State of the Market: Alarm Systems 2010

Change can also come in the form of a dying technology, evidenced by the estimated 700,000 land lines that are being cut per month, or in the fact that the entire House of Representatives is up for election this year.

Talking to dealers, installers, distributors, manufacturers and analysts regarding the state of the alarm market in 2010 reveals a market that will continue to change under the influence of myriad factors. Embracing the resulting change — and generating some of your own — will be the difference between having a “poor” year and an “excellent/very good” year.

Of course, some changes happen faster than others, and while everyone wishes the economy would fall into the list of fast-moving change in 2010, experts and key factors driving the alarm industry’s revenue indicate that isn’t going to be the case. 2010 is the year to get through, and 2011 is the year that everyone will really feel the relief. Analysts at ISBWorld predict security industry revenue will still decline about 2.1 percent in 2010, although it will improve considerably at the end of the year. Considerably higher growth is expected beginning in 2011 — at 3.5 percent and beyond. This matches the Federal Reserve Systems’ Federal Open Market Committee’s (FOMC) projections for output growth, unemployment and inflation in 2009, 2010, 2011 and beyond. The projections were that a slow-shrinking unemployment rate, continued tight credit conditions, households’ continued struggle to pay down debt and a still-weak demand for housing, among many other issues, would hold back the speed of the recovery through most of this year, with a strengthening upturn late in 2010 and into 2011. SDM’s own Forecast Study, conducted annually since 1981 among subscribers, showed similar results. Total annual industry revenue declined for the first time since the Forecast Study has been conducted, at a rate of 7.8 percent in 2009. Dealers and integrators predicted a further overall decline of 1.6 percent in 2010. All of these factors play into the alarm market.

Alarm dealers made numerous changes during a tough market in 2009 — shaving margins paper thin, tightening budgets, adjusting target markets (residential versus non-residential, new construction versus retrofit, etc.) and more. With that in mind, many dealers say they are navigating the slow beginning of the recovery by digging in with changes they’ve already made, paying attention to the changes coming — especially changes in technology and user expectations — and focusing on future success rather than just right now.

“If everything I hear is to be believed, 2010 will be a far better year than both 2008 and 2009, but certainly not back to what we would call ‘normal,’” says Wayne Boggs, president, Richmond Alarm Company, Richmond, Va. “Still, I fully expect 2010 to be a very good year for my company, and myself and my employees are going to do everything we can to achieve that goal.

“Our greatest opportunity this year will be in integrating new service offerings and leveraging technology to meet the real or perceived needs of the consumer,” Boggs adds. “My plan is to make a greater investment in marketing and do it in new and innovative ways, to try to get ahead of my competitors.”

Michael Allen, founder and co-owner of Southern Utah Alarm, Cedar City, Utah, also emphasizes the innovative approach to business in the current market, saying the growth is already there — if you are looking for it.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

“2009 saw an economic downturn that has not been seen in decades. We already started to see slow but steady — steady being the key word — growth towards the end of 2009,” Allen says. “This year, there is money out there you just have to be willing to search longer and in places you would not have looked in the past.”

The concept of “looking in more places” is one of the keys to success this year, according to John Sullivan, vice president of sales, ADI, Melville, N.Y.

“We’ve been focusing more on niche markets in the security space to help our dealers remain competitive. We’ve introduced them to expanding segments: outdoor perimeter protection, remote control solutions, home solutions, emergency response systems, home automation and wireless. We’ve increased training opportunities to help dealers get into new markets, cross-sell and up-sell, find opportunities to increase RMR, and offer adjacent products.”

HB Alarm Inc., Cranston, R.I., provides a broad range of security and fire alarm systems. In 2010, the company is focusing on keeping expenses low and outdoing the competition.

“New home construction has ground to a halt. People can’t sell their house, so they can’t move and put a system in the next house. It is a domino effect that still isn’t over,” says John Bourque, HB Alarm’s chief executive officer.

“Because it isn’t over, this year is really all about surviving and putting yourself in a position to come out of the recovery in a better position than your competition,” adds Bourque, a 20-year First Alert Professional Dealer, whose company has been in business since 1971. “2010 is the year to cut expenses, and yet still be open to possibly picking up some new staff from your competition for the benefit of the future.”

Like Bourque, many dealers are looking to use the high unemployment rate to their advantage, picking up fresh talent made available in the current job market and justifying the extra payroll as a way to come out stronger when the economy really picks up. And they’ll still have time to do it, as experts are predicting unemployment, one of the factors playing into the economy’s recovery, to remain high into 2011.

The majority of the Federal Open Market Committee appears to see unemployment remaining high into 2011, with growth remaining weak in 2010.

Why watch the unemployment rate? It impacts the public’s perception of the economy.

“I think the public perception of the economy — that jobs are insecure, that more layoffs may be coming, that economic growth is lagging — are all reasons for the slow sales of security in general, and both the residential and commercial burglar alarm markets are affected by these perceptions,” says Boggs.

The public’s perception of crime will also continue to be relevant to the 2010 alarm market. Some areas in the country have seen rising crime rates and increased sales as a result.

Ironically, while crime, or the public’s perception of crime levels, generally aids alarm sales, the numbers just aren’t there for the country as whole. Data from the FBI’s semiannual Crime Index indicates that crime isn’t rising. In fact, the latest available data, released in December 2009, shows that in 2008/2009, crime fell in all 10 reported categories, including robbery, property crime and burglary.

“We have not seen any increase in crime in Virginia, and our unemployment numbers are better than the national average, but the perception is still there,” Boggs says. And that’s what counts.

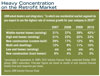

CHANGING INSTALLATION MARGINS

One big change dealers expect to continue in the upcoming year is a shift in installation margins.

Family-owned Per Mar Security Services, headquartered in Davenport, Iowa, has provided total security solutions since 1953. The company experienced the same reduction in installation margins due to increased bids for jobs.

“We are seeing more competitors bid on public jobs than we ever have in the past, and the margins are thin to secure the business,” says Brad Toliver, vice president of electronic security, Per Mar Security Services. “On a positive note, we have done a nice job of reviewing our installation practices and job costing on a regular basis, which has had a positive impact on our installation margins, due to increased efficiencies.”

David Balestrery of Sentry Security in Wheeling, Ill. is tackling lower margins with adjusted commissions and negotiations with vendors.

“There is definitely price compression on new alarm installations,” he says. “We are probably averaging a 10- to 15-percent decrease in total sales per install, partly due to a reduction in scope per the customer, and some price concessions. Sentry’s install profit has suffered minimally due to top line revenue compression; however, we have reconfigured sales commissions and negotiated price decreases from vendors to largely cover price shortfalls.”

CHANGES IN LEGISTLATION AND ORDINANCES

The alarm industry doesn’t have just the economy and strong competition to worry about in 2010. It has elections to pay attention to as well. The alarm industry always has its fair share of issues to attend to in Washington and with state and local governments, but with all of the members of the U.S. House of Representatives up for re-election, 36 of the 100 seats in the U. S. Senate up for grabs, 36 gubernatorial races and more all occurring in the 2010 elections, experts are predicting a flurry of legislative activity this year. This heightened political activity, which is already high due to the economy and troubled budgets, will affect most alarm dealers.

The director of government relations for the Electronic Security Association (ESA), John Chwat, predicts a flurry of political activity affecting the alarm industry this.

“Every government action,” Chwat says, “is going to affect business operations one way or another, so it is important to keep up on the government relations section of the ESA Web site, keep up on alerts that are sent out, and become vigilant and active in your state.”

Stan Martin, executive director, The Security Industry Alarm Coalition (SIAC), Frisco, Texas, says that in addition to new legislation at a federal level, ordinances will continue to change on the local level as well.

“In 2010, we’ll see more ordinances get more aggressive and become more restrictive in the sense that dealers and customers can expect fewer free alarm dispatches before fines are imposed, the amounts of fines will most likely increase, and we may see more departments move to some form of limited or no-response to alarm signals as departments work with less dollars in their budget,” Martin says. “This is just another reason for dealers to utilize two-call verification, CP-01 equipment and improve their training of the system users.”

SAYING GOOD-BYE TO POTS

The alarm industry is in the middle of a technology evolution, and 2010 will bring continued change. One such change many see picking up speed this year is the decline of plain-old telephone service (POTS). According to Jonathan Klinger, vice president of marketing, Honeywell Security & Communications, Melville, N.Y., this trend is poised to have just as meaningful of an impact on the industry this year as the more frequently mentioned economy.

“The growth of cell-only homes and concerns with VoIP (voice-over Internet protocol) will drive demand for GSM-enabled systems,” Klinger says. “Twenty percent of homes are cell-only now. Another 20 percent are cell-primary, and quite irrespective of the state of the economy, many of those consumers will shift to cell-only.

“Because today’s end-user is more likely to live in a home without a POTS landline, more likely to use smart phone-based applications and more likely to own a flat-screen TV, digital picture frame and/or GPS navigation device, they are therefore more likely to require a system with a GSM radio for alarm signaling, be more interested in remote interactive services … and be more demanding with respect to product aesthetics and ease-of-use,” Klinger points out.

POTS is becoming more and more of a technology on the brink of extinction. In a recent report to the Federal Communications Commission (FCC), AT&T claimed that, “with each passing day, more and more communications services migrate to broadband and IP-based services, leaving the public switched telephone network (PSTN) and plain-old telephone service as relics of a bygone era.”

As the POTS era draws to a close, Klinger emphasizes dealers’ role in the change. “Dealers have a tremendous role to play and a tremendous opportunity to explain to consumers as to why having GSM or using it as primary is a critical link in a secure home,” says Klinger. “A dealer who understands the transition taking place and offers GSM as a primary means of operation has the means to grow their sales and increase their recurring monthly revenue,” he says.

James Rothstein, Tri-Ed’s senior vice president of marketing at the Woodbury, N.Y.-based distributor, sees this trend as a reason to be optimistic about 2010. “The factors behind our cautious optimism for 2010 are the following: the evolution of burglar alarm panels is continuing to move forward, adding more convenience and more value with advanced technologies such as touch screens, synergies with GSM communications (data and two-way voice), size of wireless devices and home automation capabilities. These features will improve the overall perception of the value of an alarm system in one’s residence. The smaller- to medium-sized custom-oriented residential companies leverage this added-value in systems. Many of the mass-market companies leverage the advances in speed and ease of installation. Both of these factors mitigate, to some degree, the negative economic climate,” he explains.

Tom Mechler, product marketing manager, Bosch Security Systems Inc., Fairport, N.Y., adds IP communications to the list of growing trends.

“We’re seeing a faster rate of growth with our IP communications modules, driven, in part, by end users who want to enhance security and reduce costs,” says Mechler. “The cost for phone lines can range from $15 to $30 per line, per month, depending on the telecommunications service provider. For an organization with multiple control panels, eliminating the need for these phone lines instantly cuts recurring operating costs for their intrusion system.”

A NEW USER EXPECTATION

The transition away from POTS isn’t the only new characteristic of end users in 2010.

Sullivan says ease-of-use is another common user expectation that companies will see more often.

“Residential users are looking for systems that are easy to use and manage. They are attracted to solutions with a graphical user interface, communication capability and wireless ability. Non-residential users are interested in remote control, partitioning, multiple user access and reporting capabilities.”

This is echoed by Mark Ingram, vice president of sales, Visonic Americas. “Systems that work are easy to use, fully functional, do not false alarm and work the way engineered are critical to end users,” he says. “It is imperative that manufacturers continue to build products that always work and never give rise to performance issues.”

But most agree that consumer demands will change as the price on currently “high-end” systems drops down and end users’ expectations continue to be influenced by other technologies in their lives.

As Klinger explains, “Consumers don’t relate to products and technologies in market-specific silos. Their experiences with cell phones or laptops or televisions influence what they expect for a security system.”

And they come to expect the instant information that is available in so many other places, as Alison Slavin, vice president of product management for Alarm.com, points out. “A significant trend is that consumers today expect to have instant access to information about everything that matters to them — the weather, their bank account, local news, sports scores, etc. — from anywhere, at any time, through their phones, PCs and other Internet-connected devices. Information about the security of their home and belongings, and the well-being of their family members, is no exception to this trend.”

“What has traditionally been called a keypad should really now be an interactive window of information with applications that we could offer that would not only increase our revenue, but, just as importantly, also elevate our perceived value,” says Bourque.

“We think there’s a great opportunity in 2010 for those security dealers who can respond quickly to the above trends and offer their customers Web-enabled security services that go beyond traditional systems and don’t rely on a landline phone or broadband connection,” says Slavin.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!