Financial Services: What’s Changed, What Hasn’t?

The dealer financing market has been stable for many years. The changes that have occurred include new types of investors and new factors that potential lenders will consider in making loans to dealers.

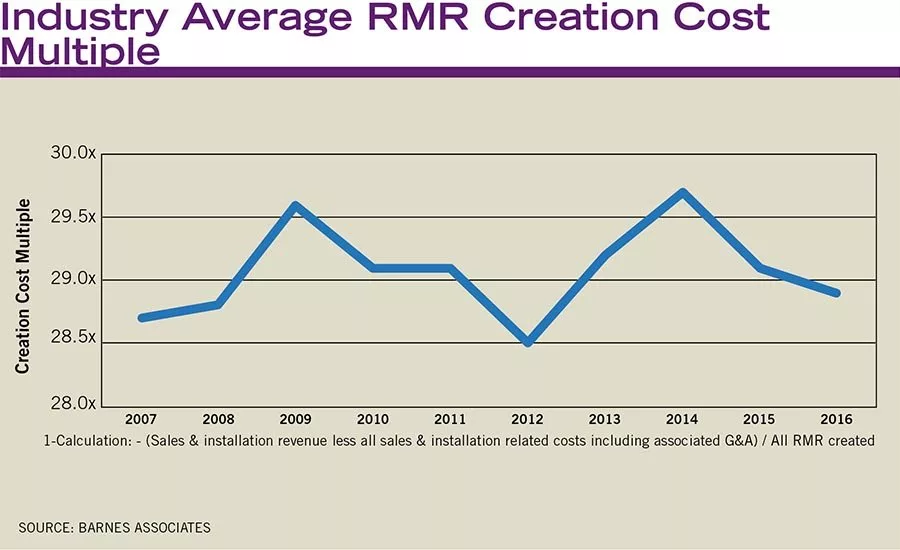

A dealer’s need for capital is driven by the RMR creation cost multiple, or the fully burdened cost to create a dollar of RMR. The industry average RMR creation cost multiple has fluctuated over time.

Raising outside funding can give security dealers the boost they need to bring on new accounts, thereby generating escalating recurring monthly revenue. But because security industry economics are so different from many other industries, security dealers face a unique set of challenges as well as opportunities when they set out to raise funding. Some of these challenges and opportunities are the same ones that dealers have faced for many years; others are new.

What’s changed and what hasn’t?

One thing that hasn’t changed much is what drives security dealers to seek outside funding.

William Schmidt, managing director of the security lending group at St. Louis-based CapitalSource, a division of Pacific Western Bank, sees three reasons: when the company is growing faster than internal profitability can support; when the company is acquiring accounts; and when one partner is buying out another.

Another thing that hasn’t changed: Traditional banks are not typically a viable funding source for security dealers because they usually will not accept monitoring contracts as collateral.

Fortunately, there are lenders that specialize in the security industry, who understand the industry’s unique economics and who will allow dealers to use customer contracts as collateral. There is one major hitch, though — one that hasn’t changed much in many years: These specialty lenders generally won’t lend money to smaller companies.

According to Schmidt, specialty lenders generally won’t look at companies with less than $150,000 a month in recurring revenue. That minimum threshold also hasn’t changed much over the years.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

There are at least two lenders that will loan money to smaller companies, however: Kattskill Bay, N.Y.-based Acquisition and Funding Services and Corte Madera, Calif.-based Alarm Financial Services. Both of those lenders will consider dealers with as little as $10,000 in recurring monthly revenue (RMR).

What about dealers whose RMR is too low even to meet that threshold? “Work hard,” advises Acquisition and Funding Services owner Rory Russell.

Some dealers may consider selling some of their assets to raise funding to generate more accounts until they can qualify for a loan. Alarm Financial Services sometimes does one-shot deals to buy accounts from dealers looking to raise money for a specific purpose, such as buying out a partner, notes Alarm Financial Services President Jim Wooster. Alternatively, for smaller dealers seeking funding on an ongoing basis, participation in a dealer program may be a better choice. A range of companies offer dealer programs that formalize the process of selling accounts on a regular basis. (See “Dealer Program Financing Options” below.)

For those companies that are large enough to be considered for a loan, lenders look at two key metrics, Wooster notes. These include the size of the loan in relation to the value of the collateral, or RMR, and the borrower’s ability to repay, he explains.

The amount a dealer can borrow is tied to RMR and is calculated using what are commonly known as “multiples.” Multiplying the dealer’s RMR by the multiple yields the maximum amount the borrower is willing to lend. As Henry Edmonds, president of St. Louis-based The Edmonds Group, LLC, explains, multiples typically are in the mid to high 20s.

In gauging a borrower’s ability to repay a loan, Wooster does cash flow analysis, looking in detail at “how much money is coming in and going out,” he explains. “We make sure there is enough left over to make the loan payment.”

When dealers qualify for a loan, funding usually comes as a line of credit, which the dealers can draw upon as needed. Typically, dealers only pay interest, not principal. Instead, paperwork may call for dealers to pay off the entire amount owed when the loan ends — although as Schmidt explains, dealers often simply negotiate a new loan at that time. “Very few loans are paid back except when dealers sell the company,” he says.

Wooster notes, however, that Alarm Financial Services’ lines of credit eventually convert to five-year term loans, which require the borrower to pay off a portion of principal as well as paying interest every month.

A FEW THINGS THAT HAVE CHANGED

Experts interviewed for this article don’t expect major changes in security industry financing — and to Wooster, that’s a good thing. “Those who were lending five to 10 years ago are still lending,” he observes. “A lot of industries can’t claim the same stability.”

The stability of the security industry in and of itself has driven one relatively recent change, however. As Edmonds explains, “The alarm industry fared very well during and after the financial crisis of 2008 to 2009.” And that, he notes, generated increased interest in the security market on the part of private equity firms — investors that seek to own a controlling interest in larger security dealers. Interest in these larger companies has been so strong that private equity firms now own just over half of the 20 largest alarm companies, according to Edmonds Group.

“Our experience is that a company must be at least $500,000 in RMR to be a candidate as a platform investment,” Edmonds observes. He notes, though, that once a private equity firm has invested in one major platform company, management may then buy smaller dealers and roll the operations of the smaller dealers into the main company — a strategy Edmonds calls a “fold-in acquisition.”

Another new type of investor in the security industry is the “search funder,” notes Michael Barnes, a partner with St. Louis-based Barnes Associates. As Barnes explains, these people are “promising, typically younger proven operating executives that are looking to acquire a company and backed by a specific group of investors.” The executives typically are lured away from corporate jobs and receive some form of compensation from the investors while they search for a company to acquire and operate, Barnes notes.

Like private equity investors, search funders generally seek to acquire an entire company or at least a controlling position, but may be willing to consider smaller opportunities than private equity firms would consider, Barnes comments.

A search funder can be a great option for some dealers, notes Barnes Associates partner Mark Gronowski. “In situations where the founder, for instance, is looking to transition away from day-to-day operations, but wants the company and the brand to survive, develop and grow, this can be a great transition arrangement,” he says. “The investors bring capital for growth and liquidity to the founder, while the young executive can have an orderly transition into the CEO chair.”

CHANGES AFOOT

One change that hasn’t happened yet in dealer financing but which sources expect to see soon is an increase in interest rates. The federal government has indicated that it expects interest rates to go up, which will impact the LIBOR (London Interbank Offered Rate), the average amount of interest that London banks would charge to lend to one another — and the rate to which dealer financing typically is tied, explains John Robuck, managing director of McLean, Va.-based Capital One.

In response, sophisticated borrowers are looking for agreements that include a cap on how high their interest rate can climb or that lock in a certain rate for a specific number of months, Robuck notes.

Alarm company owners looking to sell their business may feel the impact of higher interest rates, says Kelly Bond, senior vice president of business development for Philadelphia-based Alarm Capital Alliance. Because buyers will have to pay higher interest rates, they may base the purchase price on lower RMR multiples than the industry has seen of late, she explains. The same holds true for dealer programs, Bond observes. Higher cost of capital for the program operator may drive lower multiples there, too.

Other changes in financing for security dealers:

-

Merger and acquisition (M&A) activity on the rise. During periods of uncertainty, such as the period leading up to a presidential election, buyers and sellers become more risk averse — a phenomenon that caused a drop in the number of M&A deals last year, Schmidt observes. Now that the election is in the rear view mirror, however, “the pipeline is back up,” he says.

-

Personal emergency response system (PERS) monitoring contracts become more accepted as collateral. Traditionally lenders have been wary about lending against PERS accounts because they do not have the longevity of traditional security monitoring accounts. But that’s beginning to change, Edmonds comments. Lenders, he says, are “getting comfortable with PERS.”

-

Commercial accounts viewed more favorably. Another type of account that lenders are viewing more positively is commercial accounts, Robuck notes. “If you have a growth-oriented sector, it’s more attractive for us,” he comments. “[Traditionally], market penetration on the commercial side was very high and it wasn’t viewed as a growth segment. [But today] people are re-invigorated about the growth opportunities on the commercial side of the business.” Those growth opportunities include video and access control managed services, as well as services that use data gathered from security systems for non-security operational purposes, he explains.

Perhaps the best word to describe the state of dealer financing today is “stable.” Relatively few things have changed and, with the exception of impending higher interest rates, those changes that have occurred have been positive. As Barnes Associates partner Michael Barnes puts it, “the overall environment for this industry is as good as we have ever seen it, supported by good industry fundamentals and an improving economy.”

Dealer Program Financing Options

For dealers too small to get a loan, for baby boomers easing into retirement and for others, dealer programs can be an excellent source of funding. Dealer programs offer a formalized means for the program operator to purchase monitoring contracts from security installing companies on a regular basis. The program operator pays the dealer a multiple of the RMR and in exchange, gets the RMR.

“People come to us to sell all or a portion of their accounts to create capital for growth, paying off debt, etc.,” explains Kelly Bond of Alarm Capital Alliance. In a dealer program, some dealers may sell a percentage of their new accounts each month, while others may only sell once in a while when they need funding for a specific purpose.

Bond cautions, though, that “if you need a significant amount of immediate cash, dealer programs are not set up for that.” Instead, dealer programs are well suited for dealers seeking ongoing flexibility of cash, she explains.

Details of dealer programs vary. Some program operators provide monitoring, while others leave that to the dealer in exchange for payment to provide continued service on accounts sold. Some dealer programs, including those from Alarm Capital Alliance and Acquisition and Funding Services, let dealers continue to have their name associated with the account and a continued relationship with the customers they sell.

Demographic trends are giving dealer programs a boost, notes Rory Russell, of Acquisition and Funding Services. As the large baby boom generation reaches retirement age, Russell is seeing boomer dealers selling a portion of total accounts as a means of easing into retirement. By keeping a smaller base, the owners can work when they want to but still “keep their toe in the water [and] slowly exit the business,” he explains.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!