State of the Market: Connected Home 2017

With approximately 20 percent penetration into homes, professionally monitored security systems that are now interactive and connected have a lot of room to grow — but many others also seek this opportunity. Market players from all sides agree there is room for everyone in the rapidly expanding connected home space, but will that change?

LEFT: MONI’s Peter Tonti (right) and Jeff Gardner (left) say the company’s rebrand to the new name (from Monitronics) was part of a brand evolution that reflects the need to shift and adapt to new technologies — a challenge all companies in the connected home space are increasingly facing.

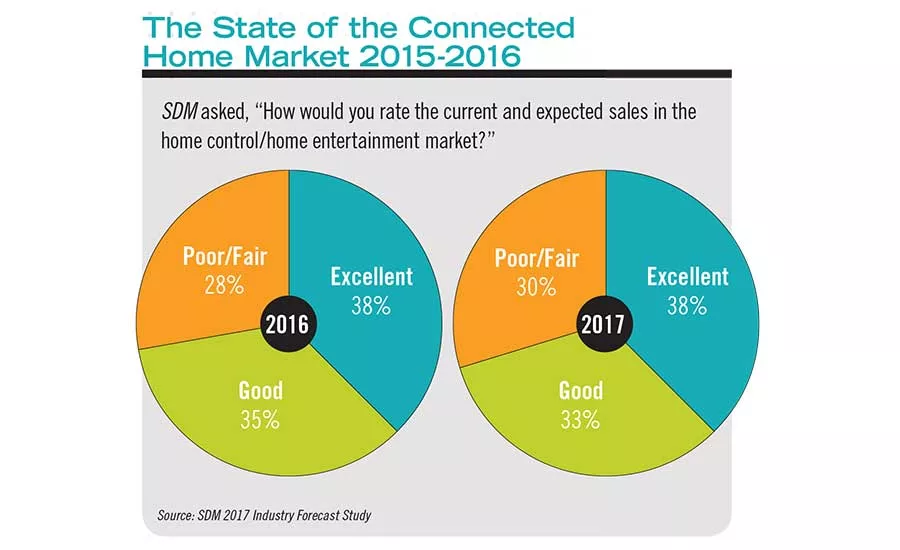

The number of respondents reporting the connected market as “good” or “excellent” rose from 65 percent last year to 73 percent in 2016. A similar percent believe 2017 will be as good or better.

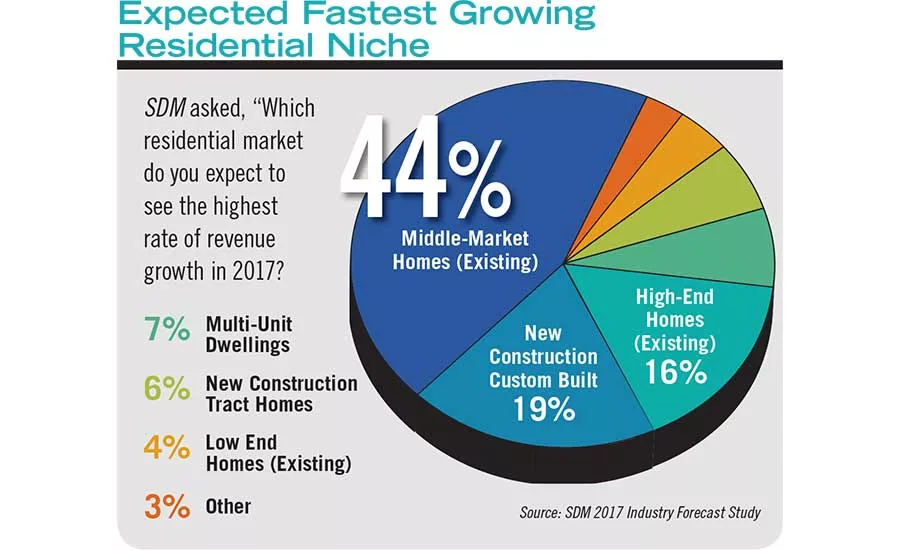

Existing middle-market homes rose 6 percentage points over the same question last year in terms of respondents' expected revenue growth. This tracks with the predicted move of connected technologies to the mid-tier.

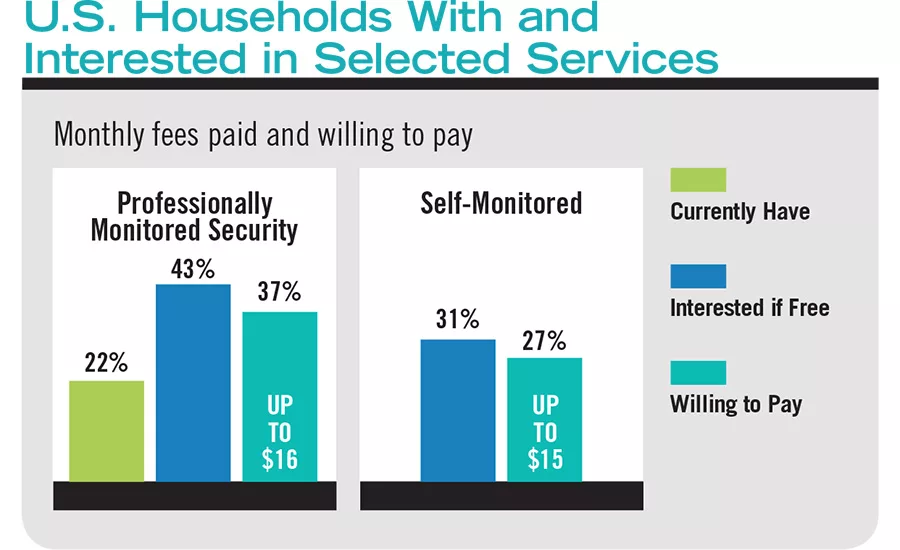

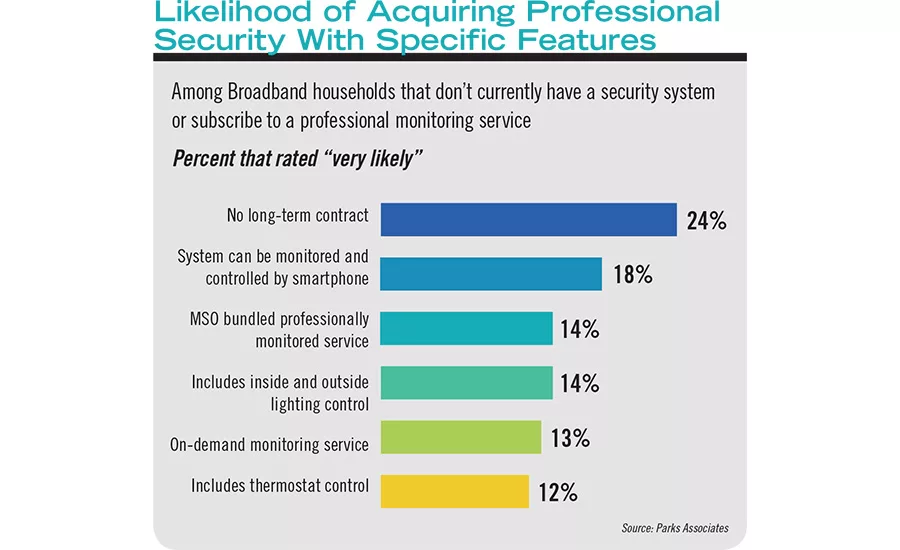

More consumers would be likely to subscribe to professionally monitored security if the fees were lower.

MONI recently placed a kiosk at Dallas Love Field airport to help get the word out about the possibilities and benefits of smart and connected homes.

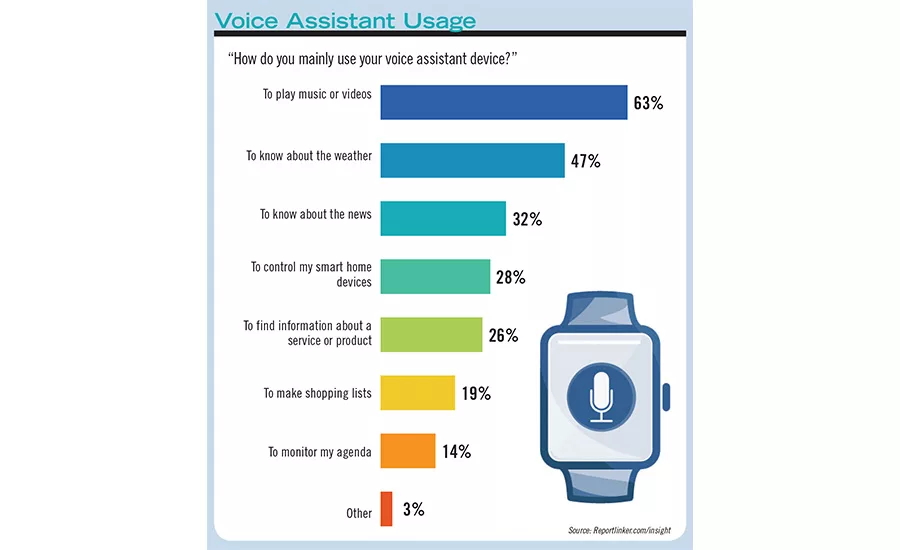

In a study conducted in May 2017, more than a fourth of users reported using a voice assistant (such as Google Assistant or Amazon Echo) to control their smart home devices.

According to Tom Kerber of Parks Associates, this consumer research that was asked of households that did not subscribe to a professionally monitored security service quantifies the relative interest in some of the new approaches to security services.

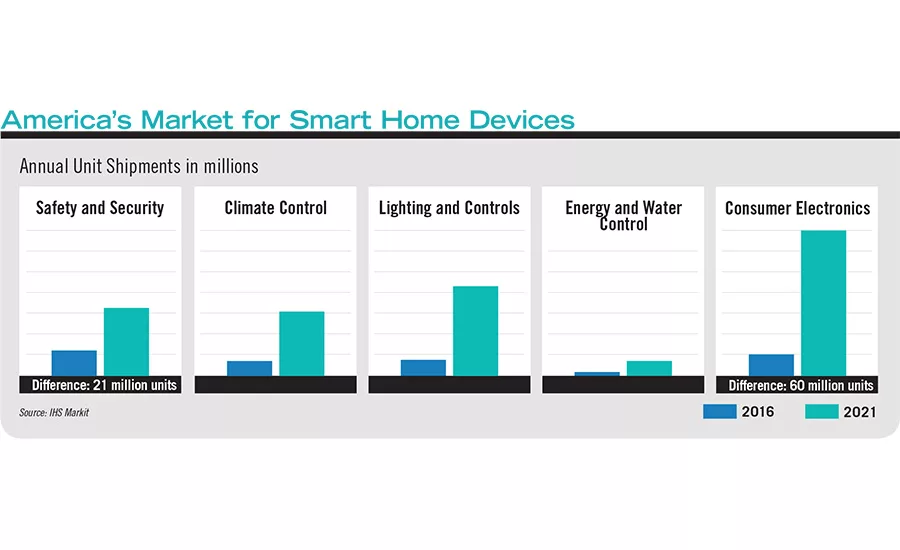

Shipments of safety and security related smart home devices will nearly triple between 2016 and 2021.

Many describe 2016 as a “pivot point” in the connected home space. While not yet out of the tall weeds, there are signs of organization and cooperation all around. More critically, there is strong desire on the part of consumers for more and more of this technology; and large players such as MONI, ADT, Vivint, Comcast and many of the DIY companies have done a good job getting the word out to potential customers about the potential of this new technology. Even better, there is evidence to suggest that customers are turning to experts for help making the whole system work — point solutions are no longer enough and they want monitoring at some level or at least help with installation and setup.

That’s the good news. But questions remain regarding whether the traditional security industry will be able to keep its edge and current pricing models in place, or whether new and varying ways of going to market, servicing the customer and types of monitoring contracts will be necessary to keep new connected home customers happy in the long run.

According to IHS Markit, Englewood, Colo., the total connected home market grew by about 29 percent in 2016 over 2015. “In 2017, the Americas connected home market is expected to expand by 33 percent in terms of unit shipments, and revenues for these shipments will reach about $6.2 billion, up from $4.9 billion in 2016,” says analyst Blake Kozak. “This growth will be driven by consumer electronics such as smart speakers and lighting.”

Another report by Markets and Markets found that 41 percent of people have already adopted at least one smart home device, with their favorites being connected appliances (20 percent), thermostats (16 percent), security (12 percent) and lighting control (10 percent).

And a recent study by August Home and XFINITY Home found that 30 million U.S. households are projected to add smart home technology in the next 12 months.

However, these numbers, while exciting, don’t necessarily reflect the portion of the business that professionally installed and monitored security is getting so far. In terms of smart home penetration, IHS predicts a 7 percent penetration by 2025. “In 2023, professionally monitored smart homes will exceed non-connected, traditionally monitored systems,” the report further stated.

It’s important to note that the penetration and growth numbers, especially those originating from different research organizations, don’t always align, depending on what is being measured, the geographical area covered, and the type of survey respondents. For example, the latest research of consumers by SDM showed that the penetration of (non-connected) professionally monitored home security systems was 21 percent.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

“When we talk about connected home we talk about products,” says Tom Kerber, director of IoT strategy for Parks Associates, Dallas. “Every one of those had double-digit growth and that is a strong indication of adoption.” But he adds the category leading the pack is smart thermostats, where approximately 11 percent of homeowners own one, but the majority (60 percent) are stand alone. The bigger takeaway, Kerber says, is that 2016 saw this category moving from high-end homes to mid-tier. “The premium tier is about 10 percent of the volume and mid-tier is 30 to 40 percent. The value tier is the remaining market. Moving to the mid-tier means adoption will move more rapidly because the price points are more affordable to the average person.”

Looking at the professionally monitored security channel specifically, Parks predicts “modest growth” at 2 to 3 percent over the next five years to reach approximately 22 percent of households in 2021. But, if you look at that same period for interactive services, “That portion is growing at 12 percent growth. That is where the action is. This is the number of households that are converting, upgrading or being added to the pool of security households. That is a huge driver for incremental RMR, as well as a method to expand the base of customers. That will be very strong over the next five years and is a trend to watch.”

This correlates to a generally optimistic outlook from SDM’s own research. In the 2017 SDM Industry Forecast Study, conducted last November, 73 percent of respondents characterized current sales in home control/home entertainment as good to excellent, and a similar number (71 percent) expected it to remain so in 2017.

It also reflects the numbers manufacturers and dealers reported seeing last year. Those that offer a strong connected platform or product that connects to one, did the best.

“Our total 2016 revenues were $757.9 million, a year-over-year increase of more than 15 percent,” reported a spokesperson for Vivint Smart Home, Provo, Utah. Its subscriber base increased more than 17 percent and nearly 90 percent of customers opted for advanced smart home services in 2016, in addition to traditional security, the company reported.

“We see significant growth in the market,” says Robert Beliles, senior vice president of marketing and product management, Nortek Security & Control, Carlsbad, Calif. “We are a beneficiary of that growth, but we also feel there are some pretty big inflection points starting. One prominent trend that will increase adoption is the ability to use voice commands.” (See sidebar, “The Role of Voice & Video,” page 63.)

Roger Barlow, senior director, product management for security products, building technologies and solutions, Johnson Controls, Toronto, has a similar assessment. “I think 2016 was on the cusp of migrating towards some real trends in term of connectivity in the home and the ability to control devices in your home from anywhere, anytime, effortlessly. We are starting to see a lot of the larger players look at that and bring together some consolidation.”

MONI reports that close to 90 percent of its customers have at least interactive security services. “It keeps growing every month,” says Peter Tonti, vice president of product marketing for the Farmers Branch, Texas-based company. “When we look at home automation or connected it is about 23 to 34 percent of new customers and that is growing. At the end of 2015 it was closer to 18 or 19 percent…. I think that is a pretty quick rate of growth and it will continue to grow at that same rate.”

Jeff Gardner, president and CEO, MONI Smart Security (featured on this month’s cover) in part credits the recent rebranding from Monitronics to MONI. “Our shift to MONI has already made a difference to both our dealers and company in the connected home space. Following our recent rebranding, MONI emerged as a leader in home automation, with more customers seeking out our solutions through both our dealer and direct channels…. We’ve seen a growing demand for the integration of smart home automation and moved quickly to incorporate it into our packages.”

Not only is the market picking up speed, it is specifically growing in terms of ecosystems or hubs, adds Jorge Hevia, senior vice president of marketing and sales, NAPCO Security Technologies, Amityville, N.Y. “A few years ago there was a lot of talk about the connected home, but it was limited in the security industry to controlling your alarm system remotely and maybe a little remote video business. Now it seems as if everyone is waking up to the connected home and they want it all in one app to control their different subsystems in their homes.” Hevia says his business grew about 20 to 25 percent in 2016 and will grow at least that much in 2017, in large part due to their Starlink product, a cellular radio communicator that allows dealers to easily add connected home services to almost any panel.

The connected home market is made up of a variety of players from both inside and outside the traditional security sphere. One of the relatively newer entrants is Comcast XFINITY Home, which recently reported more than 1 million subscriptions to its security offering. “We have doubled our subscriptions in two years,” says Daniel Herscovici, senior vice president and general manager, XFINITY Home from Comcast, Philadelphia. “More than half of our subscribers are new to the category, meaning they haven’t had home security before.”

This raises the question, how big can the connected home space grow? Could it be the “iPhone of the security industry” — disrupting the industry to the point where almost everyone is truly a potential customer?

MONI dealer Todd Johnson, CEO, Capital Connect, Tuscon, Ariz., says his company does about 90 percent residential sales, of which 80 percent is automation. “We have been transitioning over the last couple years. Between 2015 and 2016, that was the year that it really took off for the first time.

“I have no doubt that a good percentage of this growth is customers that would not have bought just a security system. In many cases, the security system is almost an afterthought to the automation features.”

Essence, a DIY security platform, had its “best year we have ever had in 25 years of business,” says Josh Locke, director of sales for the Plymouth, Mich., company. “Everything was up. We integrated with IFTTT, went to Z-Wave+ and increased functionality from our app to allow for professional installations. That led to increased sales.”

For many, the key to this type of growth has been about expanding offerings to previously under-served customers, making it easier to connect, or increasing functionality of a point solution.

“Our connected home products are up 50 percent year over year,” says Dave Mayne, vice president of marketing, Resolution Products Inc., Hudson, Wis. “Some of this is we are a new product, but more is really driven by the fact that we have products that are compatible with a lot of devices consumers are interested in, and we have built a product that extends into new markets, such as renters.”

IS IT GETTING HOT IN HERE?

Just how big is the connected home space and who is really succeeding in it right now? Most point to four main types of participants: 1. The professionally monitored security companies and dealers that have emerged as leaders with an integrated solution with a hub and multiple partnerships; 2. Cable operators and MSOs that have found success bundling interactive security and smart home devices with their cable and Internet offerings; 3. DIY solutions that either stand alone with an app or increasingly work with many of the other solutions; and 4. The giants of the consumer space (Google, Apple, Amazon) that are dabbling in the connected home space with products, but more often working together with the platform providers. Another part of the market worth mentioning is the protocols such as IFTTT, Z-Wave, Zigbee, Wi-Fi, Bluetooth and NFC, to name a few of the most popular.

How many is too many? So far, it seems that limit hasn’t been reached.

“The cool thing about the smart home opportunity is it is so large that there is no reason to be fighting over market share at this time,” says Mitchell Klein, executive director of the Z-Wave Alliance, Freemont, Calif. “There is room for everyone because the market size has yet to even be established,” he says.

“The market is growing; the question is who is growing at a faster rate than the market?” Kerber says. “Cable operators definitely, and some of the larger national players like Vivint and ADT, for example. I would say everyone is enjoying the growth, either from increased subscribers or increased RMR. There are a lot of reasons to celebrate as long as you are riding that wave.”

Perhaps because of this sense of enough to go around, there is a lot of cooperation going on in the market right now. Apple, Google and Amazon have multiple partnerships with various platform providers to work with their various devices so that customers can easily use their new Amazon Echo to program their security system, for example.

“The sum of the whole is worth more than the individual components, Barlow says. “Now you can have a home experience like you started to have [with cellphones] when the iPhone came out. You can do things you hadn’t foreseen before…. Everybody’s vision seems to be moving toward the idea that there is a piece big enough for everybody in this pie. The opportunities are endless.”

DIY companies are also getting in on the action.

August Pro division was formed to take advantage of the professional security channel, says Michael Buckingham, director of August Pro, August Home Inc., San Francisco. “Traditional security has been looking for ways to grow out of their space, which traditionally has been about 20 to 25 percent of American households. That has been stagnant for the last 20 years. If anything, this market expansion provides more opportunities and as more players produce products compatible with the industry, undoubtedly it will expand. If we can expand that market share it is best for all.”

Scott Harkins, vice president connected home, Honeywell Building Technologies, Atlanta, points to the DIY trend as just the tip of the iceberg. “When you elevate from security to smart home, the industry that has benefitted most thus far has been the security dealer, because of the willingness to pay a monthly fee that seems to just keep getting higher. That attracts the interest of the DIY companies and that is why they are coming in. I wouldn’t be surprised if we started to see utilities or the insurance industry, too. There are more players entering in different ways beyond what we are used to talking about.”

Many of the newer entrants from inside and outside the security space are attracted by the relatively low penetration rate into homes that the professional security market has had thus far, along with the attractive prospect of the lucrative RMR. They see 80 percent opportunity.

“Looking over the years at the security market, it has not grown, although the number of homes and businesses has, says Jorge Perdomo, senior vice president corporate strategy and development, MivaTek, Freemont, Calif. “We are focused on looking at that remainder that is non-traditional.”

Springfield, Mo.-based DMP has traditionally played more in the commercial security space, says Mark Hillenburg, executive director of marketing. “We haven’t had a product that really competes in the residential market until last year. But that is our biggest opportunity for growth. We are not going to step away from the commercial, but the penetration rate there is 85 to 86 percent and only 23 percent on resi. There is a lot more upside on the residential side.”

Chasing this seemingly big market may not be as easy as it looks, however. Tonti of MONI Smart Security sees a natural barrier in the price of these services. “When you start to add IoT components, that can start to get a little pricey and become a natural inhibitor,” he says. “My projection is we will end up somewhere between 25 to 30 percent of new customers doing connected home.

“I think there is potential for growth, but I don’t think it will double. I think what will drive that will really have to be a sea change in terms of how the components work. When you look at a $30 to $50 monthly fee on average, there is only a finite percentage of customers who will want to pay that.”

That is in line with what Herscovici predicts, as well. “We look at homes as a percentage of broadband households and we have about 23 to 24 percent of those households…. We see growing that to 30 percent.”

Still, a 5 to 10 percent growth would be far more than the market has seen in the past several decades, Todd Johnson of Capital Connect says. “We have already seen some expansion…. We have seen that number 20 to 25 percent as long as I have been in this business. That tells us that is the security number. I don’t think that number will go down, so the only way it goes up is if there are other things beyond security that you are offering.”

Dealer Ray Gurski, owner, RMG Security Solutions Inc., Gilbert, Ill., is optimistic that the pie will indeed grow for all, but only as technology and solutions change. “People don’t want the old-style panels. Everybody wants to use the phone to do everything. It will move the needle soon. The economy is moving now and people want this. They want to close their blinds with the push of a button. I think it will move within the next year or two.”

It is all about convenience — which leads to stickiness, points out Warren Hill, product marketing leader, security, safety and smart home products, Interlogix, a Lincolnton, N.C.-based part of UTC Climate, Controls & Security, a unit of United Technologies Corp. “For the consumer that interacts with security or life safety, how often do they do that? The smart home makes it so we use our phone to unlock doors or turn off lights. There is a convenience factor. Dealers can rest assured that homeowners will continue to use that system and they will be willing to pay that bill because it is adding convenience for them.”

That is good news for the traditional security market, Mayne says. “Consumer ads and social media are all driven around ways to engage devices as part of your normal daily life. It is moving from a cool technology to part of your daily routine. That is the key win for the security industry. The more this becomes part of what they do when they get up and before they go to bed, the more value we have.”

EMBRACE THE EXPERT ROLE

Whether the overall pie grows to 30 percent or 80 percent, right now the professionally installed and monitored security players are still in an incredibly strong position to capitalize on it — provided they keep up with the fast pace and get on board, if they haven’t already.

Blake Kozak at IHS Markit says the growth in the past year was led by more marketing and consumer education from several sources, but that the growth really came from the professional security channel. “Although DIY is certainly helping to introduce consumers to the connected home, the professional channel was more successful in 2016. Despite advancements in consumer awareness, challenges that hindered growth were cost and interoperability. For the DIY approach, the smart home is expensive.” A true connected home cannot be achieved for less than $1,000, and it can be complicated for the DIYer to do, he says.

That is why homeowners are more likely to turn to the “experts” who have the systems and solutions that make it all work together — the security channel.

Nick English, national sales manager, Kwikset, Lake Forest, Calif., says dealers need to take advantage of the opportunity to be the educator. “I can sell you a security system with a connected door lock, install everything and walk out the door; but that isn’t the full job. I need to show you how to enter the code and turn down the lights and thermostat and help you set up those things and take the time with you to teach you how to interact with the system. Too often the dealer sells, then moves on.”

That could be a mistake for another reason when it comes to connected home devices. Studies show that consumers that buy a connected product for the first time will likely buy at least one more within the first three to four weeks of purchase.

“The biggest opportunity for dealers selling and installing connected home products is the ability to remain in touch with the consumer,” Kozak adds. “Smart homes start off small, regardless of whether they are professionally installed or a DIY project. This means the dealer should be going back to the consumer at least once every quarter to query about getting more devices installed.”

He adds that going to the consumer over time reduces the “sticker shock” of how much these systems cost, as well as the stress of having to do it all at once.

James Rothstein, senior vice president global security marketing, Anixter Inc., Glenview, Ill., says this year and going forward is a golden opportunity. “I’m optimistic that security dealers’ expansion within the home will be very positive for the industry in 2017. Homeowners are realizing the benefits of a connected home and are particularly concerned with security. Those looking for comprehensive home security solutions will be a significant driving force in the industry this year,” he says.

The August and XFINITY Home study supports this. It found that when it comes to adopting smart home technology, family safety is the motivator for 63 percent of consumers, followed by convenience features that have a safety aspect such as ability to turn on lights after dark (54 percent).

“Security and security monitoring remains one of the top reasons end users are adopting connected home equipment and to that point, any company that can offer that seamlessly to their customers will continue to contribute to the overall market with the potential of becoming a major player,” predicts Chris Carney, co-founder of Abode, Palo Alto, Calif. “Interoperability, more specifically lack thereof, continues to be a factor limiting the growth of the connected home market…. For consumers there are many choices when purchasing connected home products, which can lead to confusion among end users about which devices work together.”

Kerber says the consultative sales approach, which is the bailiwick of the professional dealer, is critical right now in the connected home space. “Dealers are benefitting from that strong sales channel and consultative sales process. That is what is needed because at this point that is very low. They are optimally positioned at this point.”

Another differentiator the security dealer could have is cybersecurity, which is something the security industry is coming up to speed on and may not be the forte of some of the other players, particularly DIY. Helen Heneveld, president, Bedrock Learning Inc., Holland, Mich., and SDM columnist, says, “It is coming and if you don’t watch it and look at it you are going to be passed by. Dealers are in the best position because they are already in the home, they have an RMR model, they are trusted and they have a longer-term relationship. The opportunity as a trusted professional is to step up and be the hero by providing IoT security in the home.” (For more on this, see Heneveld’s column, Smart Insights.)

Whether they are aware of it or not, most security dealers large and small have the capabilities right now to be offering at least interactive if not full connected home products and services, Klein says. Most major system manufacturers in the security space have standardized on Z-Wave and added that capability to their panels and products (along with others such as Wi-Fi).

“The vast majority of sensors used in residential home security can be multi-purposed,” Beliles adds. “The door or window contacts can be used to trigger an event. We see this as a real opportunity for the dealer channel to get more involved in the home automation front.

This leads to an increase in RMR, Klein says. “You have an opportunity to go back to that customer and raise that RMR. You can go from $25 to $49 a month because you are adding the ability to monitor temperature and control lights. That is huge.”

This has been the case for Johnson’s company, he says. “We’re historically up about $8 in RMR per customer and that is all attributable to people paying for more than one automation device. We wondered whether people really would be willing to pay $69.99 a month and the answer is yes, they are.”

CHANGES & CHALLENGES

But as already noted, there may be a limit to how much that RMR can go up before the consumer balks — or until the industry reaches the finite number of customers willing to pay it.

“There is a high monthly cost associated with alarm monitoring and many consumers are simply not interested in alarm monitoring, which is evident in the stalled penetration rate of 22 percent in the U.S.,” Kozak says. “As a result, the ability to continue to bring new consumers into the channel with security as the cornerstone is an unsustainable model.

“The challenge of the connected home right now is finding an RMR model and offering ecosystem options that appeal to the various types of consumers,” Kozak adds. This is something more and more security industry companies are starting to understand.

“The high monthly revenue we are seeing from the combination of security and home automation will reach a peak and then start to come down,” Tonti predicts. “The reason it keeps going up is we subsidize a lot of the equipment and that will have to change.”

This might mean a tweaking of the model, Harkins says. “There are different models that have to be explored. Maybe they become both a traditional security player at $40 a month and also a smart home provider and get RMR out of a more DIY self-installed model that is different and maybe only costs $19 a month (See related sidebar, “DIY or Die?” at www.SDMmag.com/diy-or-die.)

“The security space has the best opportunity to become that trusted smart home provider. It might not include the RMR at a level they are used to, but there is an expansion opportunity there. Lead with security, but become the smart home pro.”

This is what Vivint is trying to do, says the company spokesperson. Vivint recently introduced Flex Pay, a new payment plan that allows customers to pay separately for products and services. It also announced in May a partnership with Best Buy that will place a Vivint smart home expert in the store to help customers design a comprehensive system, receive professional installation and monitoring.

Kerber sees growth potential in lower monitoring prices. “We asked people with a smart smoke detector whether they would want it monitored. Sixty percent said they would pay up to $10 a month. There are a lot of ways to cut this and that market opportunity will be significant.”

The industry is actively experimenting with new models, something Mayne views as a positive thing. “I think you see this industry working towards models that will break through that barrier and that is encouraging. Is it going to be on-demand monitoring, or do-it-for-me or DIY that expands? Is it integration with some of the newer IoT devices entering the marketplace? The business model is shifting and evolving, but it is encouraging that the industry is working to do that. I don’t know what the winning answer will be but I love that we are providing the tools that allow dealers to expand and experiment with new ways to market and there will be a winning model that comes out of that.”

However, Shawn Welsh, senior vice president of product line management and marketing, Telguard, Atlanta, cautions there is a potential downside to playing too much with RMR models. “There are solutions out there from DIY and others that are $0 RMR and they earn their revenue from other sources. The security industry needs to look for solutions that don’t pit them against that ecosystem, but one that allows them to do security and do it well. There are a lot of solutions available today that do pit us against free services that are out there.”

It’s hard to compete with free. But Welsh and others get back to the security play and the importance the customer places on that.

“Security is a very powerful and important piece of the connected home for most consumers,” Hevia says. “If you ask consumers what they would like to remotely control, invariably it is something that makes their home safe and secure. They love to see loved ones come home safely or remember to arm their system. Most everything except thermostats becomes a security play. The more our industry can provide a full suite of solutions, the better.”

Welsh adds the best place to pick up business is still from the existing security customer that may want one or two connected devices to try it out. “Capitalize on that interest without having to go waist deep. There is plenty of opportunity with people looking to dabble in the connected home and that would be the first, best opportunity touch those customers.”

Nobody can predict where this market is going, but most agree it will change. The key is for the security dealer to navigate this change in the meantime. “If we don’t go out and market it strongly as an industry, someone will do it for us,” Hevia says. “You see what just happened with Amazon getting into groceries. It is always better for an industry to do it themselves than to wait for someone else to usurp your reason for being.”

The same goes for dealers at all levels. Kerber notes a trend of smaller dealers not growing at the pace of the market. “Whether they are slower to adopt interactive technology and push through home controls, or not investing in the training, that trend is worth noting for sure.” They are losing share, he says.

This is a trend Harkins has seen, as well. “My biggest worry is some of the professional security dealers are just not adapting to these new technologies. I have had conversations with dealers that think these new tech giants are threats to them so they won’t enable it even as they get calls asking if they integrate with this or that…. I truly believe that to remain relevant in a landscape under attack from new professional models, it is adapt or die. Three or four years from now, those not offering something like this are likely to have a challenge in growing their business. Consumers expect it and everything is connected.”

Harkins ends on a high note, however. “This is a super exciting space right now and moving at a pace the security industry hasn’t traditionally moved at. We need to be getting that knowledge, adapting and moving really quickly because that is the consumer expectation. Being willing to test new models is critical. It is a fun time to be a security professional in the smart home world!”

The ‘GAFA’ Effect

A few years ago, a new acronym appeared on the horizon — GAFA (Google, Apple, Facebook, Amazon). GAFA are the giants of the consumer world, with deep pockets and an interest in being on the forefront of technology innovations. With the exception of Facebook, GAFA have been exploring the connected home space for a few years now. So far it has been mostly beneficial to the security industry, but if there is one worry many point to, it is that GAFA could become competitive instead of cooperative.

“You see Amazon starting to get into this game, but really they just want Alexa ever present in your house to buy things,” says Peter Tonti of MONI. “They haven’t made overtures to building an ecosystem, they just want their platform to help. Apple will do something with Homekit and Google with Google Assistant is similar to Amazon and Alexa. All these players will do something and what is going to be interesting is those platforms may have a lot of consumer appeal. To the extent that someone uses Apple in their home, they will say they want whatever they buy to be compatible with Homekit and they won’t be willing to pay an added fee for control because Homekit does that. That is where there will be some pressure on revenue down the road, when these truly consumer-facing brands start to get into the home control business.”

The general consensus is that if GAFA choose to get into the market, they could be a big disruptor, but other than keeping an eye out, there isn’t a big worry right now.

“It is really about where does everybody bring value into their ecosystem,” says Johnson Controls’ Roger Barlow. “Google may say they want to get into it, but they will never do security as well as we do. As long as everybody understands we are an important piece of the pie, I think it will go well.”

One reason not to worry is the size of the industry, says DMP’s Mark Hillenburg. “Look at what happened with AT&T Digital Life. They said, if you are going to be a division you have to be 1 billion customers or we are not interested. They managed to build it to 600,000 and most alarm companies would think this is phenomenal. But they thought, ‘Ho Hum.’ With GAFA there may not be as much there to keep them interested as they think. Time will tell.”

Another challenge that GAFA would face is the service aspect of the industry, says Resolution Products’ Dave Mayne. “The security industry has been built around a service mentality, helping people understand the technology, bringing expertise that is delivered in a personal engagement across-the-table format. There is tremendous value in that and that is not a strength of any of the GAFA businesses.

“I am optimistic that security providers will remain part of the connected home for the foreseeable future and these new entrants will only create lift and growth. GAFA will come to respect the capabilities that exist in security and continue to find ways to work with us as opposed to displace us.”

From Interactive to Connected: 2020 & Beyond

Security dealers have been involved in the interactive security space for several years now — but there is still a percentage that doesn’t offer it. Connected home industry insiders say this is a mistake. Not only is it a good idea on its own, but it will likely lead to connected products over time. Industry experts weighed in on the interplay between interactive security and connected home as well as what the landscape may look like in just three short years.

Nick English of Kwikset puts the number of dealers not participating in at least interactive at about 30 percent, based on a recent session he gave at ESX. “Seventy percent in my training class knew about connected products, but 30 percent were completely new to it.”

Telguard’s Shawn Welsh says that these dealers who haven’t already better get onboard with interactive because it is “table stakes now and will definitely be by 2020. If you don’t have it by then you will be a dinosaur unless everybody suddenly falls out of love with apps.” He adds that selling interactive now is a critical gateway to connected in the future.

“When it comes to takeovers, I don’t think dealers are thinking about adding the interactive services and that is what they need to be doing more of. It is not just a routine swap. This is an opportunity to upsell them at this point to that interactive services offering and it is a lost opportunity for many dealers. Because at that point you are not investing heavily in hardware, so asking them for a little bit more per month could lead to even more connected offerings later on.”

Peter Tonti of MONI says many of his dealers are actually having the reverse experience, for now. “[They] are all trying to target the home automation market and most of the time they end up with an interactive sale. That is not surprising because that is the middle range. But you can always add on. The challenge is how to market the base beyond that initial sale, which is a change to the industry.”

But he adds that by 2020, “the amount of stuff we sell that is not interactive will be less than 1 percent. I think that interactive will shrink overall because the connected home will take more and more, but almost everything will be at least interactive.”

Daniel Herscovici of Comcast sees interactive really growing. “We are upgrading non-interactive to interactive. We have seen substantial conversion in that category.” He notes a little more than half of his potential customers have non-interactive security systems. “With all the advertising and discussion about what interactive offers, we will upgrade systems and that produces a lot of growth for those players focused on interactive systems.”

Tom Kerber of Parks Associates says interactive services is growing at a significant rate. “In 2021 our estimate is 60 percent of those who have professional monitoring will have interactive. Today that percent is 40, and it is going from 15 to 24 percent for systems that will also have some sort of home control component.”

John Pirrie, vice president of product, SecureNet Technologies, Lake Mary, Fla., adds, “Interactive services from a security perspective will continue to offer new capabilities and tools for the dealer, including greater hardware, software, and central station integration. For consumers, the user experience will continue to improve, becoming more simplified and intuitive. There will be more options for connecting devices across multiple protocols within the home. There will be more proactive interactions through analyzing data and machine learning with virtual assistants playing a role.”

The Role of Voice & Video

Two technologies stood out as ones that drove the connected home space in 2016 and will continue to do so: Voice and video.

Blake Kozak of IHS Markit says, “2017 will be the year of the camera, but the industry will also start to see more connected appliances and voice control being integrated into more devices around the house, from lamps to thermostats and wall sensors.”

According to IHS research, they are well on their way. Globally in 2016, 35 million devices were shipped with the capability to be controlled through a voice assistant (although only 10 million were actually used that way). By 2021, IHS predicts this number will be 220 million.

“What Amazon has done with its Echo products, whether they intended to or not, was opened people’s eyes to this whole home control opportunity,” says Mitchell Klein of the Z-Wave Alliance.

Voice lowers the adoption barrier, adds Helen Heneveld of Bedrock Learning Inc. “Not only that, but another big deal is the experience. Last night I said to Alexa, ‘Set the alarm for 10 minutes.’ I was making apple crisp. My husband asked, ‘Who won the world series?’ That experience is important.”

ADT integrated Amazon Alexa with ADT Pulse just recently, says Jason Shockley, ADT spokesman. “Our customers not only love controlling their smart home features through the convenience of voice, but also operating security features like a disarm function via a PIN that is verbally communicated,” he says.

On the video side many dealers point to residential video sales as being particularly strong last year. In fact, Ben Brookhart, CEO, Power Home Technologies, Raleigh, N.C., attributes his company’s 20 percent growth directly to the Skybell doorbell camera. “The Skybell allowed us to grow in this space and sell additional door locks and other cameras,” he reports.

Peter Tonti of MONI says video is its own category, with about 20 to 25 percent of new sales including cameras today. “We do have customers that have a Nest or an Arlo that isn’t tied in.” But he adds that the potential for video to play a vital role is there. “Could I envision a time where you don’t have an alarm system as much as cameras with intelligence that spot a person that is unknown and sends an alarm? That could be viable at some point.”

Check out more SDM State of the Market Reports

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!