FINANCING

Despite Pandemic, Security Industry Seen as Financially Sound

Some large borrowers continue to face challenges, but acquisitions have resumed. How are values holding up? That depends who you talk to.

PeopleImages/E+ via Getty Images

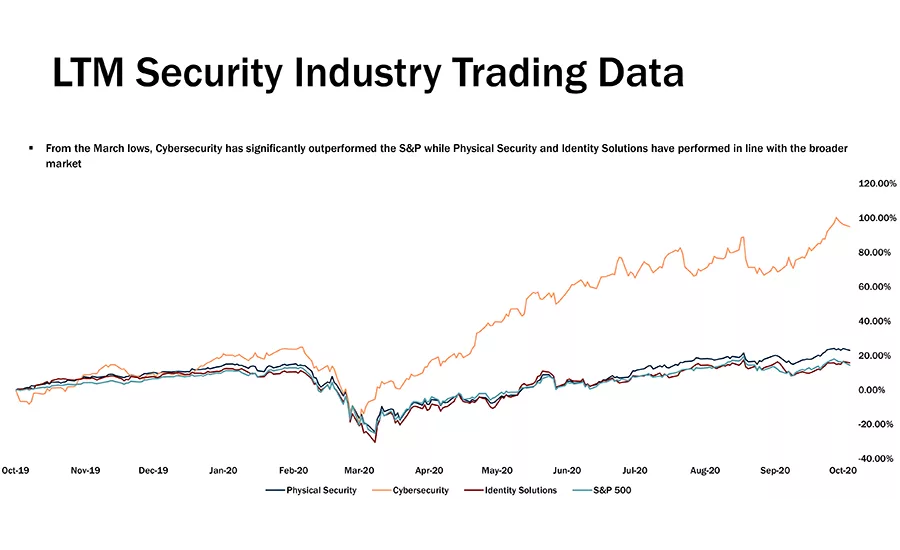

From the March lows, cyber security has significantly outperformed the S&P while physical security and identity solutions have performed in line with the broader market.

CHART COURTESY OF IMPERIAL CAPITAL

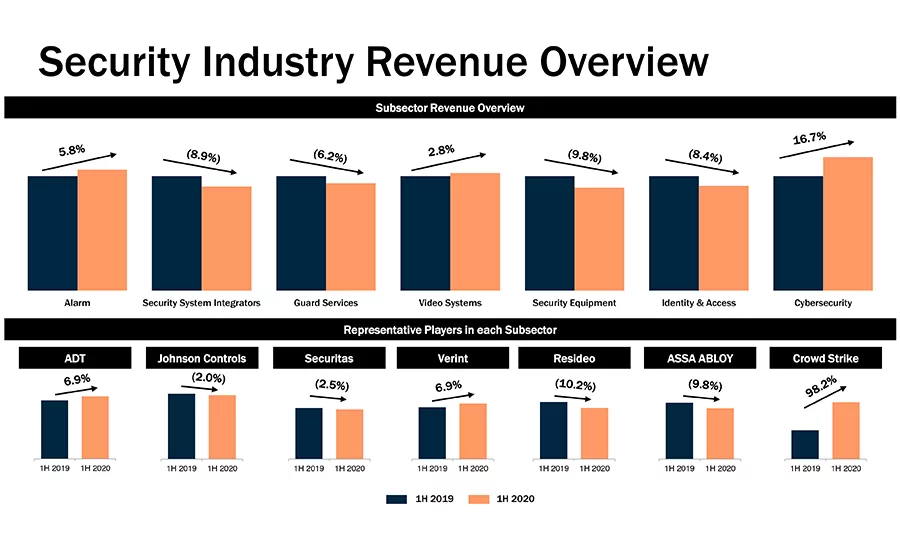

Alarm and video systems have seen growth in 2020.

CHART COURTESY OF IMPERIAL CAPITAL

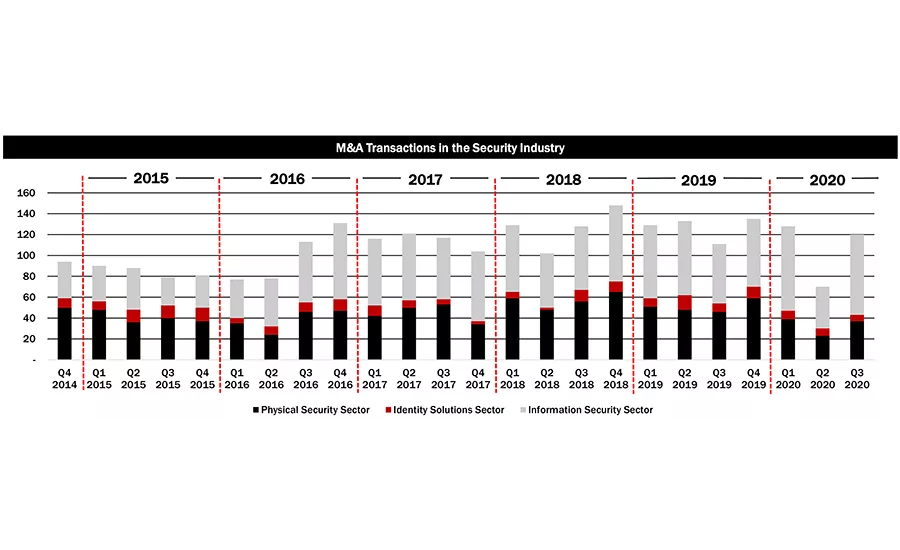

Q2 2020 activity highlights a major pullback in the M&A market due to the COVID-19 pandemic.

CHART COURTESY OF IMPERIAL CAPITAL

Even before the COVID-19 pandemic drove widespread stay-at-home orders, 2020 was shaping up to be a challenging year for larger security dealers. As SDM reported last year at this time, at least two banks that had been major lenders to those dealers had either stopped making new loans or had begun imposing terms that were less favorable to the dealers. And there were concerns that this might have a ripple effect by reducing the number of buyers in the market, thereby reducing how much remaining buyers would pay for new acquisitions.

It’s hard to tell how big that ripple effect would have been, because the COVID-19 pandemic put numerous pending deals on hold. Today, however, sources involved in the financial side of the security industry see acquisitions resuming, and some even see values in the range of what they were seeing before the pandemic.

Virtually everyone we spoke with sees a high level of confidence in the security industry overall.

As David Stang, founder and president of Stang Capital Advisory LLC, notes, lenders don’t want to make loans to an industry, such as tourism, that is unable to operate in a pandemic. Stang Capital Advisory raises debt and equity for security dealers and other companies.

Security dealers were designated as providers of essential services, and although new business may have slowed down during the pandemic, Stang notes that attrition was low — in part because customers were not moving.

The exception, of course, was for dealers with a higher percentage of businesses such as bars, restaurants and gyms that in some cases were forced to close by pandemic-driven shutdowns (more on that later in this story).

Jim Wooster, president of Alarm Financial Services, a San Rafael, Calif.-based company that makes loans to small- or medium-size security dealers, argues that the COVID-19 crisis has demonstrated the strength of recurring monthly revenue (RMR).

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

“Lenders understand there may be short-term hiccups, but the underlying collateral is really sound,” Wooster says.

Jim Stewart, president and founder of Legacy Security Consulting, a security industry broker with offices in Bend, Ore. and Memphis — isn’t aware of any security dealers declaring bankruptcy since the onset of the COVID-19 pandemic. As he puts it, “Investors and buyers see the industry as bullet proof.”

Mark Melendes, managing director and group head of CIBC Bank, which lends to security dealers from its U.S. headquarters in Chicago, echoes those comments: “COVID proved how resilient the industry is.”

Loans

People involved in the financial side of the security industry are often bound by confidentiality agreements and are not always willing or able to share information about clients, so they tend to talk in broad terms. And each person’s perspective is shaped by their unique business relationships — which means that SDM heard some conflicting information about the state of lending and acquisitions in the industry.

For example, several sources note that new lenders have come into the market, but we heard differing views about whether the new lenders have filled the void left when some banks began to phase out https://www.sdmmag.com/articles/97509-monitronics-bankruptcy-watershed-development-or-non-event their involvement in the market. Some sources — including Stewart and Ron Davis, CEO of Long Grove, Ill.-based Davis Mergers and Acquisitions Group Inc. — see new lenders having largely filled the void.

Private equity firms are getting more involved in the security business, Stewart notes. He estimates that in the past, about one in 15 deals that Legacy Security Consulting was involved in were based on private equity financing. Today, that number has doubled. Others see it differently, though.

The amount a lender is willing to lend is a multiple of RMR. And as Mark Sandler, managing director of SPP Advisors LLC, a Charleston, S.C.-based company that advises security dealers, explains, lenders traditionally made loans based on a multiple of 23 to 25 times RMR. But for a period ending in 2019, some went up to 26 or 28.

When Monitronics filed https://www.sdmmag.com/articles/96678-monitronics-brinks-home-security-files-for-bankruptcy-protection for bankruptcy and concerns about competition from DIY security systems rose, the lenders that had been the most aggressive stopped offering loans at the higher multiples, and in at least one or two cases, opted not to make new loans.

According to Sandler, there are some security dealers that had received loans based on the larger multiples that have not yet refinanced and will not be able to get new loans based on the original multiple when the current loans expire because “that deal doesn’t exist anymore.”

If those dealers have enough cash to pay off a portion of the loan, they may be able to get new financing at a lower multiple. If not, their options are less positive.

Over the next year, “some of the large deals will settle out, either through a sale or refinancing or a restructured balance sheet,” observes Sean Forrest, CEO of Alarm Funding Associates, a West Chester, Penn.-based alarm funding and acquisition company.

Flexible Loan Terms & PPP Help Dealers Make It Through the COVID Crisis

Although the security industry has fared better than many other industries during the COVID-19 crisis, dealers have nevertheless faced challenges.

With customers encouraged to social distance, many have been unwilling to allow technicians into their homes, which means installation and service calls dropped substantially — initially, at least.

Dealers have mostly been able to make payroll and keep technicians and other employees on staff. This was made possible, in part, by lenders that offered more flexible terms and, in some cases, by the Paycheck Protection Program (PPP).

Some lenders, including Alarm Financial Services President Jim Wooster and others, allowed dealers to pay interest on loans during the pandemic, and delay paying off principal.

The PPP was established by the federal government in the CARES Act adopted after COVID-19 was declared a national emergency.

“It was our experience that security companies made good use of PPP,” Melendes says. “We saw a high degree of participation, and we saw the industry use it for the right reason — to retain employees. . . . PPP helped out and the industry really took advantage of that.”

Acquisitions

Virtually everyone we spoke with agrees that acquisitions in the security business essentially came to a halt in March when COVID-19 was declared a national emergency.

According to some, though, acquisitions rebounded several months later. Stewart, for example, had 17 deals in the pipeline when we spoke to him in November. Others say the market is still slow.

Sandler sees buyers unwilling to pay top dollar because there is too much uncertainty about attrition rates as a result of the COVID-19 pandemic. As a result, buyers are unwilling to pay high multiples, and sellers may prefer to wait rather than accept the price offered.

As with loans, security dealer acquisitions are typically expressed as a multiple of RMR — and here, too, the people we spoke with had different views about current values.

While Davis has seen a slowdown in deals made, he says values haven’t been impacted.

“Deals at traditional metrics of 36, 37 and 38 are still done on a regular basis,” he says.

Stewart says the amount buyers were willing to pay for security companies declined in the early days of COVID-19, but valuations are rebounding.

He cites the example of a client that tried to sell in the early days of the pandemic and couldn’t get a multiple of 32. More recently, however, the client closed a deal at a multiple of 38.

“Multiples are down but not like six to eight months ago,” Stewart says.

Sources who are most familiar with larger companies seem to be the least positive. For example, Forrest says multiples are down.

“Much of that comes out of the ability to finance a deal,” he says. The availability and terms of loans impact the acquisitions market because buyers often need financing to make a purchase. If a lender isn’t willing to lend as much, the buyer can’t afford to pay as much.

According to Forrest, “There are not enough lenders, especially for multi-bank deals.” Dealers wanting to borrow $50 million to $200 million generally must obtain several smaller loans from different lenders, he explains, and nowadays that’s difficult.

Dealers seeking loans are also facing tougher scrutiny, sources note.

Wooster says, for example, that buyers are looking closely at the types of business accounts a potential acquisition serves. Concerns center on businesses such as bars, restaurants and gyms that have seen closures during COVID-19.

Buyers “are not always saying they will change the price, but they will hold back more,” Wooster says.

Hold backs are a common practice in security dealer acquisitions. The buyer pays a portion of the selling price up front but agrees to pay the remainder later, with deductions made if attrition exceeds a certain threshold.

Moving Forward

Although some sources are more optimistic than others about the current state of security dealer finances, virtually everyone we spoke with was positive about the future.

Forrest see the industry outlook as “good.” As a result of civil unrest this summer, he sees a greater need for security, and he adds that, “With COVID, we’ve been able to prove ourselves. Continuity plans were in place and dealers continue to operate and drive the customer experience and financial metrics.

“This is as severe as anything any of us have lived through and that’s great for our industry,” Forrest says.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!