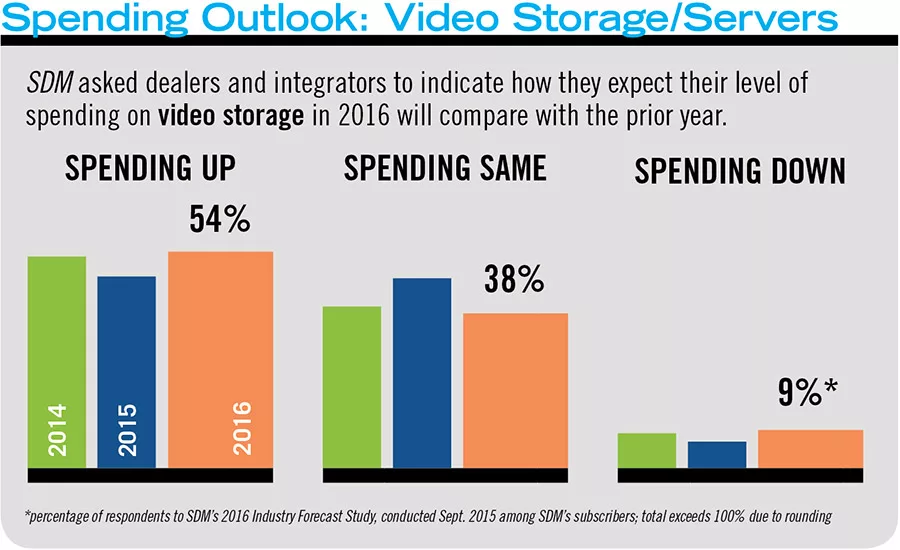

A greater percentage of respondents to SDM’s Industry Forecast Study indicated that they plan to increase their spending on video storage/servers this year, compared with one year ago.

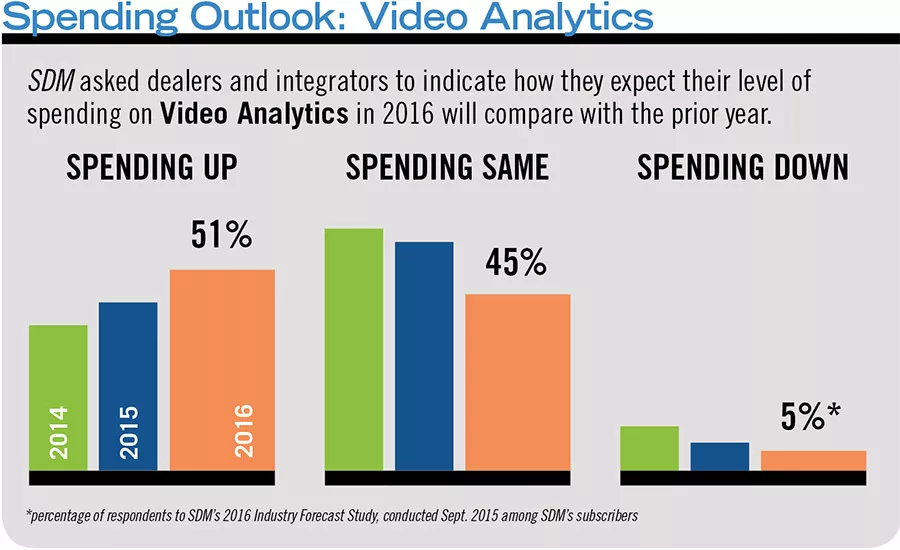

Video analytics had a significant surge in the percentage of respondents to SDM’s Industry Forecast Study, who said they planned to increase their spending on it in 2016 — from 33 percent to 51 percent.

For many years, it has become an annual refrain to declare the video surveillance market to be strong. How long that refrain continues remains to be seen, but at least for now, the state of the video market is perhaps best summed up by the words of Buzz Lightyear: “To infinity and beyond.”

There are many indications that we’ll be saying the same phrase next year as well. According to Jon Cropley, principal analyst, Video Surveillance & Security Services, IHS, 2016 is likely to see the continuation of several long-term trends in the video surveillance market. Among these trends that will drive video are the continued migration from analog to IP, aggressive price competition, further consolidation of the supply base, and the increasing importance of China to the world market.

Like much of the industry in general, 2015 was a solid year for Integrated Security and Communications, an integration firm located in Hamilton, N.J., although the company’s revenue stream took an unusual path over the course of the year.

“We had a great year overall but would say it was uncharacteristic as compared to the past years in that there were defined peaks in opportunities and activity at deferent intervals throughout the year,” says CEO Michael Thomas.

In the early stages of 2016, the company has begun to see a similar change in customer activity patterns emerge. “We have already hit some targeted goals and are responding to early customer requests for solutions. This is also a bit abnormal as compared to, say, the last five years,” Thomas says. “Although we have had double-digit growth in each year, it’s normally a slower start as companies are closing the previous year and establishing budgets for the following year.”

This deviation in the business cycle could be a harbinger for the industry as a whole that end users are placing greater emphasis on security, Thomas says. “I believe this may be a key indicator that companies are actively seeking to fund security for their facilities and that the budgets are being approved by senior management in response to what’s happening in the world around us as they seek a safer and more secure work environment for their employees,” he says.

Among those projects organizations seem to be more willing to fund are upgrades from analog to IP, many of which are long overdue. “It very much appears that end customers have finally received budget approvals for security upgrades to increase or replace video surveillance systems,” says Tom Larson, director of sales and engineering, BCDVideo, Northbrook, Ill. “There have been many projects in the retail vertical that were upgrades of analog systems that were 10 years old.”

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

A much less positive factor is also driving the video market, namely recent events that include acts of terror and workplace shootings. The unfortunate reality is that end users’ acceptance of video is growing with each incident.

“Events such as the San Bernardino shootings have refocused attention on real threats to areas where people gather, including large public spaces and campuses,” says Keith Drummond, senior director of sales, IDIS America, Coppell, Texas. “An already ongoing conversation regarding terrorism and homeland security has intensified, as has an appreciation of the role of video surveillance in both identifying and neutralizing threats, and providing detailed documentary evidence to law enforcement in the wake of incidents.”

Meanwhile, the industry is reaching a number of significant milestones as well, including moving past the tipping point where sales of IP products have surpassed analog. We are also on the brink of innovations such as the H.265 compression algorithm that will make 4K video more realistic for more end users, as well as higher-megapixel cameras and growing awareness of the need for data and cybersecurity and other factors.

Greater reliance on networks has also brought increased competition, primarily the form of IT value-added resellers (VARs), a trend that should continue, Cropley says.

“Network video surveillance equipment is relatively easy to physically install; however, it does require an in-depth understanding of how these cameras will affect the network they are connected over. This knowledge is already present in IT integrators and VARs,” he says. “We have seen these IT integrators and VARs enter the market as traditional security integrators have struggled to re-skill or upskill their workforce. IHS expects this trend will continue as network cameras begin to be seen as just another part of the IT network.”

However, there are many who haven’t taken a dim view of this increased competition.

“Competition is good. Those who are best educated will provide the most reliable solutions, which snowballs into new business,” says Mark Espenschied, director of marketing, Digital Watchdog, Tampa, Fla.

Rather than lament the challenges associated with stiffer competition, Hank Monaco, vice president of marketing, Tyco Integrated Security, Boca Raton, Fla., suggests seeing it as an opportunity. “Security has always been a hyper-competitive environment and market. Some outside competition can make us better at what we do. We have to raise our game to make sure we have the best technology and the best workforce so we can serve our customers well,” Monaco says.

While the video market remains strong, it is not without factors that to some extent are hindering growth. Among these is the technology itself, believes Tom Cook, vice president of sales and marketing, North America, Samsung Techwin America, Ridgefield Park, N.J. “If something was holding back growth, I believe that might be technology. A lot of companies are waiting for adoption of H.265 to make purchases. They don’t want to jump into 4K because of bandwidth and other concerns, so they’re sticking with the lower-priced solutions that are cheaper,” he says.

Customers in the retail, hospitality and restaurant industries served by Los Angeles-based integrator DTT Surveillance have to some extent delayed purchase decisions based on uncertainty around and the effect of laws that directly impact their bottom line. “With the Affordable Care Act, business owners didn’t know what the cost would be to provide insurance to their staff, which related to spending 12 to 18 months ago,” says CEO Sam Naficy. “Now that that’s been overcome and is understood, there are a number of minimum wage issues around the country. The average restaurant has 30 to 100 employees, so when they have to go up in minimum wage costs for employees, that causes huge jumps in cost and creates margin erosion, which causes owners to take a ‘wait and see’ approach.”

The decreasing equipment prices within the video market may not be positive for installers and integrators, but this trend has created greater demand for video surveillance in general. “The increase in megapixel and continuing reduction in price has lowered the barrier to entry, making video accessible for more customers,” Monaco says. “As a result, we’re seeing growth across all sectors of the marketplace.”

More Savvy End Users

Keeping pace with technology changes, end users have also evolved, bringing changes in their buying patterns for surveillance. Today’s end users are savvier and more comfortable with technology in general, meaning, many customers are taking a more methodical, deliberate approach to the evaluation and decision-making process.

“End users are doing a lot more detective work and investigation of what they should buy because there’s so much technology in the marketplace, and a lot of discrepancy in what people are telling them is best,” Cook says.

A major change is the fact that customers are in large part no longer looking specifically for hardware. Instead, they want solutions — in the most basic sense of the word.

“Nobody wants video any more. Customers are savvy and have the knowledge that cameras alone are useless,” Naficy says. “You have to provide cameras with actionable intelligence. Integrating disparate systems and layering video on top is critical.”

Rob Simopoulos, president of Scarborough, Maine-based integrator Advance Technology, has seen similar patterns in his company’s customer base. “We are seeing a trend where our customers and prospects are looking for solutions that are a single-software, unified security management system rather than just a video surveillance system. Many of them are seeing benefits in unified systems that include multiple technologies such as video surveillance, automatic license plate recognition, access control and visitor management in one user interface,” he says. “The feedback we are receiving is that this unified approach is more appealing compared to the traditional offering of individual systems/software, even with integration licensing add-ons.”

Awareness of the advanced capabilities of video surveillance systems has created a stronger bond with IT departments for integrated security, Thomas says. “Our clients are recognizing that systems have grown in capabilities and with that comes some complexity; that, coupled with the positive influence by IT partnered with security and the needs for compliance and stronger cyber policies, is changing the way companies want to be serviced.” (See “Balancing Physical Security With the Ever-Expanding Role of IT” on page 56.)

Price Pressure

Perhaps the greatest challenge for both integrators and manufacturers comes in the form of declining prices for video surveillance equipment. Driven largely by increased competition and a number of lower-cost manufacturers entering the security business, the average price for a network camera fell by more than 18 percent in 2015, according to research firm IHS.

“The rise of some new competition, especially in the all-in-one market, has created a lot of downward price pressure. It’s not a fun place to be. Vendors whose bread and butter is in the 10- to 50- or 75-camera range are feeling a lot of heat right now,” says Andrew Elvish, vice president of marketing and product management, Genetec Security, Montreal. “People are starting to work on razor-thin margins on the lower end, which is a benefit to those companies that can tightly control manufacturing, distribution and other costs.”

Integrated Security has seen pricing challenges, mainly in the small and mid-size markets, but has not felt too much pressure based on its business model. “We tend to augment video through integrations with complementing technology such as ground-based radar, video analytics and system integrations; it becomes not about the camera or the cost of the camera at that point,” Thomas describes.

Unfortunately, the commoditization that results from downward price pressure is not limited to any one product type or vertical market.

“There’s no doubt that we’re beginning to see a commoditization of products and subsequently a slight reduction in profitability on projects in our video surveillance marketplace,” Simopoulos says. To address this challenge, Advance Technology has developed and launched a number of value-added service offerings to complement customers’ video systems, including proactive system health monitoring. “These managed service offerings are providing a higher percentage of system uptime and providing our customers with an improved system experience,” he adds.

Lower price points also can make it difficult for organizations to equal their profits from year to year.

“The volume of business is there, but with price points coming down, you’re selling at a lower price than a year ago. That lower price means you have to sell more units just to level off,” Cook says. “Newer technology will help, such as multi-sensor cameras that carry a higher price tag. We’ll catch up.”

Price decreases are inevitable, so rather than bemoan that trend, Sean Murphy, regional marketing manager, Bosch Security Systems, Fairport, N.Y., suggests looking for the positive. “Declining price is a struggle for every market. It increases the importance of innovation to preserve value and shortens the profitable lifetime of products,” he says. “It can, in a long enough cycle, potentially cause commoditization — a negative for the market — but it also fuels the need to innovate.”

Turning to a Service Model

In the face of continually decreasing equipment prices, integrators must think creatively to offset the negative aspects.

“Cost is a double-edged sword. It opens up video to places where there was a barrier to entry, but it also creates lower transaction value of video purchases,” Monaco says. “The question becomes how to turn video into more than just on-site collection of evidence.”

One way to recoup some profitability is to offer value-added services that will generate ongoing recurring monthly revenue (RMR), which will increase the profitability of video projects beyond deployment. In short, services are the future of security.

“There’s a great opportunity for integrators to offer additional services to their video system solutions. One example is to offer central station monitoring. If designed and implemented appropriately, analytics-enabled cameras can be deployed to protect property lines or building perimeters, providing detection and verification — often before intruders even reach the building,” Simopoulos says. “Coupling this with central station operator involvement through talk-downs and verified dispatch, these systems add another layer of security to end users’ facilities and are a great way for integrators to earn significantly valued RMR for their business.”

DTT has long recognized the importance of shifting to a service-based model. “Hardware costs for cameras are irrelevant. It’s almost like a cell phone — you’re getting it for the services,” Naficy says. “We’re not in the business of hardware. We’ll install a recorder and maybe four to 12 cameras at a location and then it’s all about the services we provide after installation.”

The expanding role of IT in video surveillance today has made it easier for integrators to take advantage of selling value-added services.

“Our value as an integrator to end users is providing a holistic approach to security,” Monaco says. “It’s not just about technology, but also ongoing services. IT organizations are more involved in decisions or influencing the decision process of video security technology, and they’re more used to subscription-based services for ongoing services.”

Beyond Security

The growing number of networked devices, known as the Internet of Things, creates opportunities to pull together data from a wide variety of security and non-security devices and systems, which then can be used for both security and operational purposes.

“There has been an explosion of sensors, and customers are adding more and more. The challenge is to figure out how to manage, make sense of and correlate the data from all of these sensors,” Elvish says.

Integrating video, access control, identity management, time and attendance, and other systems can extend applications of the video system beyond security and into providing information for other corporate or operational needs. Video analytics such as heat mapping and people-counting enable more organizations to gather more business intelligence, further strengthen the effectiveness, value proposition and profitability of video.

“We’re seeing large retail customers using video analytics to analyze shopper traffic and other more operational factors. This goes a long way toward opening up other revenue streams beyond traditional security,” Monaco describes. “Integrating video with other technologies can help customers do a better job at complying with company operating processes and setting standards over multiple sites. These are benefits that integrators can ascribe to video. We have to think beyond traditional forensics and loss prevention. Video is helping people as they think about managing their business and delivering more value.”

Video analytics have come a long way in the years since their introduction, when end users became fed up with the inability of providers to deliver the promised performance. This has significantly contributed to the ability to deploy video for more and more applications, but it’s important to remember those early days, says Dan Cremins, director of product line management, March Networks, Ottawa, Ontario, Canada.

“Analytics are better now than they were in the beginning. This enables a wider variety of security and non-security applications,” he says. “With analytics, video becomes part of ‘big data’ and can be used more for information in addition to security, but it has to be applied in the right way. If it isn’t, end users will lose confidence in analytics again.

“There are very meaningful operational opportunities that I refer to as the Internet of Security Things,” he says.

The ability to pull together all of that data to provide a cogent view into the system can provide valuable insight for operations, risk, compliance, marketing and other purposes in addition to security. This also allows customers to shift video surveillance from a capital expenditure to an operating expense, making cost more palatable.

“More people have access to the same video, so by providing more to existing customers with the same solution, it’s easier to make the ROI case,” Cremins notes. “Our retail customers have no problem with the budget because security can often get these other departments to chip in because they can use the video for different purposes.”

VSaaS & the Cloud

There has been a great deal of talk within the industry for several years about the promise of the cloud for video surveillance applications. While there are vertical segments and end users that are taking advantage of the many benefits, the cloud has yet to deliver on its full potential.

“While I do see cloud storage and VSaaS systems, as well as hosted access control, as drivers for RMR for any integrator or security dealer, the market is in its infancy in many ways,” Thomas says. “I believe there is a large part of the market that is not served, and we will see more sophisticated solutions enter the market. Many solutions today are great solutions for property managers and retail, for example, but are not being easily adopted by larger companies. I believe that if you look at SaaS and PSIMs, there will be a time where these products meet those expectations.”

Espenschied believes that opportunities exist across all vertical markets. “The backup of video to the cloud is in demand and will continue to be an opportunity for manufacturers. Direct-to-cloud surveillance is good in theory, but local recording and cloud backup is still the more reliable approach. Rather than VSaaS, edge camera systems with cloud access and backup present a more realistic opportunity.”

Sam Belbina, director, strategic sales, Hikvision USA, City of Industry, Calif., adds, “Unfortunately, it has been slower than expected to be adopted because of concerns around cybersecurity and control over data. Many customers are reluctant to let go of their data. So while the cloud and VSaaS are out there, they have not been embraced as expected.”

For more on the security of networks and the cloud, see “The Cybersecurity Effect” on page 49.

The DIY Outlook

More than one-third of dealers and integrators interviewed for SDM’s 2016 Industry Forecast placed DIY at the top of the list of the greatest competition they face today. While these solutions have had the greatest impact on the residential and small business markets, research firm IHS projects this segment will not only continue to grow annually but will increasingly expand farther into the commercial sector.

“DIY is definitely growing and I’m sure it affects people’s buying patterns. They see a low-cost solution in a store and wonder what the difference is,” Cremins says.

These solutions may be fine for some end users, but they lag far behind the features and functionality of professionally installed systems.

“We saw a lot more DIY in the second half of 2015 with technologies like Netcam, the Rain doorbell and Canary,” says Christie Hamberis, senior vice president, ScanSource Networking and Security, Greenville, S.C. “The home market is prime for those solutions, but features and functions over the long term will play big in end users’ buying decisions.”

For Samsung Techwin America, DIY has been a successful endeavor.

“For us, DIY is gigantic; it’s part of our company. We sell tremendous amounts of DIY solutions through Costco, Home Depot, Lowe’s, Sam’s Club and others,” says Samsung’s Tom Cook. “Our $69, $89 and $149 cameras are selling like hotcakes. We will be bringing that into the commercial realm, so it will be coming over into our market. But it’s not for everyone.”

End users are being enticed more and more to purchase and set up video surveillance systems without using a professional installer, says Mark Espenschied of Digital Watchdog. “However, we feel that this trend has always cycled back to the demand for the professional installer in commercial and large consumer applications.”

The good news about DIY is that it is possible for dealers and integrators to participate in and generate RMR from that segment of the market. Several of the largest security dealers already have DIY offerings.

2016 Year in Congress — A Short Timeframe to Consider Trillions of Dollars for the Government

Balancing Physical Security with the Ever-Expanding Role of IT

The Cybersecurity Effect

One of the main reasons adoption of cloud-based video services have not grown as much as anticipated is end users’ concerns about data security. Confidence in the ability to secure networks and data seems to wane with every high-profile data breach.

“Data security is a real concern for the American people in general,” Hikvision’s Sam Belbina says. “This issue will never die; it’s going to be with us forever. The dilemma is to figure out how to address it.”

In addition to potentially holding back adoption of cloud-based video, cybersecurity concerns have also led to end users re-prioritizing their security goals.

“Everywhere you go, you hear about cybersecurity. It’s a real concern,” says Christie Hamberis of ScanSource. “As a result, we’re going to see a shift in security budgets from physical to the network side.”

Previously, many video surveillance manufacturers viewed network cameras as edge devices. As such, they expected that they would benefit from the network security IT departments provide, says Jeff Whitney, vice president of marketing, Arecont Vision, Glendale, Calif. In light of recent network breaches, that mindset has shifted.

“Growing awareness, however, has led to concerns that while a network camera typically doesn’t have the computing horsepower to become a point of attack on the network should it be improperly accessed, video from it could potentially be hijacked or the camera disrupted,” he says.

The result is that several leading network camera providers, including Arecont Vision, now build more cybersecurity features into their products. Basic features such as 16-character ASCII passwords and issuing user recommendations for initially setting and later updating passwords regularly are becoming best practices for many manufacturers, Whitney relates.

With high-profile breaches coming through HVAC firmware and other seemingly unlikely entry points, the “security of security” has become critical. However, says Andrew Elvish of Genetec, the physical security industry hasn’t given much thought to managing data from IP-based cameras and other devices securely as it moves through corporate networks. “It’s impossible to understate how important cybersecurity is for physical security. While the industry has been pushing strongly for IP-based solutions, I don’t think the security of security has gotten enough mindshare.”

Education has been central to Scarborough, Maine-based integrator Advance Technology’s push toward ensuring IP-based cameras are secure from potential breaches. “We’ve been learning from the leadership of Bill Bozeman at PSA with regard to the changes integrators need to make to their business to improve their cybersecurity posture,” says Advance Technology’s Rob Simopoulos.

In addition to pursuing training for its employees and sending them to cybersecurity conferences, Advance Technology also has partnered with cybersecurity experts to assist the firm in making improvements to its business practices. “Our goal is to continue to become more knowledgeable in regards to what we can do to protect our customers and deploy video surveillance systems with improved cyber hygiene,” Simopoulos describes.

“It’s very important to be able to prove why a camera can’t be hacked and show what you’re doing to ensure that it’s not going to be hacked,” says Samsung Techwin America’s Tom Cook. “Some companies are vigilant and some aren’t, so the desire to move to the cloud might be prevented by customers’ reasonable doubt about cybersecurity.”

Having built its entire business on providing cloud-based and other services to support the video equipment it installs, integrator DTT recognizes the importance of network security. Because the company’s focus is on the retail, hospitality and restaurant verticals, that means ensuring that video devices comply with the Payment Card Industry Security Standard (PCI), which calls for some of most stringent network security requirements.

“We’re very adamant about PCI compliance and cybersecurity because we’re also accessing credit card information with POS system integration. Most customers wouldn’t even look at us if we weren’t,” DTT’s Sam Naficy says.

“Security is a real pain point as we move to the cloud, so we’re very conscious of ensuring encryption from the edge to servers to the cloud — all the way upstream and downstream,” says Hank Monaco of Tyco Integrated Security.

The United States begins the second session of the 114th Congress in mid-January (at the time of this writing). Congress will be working under a very constricted timeframe due in large part to the national election schedule. The majority of the $1.5 trillion federal budget was approved prior to Christmas, but in the first six months of 2016, Congress will review President Obama’s last federal budget request for all agencies.

This year will bring many interruptions. The Congress will recess for the July political conventions as well as their August summer break, and focus squarely on campaigning in September and October. More than 85 House and Senate members have already announced their retirement; and usually in an election cycle there are changes in seats, so this will be a critical November for control of the House and Senate.

Congress will reconvene after the November elections for a “lame duck” session from Thanksgiving to the end of the year where funding bills and end-of-session bills need to be passed and considered.

One of the areas of opportunity that ESA will be reviewing in the video surveillance marketplace for the next year is the funding process of grants that are provided from federal departments and agencies to states by a formula basis. In many of these programs, allocation of monies have been used by local governments to purchase, install and maintain video surveillance equipment to protect business districts, public housing and other locations within a community. A wide variety of funds is therefore available for competitive procurement by cities, counties and other localities based on funds appropriated not just from Congress, but also from the state governments.

ESA’s “Congressional review of the fiscal year 2016 budget approvals from December 2015” will be presented at the ESA Leadership Summit and to ESA members. There will be another round of monies to be appropriated in the 2016 calendar year by Congress, which will include hundreds of millions of dollars to states from the Department of Homeland Security and many other well-funded programs that provide funding from the federal government to a state and then onto local areas.

In addition, ESA is working closely with other industry companies and supportive groups to make funds available from the federal government specifically to K-12 school security projects at the state level. ESA has supported the creation of a School Security Caucus of House members, started by Rep. Brooks, R-Ind., and Rep. Larsen, D-Wash., to call attention to the need for security technology in schools to prevent terrorist or criminal activities and save lives and property. These efforts will focus on the Departments of Justice and Homeland Security. — Contributed by John Chwat, director of government relations, Electronic Security Association

Many of our clients are seeing a shift in budgets moving from security to IT for implementation of the infrastructure. We see the IT departments of many organizations adopting a model whereby their security directors and/or departments are internal customers or stakeholders that they serve, but IT defines the standards and requirements. So while security or procurement would have been the decision makers in the past, IT departments are heavily involved in evaluating the designs and security of devices installed on the network.

We see this as a good thing for companies like ours that are structured with resources to support this shift. Companies with a high “IT IQ” will see opportunities to serve their customers in more ways, while companies that have not made this investment in their people or changed their hiring practices to value these areas will see erosion in business opportunities with larger corporations or clients with more sophisticated requirements. Security systems such as access control and video surveillance are considered business-critical now for many clients, and we see IT as a partner.

However, from our clients’ perspective there need to be checks and balances regarding access to sensitive information required for business compliance and investigations. In some or most of our clients, IT supports the infrastructure but security audits access so IT doesn’t deem itself as the highest level holding all the information. It a good balance that’s has served our client base well. — Contributed by Michael Thomas, Integrated Security and Communication

Standards are essential in the networking world due to the wide variety of available hardware and software; they exist to ensure network design compatibility. Video developers and end users often need a common interface that allows them to easily connect products from a diverse set of manufacturers, both for immediate use and for future upgrades. This prevents end users from being locked into using solutions from a single manufacturer and being tied to that manufacturer for the lifecycle of the system.

ONVIF is an open industry consortium that is committed to standardizing communication between IP-based physical security products to ensure their interoperability and to facilitate their integration. Membership includes manufacturers, software developers, consultants, systems integrators, end users and other interest groups. ONVIF’s profile approach establishes fixed sets of functionalities for devices and clients that are mandatory to be considered conformant with an ONVIF profile.

ONVIF’s video profiles, Profile S and Profile G, address mature features and group them together in profiles, allowing many VMS manufacturers to outsource interoperability using the ONVIF specification. For example, imagine that a VMS manufacturer maintains support for 150-plus different camera manufacturers and that each manufacturer has 20-plus different cameras. This adds up to 3,000 individual drivers that have to be maintained and tested. In addition to this, there are firmware updates that require driver maintenance.

When manufacturers use ONVIF’s video standard, they can essentially outsource driver maintenance to the ONVIF profile specification and instead of addressing 3,000 individual drivers, they can address just one — ONVIF’s profile. With developers spending less time on interoperability driver maintenance, video manufacturers can concentrate their resources on the development of new innovative features and functions.

The use of ONVIF conformant products can also dramatically reduce the time spent on the design and installation process, since the devices and clients communicate using standard ONVIF interfaces instead of relying on unique software integrations between particular devices, such as cameras or door controllers, and clients such as video or access control management software.

Ultimately, though, the ONVIF standard is designed to make life easier for the people who use the products. By facilitating the interoperability of video devices and clients and other physical security systems, ONVIF makes it easier for systems and devices from different manufacturers to work together, which results in greater freedom of choice for end users. As the demand for interoperability grows, more companies want to work with ONVIF because the ONVIF specifications have struck a chord with end users, who are starting to demand interoperability when specifying a new security system. —Contributed by Per Björkdahl, ONVIF Steering Committee chair

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!