State of the Market: Alarm Systems 2016

Alert Protective Services’ Chuck Mishoulam says the security alarm market has changed dramatically, particularly with interactive services, growth in new construction and an increase in competition.

Photo by BOB STEFKO Photoraphy for SDM.

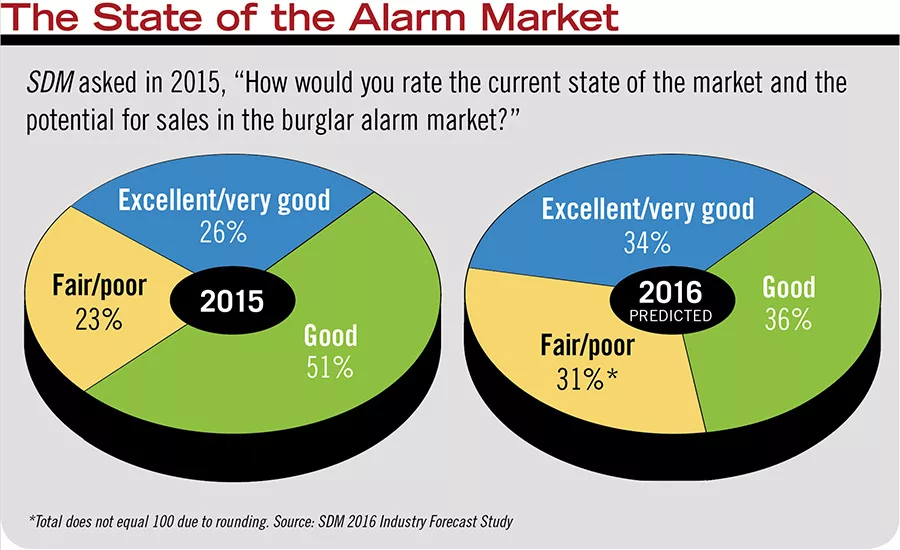

The State of the Alarm Market

When asked (in 2015) about the current state of the burglar alarm market, 26 percent thought it was excellent; when asked to look ahead to 2016, an even greater number — 34 percent — said they anticipate an excellent market for sales.

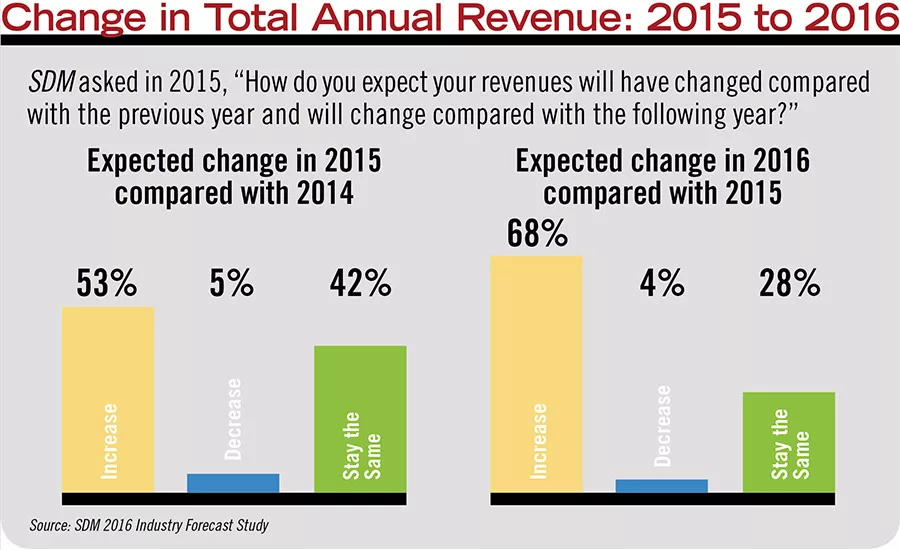

Change in Total Annual Revenue: 2015 to 2016

Dealers’ and integrators’ expected revenue change for 2016 is more positive than 2015, with 68 percent of respondents to SDM’s Industry Forecast Study saying their 2016 total annual revenue would increase this year.

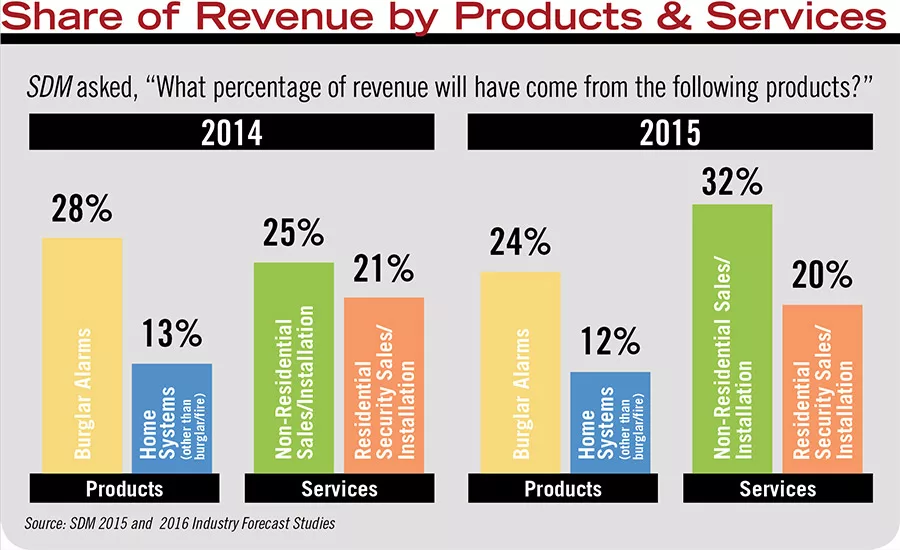

Share of Revenue by Products & Services

In 2014 dealers and integrators indicated that 28 percent of total sales revenue would originate from burglar alarms, while in 2015 that number declined just slightly to 24 percent of all revenue. Non-residential sales and installation, however, went up from 25 percent to 32 percent.

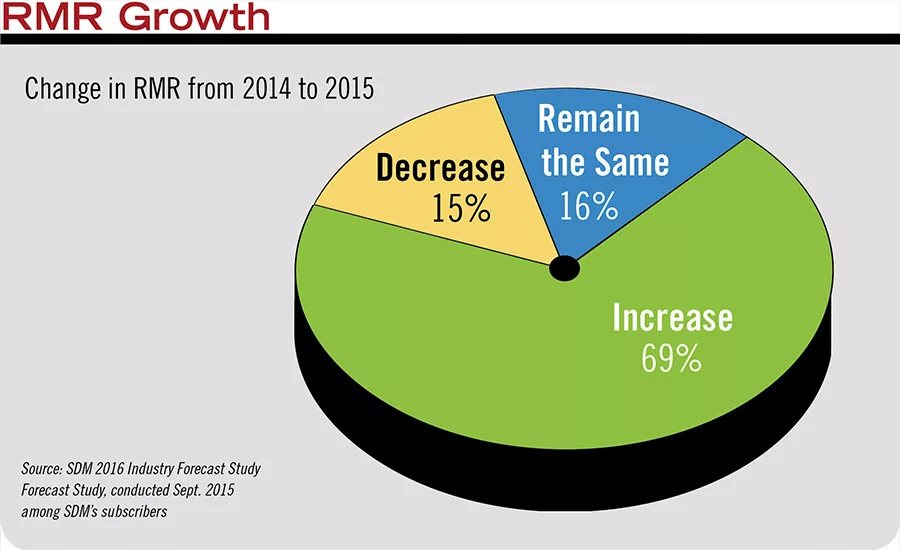

RMR Growth

Almost seven in 10 respondents reported an increase in their recurring monthly revenue (RMR) in 2015, up 8 percentage points from last year’s study. The average RMR increased by 45 percent.

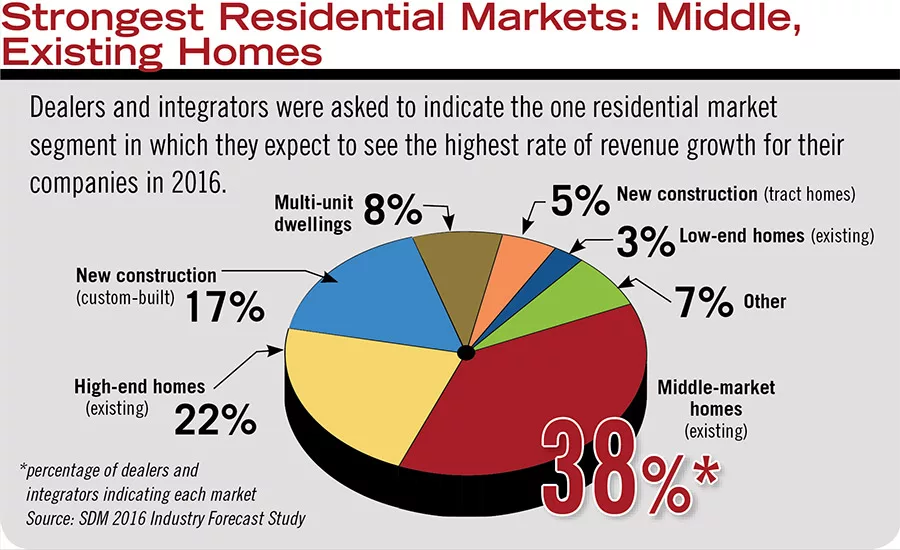

Strongest Residential Markets: Middle, Existing Homes

More than six in 10 installation companies that serve the residential market rely on existing homes for both new and add-on sales. There are 117.3 million households in the United States, according to the National Multifamily Housing Council.

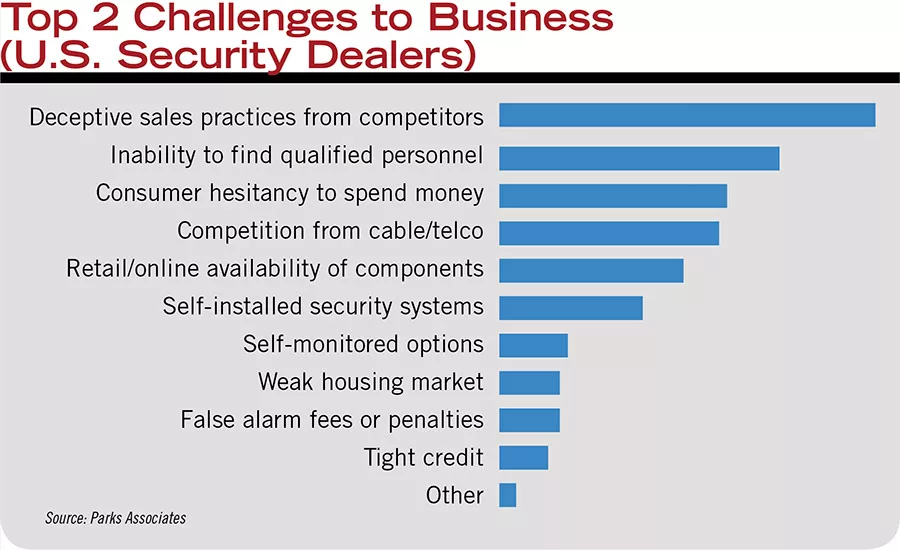

Top 2 Challenges to Business (U.S. Security Dealers)

Parks Associates asked dealers to list their top two biggest challenges. Way out in front as No. 1 is “competitive sales practices.” DIY and MIY also made the list.

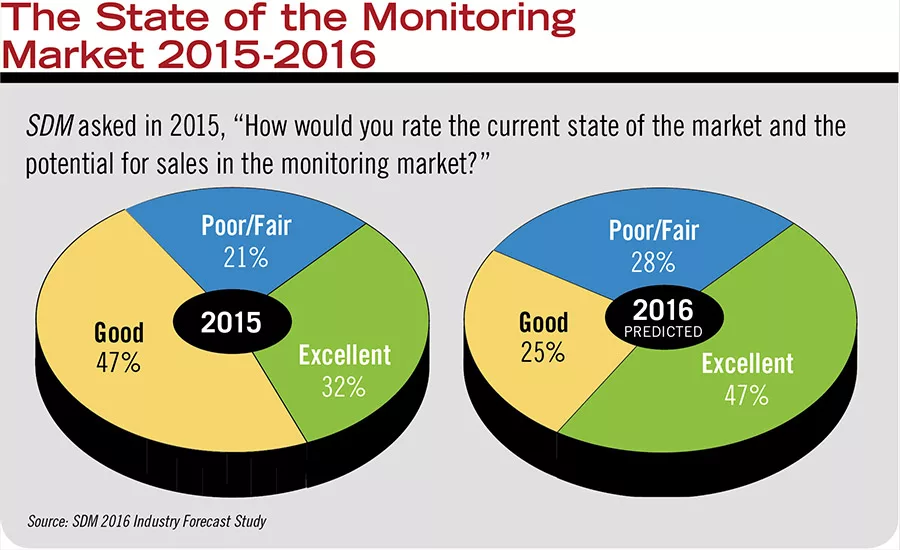

The State of the Monitoring Market 2015-2016

Weighing in on the state of the market for monitoring, almost eight in 10 dealers and integrators participating in SDM’s Industry Forecast Study reported either “good” or “excellent” results in 2015; and 72 percent predicted the same for 2016.

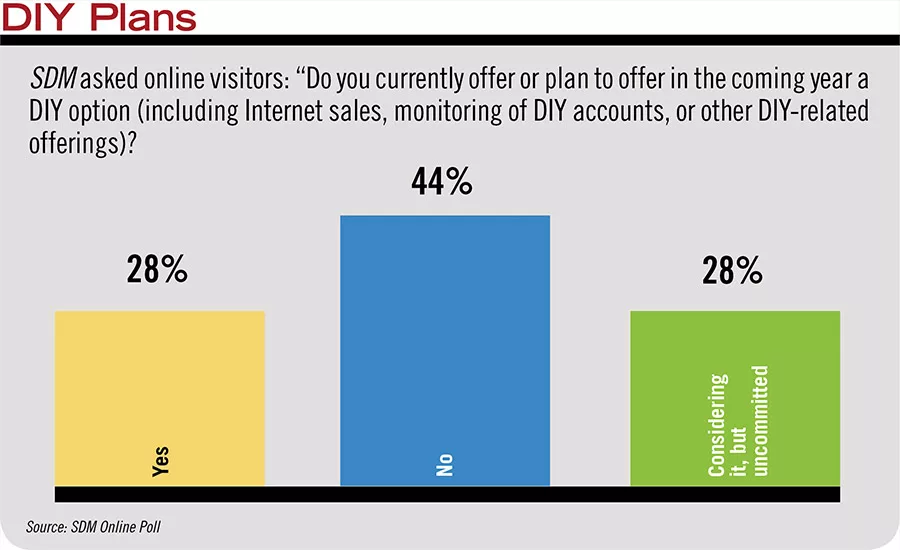

More than half of respondents are either offering or considering offering DIY security in the coming year.

It’s an election year — and a strange one at that, so far. For most of the summer and fall none of the “traditional” rules of politics seemed to apply: the young people were making their voices for change heard in the polls; many of the most popular candidates were playing to voters’ fear; and in the end it’s anybody’s guess what is going to happen. In many ways, the security market is experiencing a similar situation.

Particularly on the residential side, the security and monitoring space has changed more and faster in the past few years than the previous 30, causing a massive mind shift for all of the players involved. Every month sees more new and different players and technologies entering the market, and the Millennials are becoming a major discussion point. At the same time homeowners and business owners alike woke up one morning last November to an entirely new climate of fear and unease as they watched the Paris attacks. A few weeks later it hit home that this could happen here, when two extremists attacked a Christmas party in San Bernardino.

On the face of it, these events wouldn’t seem like they could impact the market so swiftly; yet many are seeing a trend.

“I think there is a growing sense of fear and unease in society,” says Keith Jentoft, president, RSI Video Technologies (Videofied), St. Paul, Minn. “After the San Bernardino shootings it seemed like the world was getting more chaotic and violent. People want peace of mind.”

And that peace of mind often comes in the form of security systems. Some feel this is happening more on the commercial side, but others have noticed a shift across the board.

“People are becoming more safety conscious,” says Rory Russell, owner, Acquisition and Funding Services (AFS), Kattskill Bay, N.Y. “With the greater affordability of interactive security alarm systems, a larger span of socioeconomic groups are utilizing these services.” Home and business owners want to protect what they have, protect their families and businesses. They want to feel safe in an unsecure world, rift with local and national security threats that may pose potential personal harm to self, family and treasured possessions.”

ADT, Boca Raton, Fla., has seen this play out in recent sales numbers, says Jim Vogel, vice president of dealer business. “Some of it is anecdotal, but I think folks are becoming increasingly aware of what it will take to protect their families, their businesses and their homes. We saw a bump in demand after Paris that was counter to the seasonal trend. It was a definite spike versus a year ago. It is sort of an undercurrent, but as I speak with our dealers and ask them what is behind it, this is what they say.”

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

This could be a temporary bump, however, cautions Pat Comunale, president of global security, Anixter, Glenview, Ill. “From an economic standpoint, what is happening in the world today is putting security front and center, whether that is residential, commercial or even personal protection. We live in a different time right now. Since we have had two recent, significant events it is in everyone’s minds. But if nothing significant happens in the next six months it gets put on the back burner. If these events continue to be in the news it becomes a driver for people. It’s just the world we live in.”

Indeed, for SDM’s 2016 Industry Forecast Study, conducted last fall (before the events in Paris), SDM’s readers were asked about their experiences in 2015 and their expectations for 2016. When questioned about the factors that would most affect sales next year, terrorism ranked 0 percent. However, general crime, which had ranked fourth the previous year, was bumped to second, with 14 percent of respondents naming it. Economic conditions remained No. 1, with 33 percent, perhaps reflecting the uncertainty of what the next year will bring with the election.

The world has changed on more than just the national security front. For security dealers there has been a much more seismic shift away from the way things have been done forever. As cable and Internet companies come into the market and offer security as part of their offerings — at a much lower cost — and consumer electronics manufacturers offer more and more do-it-yourself (DIY) offerings for sale online and at mass market retail stores, the traditional security dealer is having to change quickly, or get out.

Dave Sheffey, senior vice president of sales, northern region, Napco Security Technologies, Amityville, N.Y., put it succinctly: “The commercial side is growing fairly well and the residential side is changing dramatically.”

This is not necessarily a bad thing, but it is a challenging opportunity, he adds. “I can’t honestly say residential is growing; we are cutting the pie differently. There is more DIY today than three years ago. We are seeing the Internet play a bigger role and there is a lot of influence generated by interactive service…. For the singularly focused alarm companies coming in and starting out and looking for a product, the whole model is changing. When we look at how it is changing, we have to adapt to that and also migrate into areas that are still viable and profitable for a company like ours.”

They are far from alone.

“What I have noticed is there is finally a realization in the industry that the industry isn’t going to keep being what it was,” says Pam Petrow, president and CEO, Vector Security, Warrendale, Pa. — SDM’s 2015 Dealer of the Year. “That is hard for an industry that has remained unchanged for almost 30 years. We have figured out the world has changed. These new entrants are here to stay. How do we learn from them? How do we fit into this picture? There is a lot of opportunity, but it is not the same opportunity.

“This is the new us. We have to react faster, process faster, clear things faster, and be much more nimble. That will be our challenge, because we were relatively slow-paced before.”

It’s a very exciting time in the industry, says Dave Mayne, vice president of marketing, Resolution Products Inc., Hudson, Wis. “Yes, there are a lot of questions and unknowns, but I like that the industry doesn’t seem to be running from it. As a matter of fact it is embracing it. I see people considering and changing and investigating how they can make [these changes] a part of their business.”

Chuck Mishoulam, president, Alert Protective Services Inc., Chicago (featured on this month’s cover) is definitely in that category. While he sees the new entrants as a threat that is “definitely eating into some of the marketplace,” he also views it as a trend that is growing the overall pie and something that could benefit all. “Traditionally the market share in security has been rather small and stable all these years. It has definitely become more robust with all the stuff going on in the marketplace today.”

Market Outlook By The Numbers

When asked generally about the market for 2015, both SDM Forecast Study respondents and dealers and manufacturers interviewed for this article were generally positive (with the majority reporting double-digit growth). But many also inserted small notes of caution for the coming year, even as the outlook continues to be generally positive.

The good news: Burglar alarms topped the list of products by revenue for the second year in a row, with dealers and integrators indicating that 24 percent of sales revenue came from alarms in 2015 (the next highest was access control at 17 percent). While this is down slightly from 28 percent in 2014, the number of respondents listing home systems (other than burglar and fire) remained steady at 12 percent. (See chart, page 80.)

However, while a whopping 82 percent predicted overall growth would increase in 2015 in last year’s survey, only 53 percent reported that actually would happen in 2015. The outlook for 2016 is a little more modest, with 68 percent predicting growth in total annual revenue. (See chart, page 79.)

“Business has been good in the industry,” says Michael Flink, president, ADI Global Distribution, Melville, N.Y. “The market was up in revenue and somewhat flat in unit sales. The average selling price of a system was larger this year due to more connected features….There is a high level of optimism about the trend continuing from last year. But talk of recession and global economic concerns or unstable stock markets can lead to consumer pessimism.”

This is also reflected in the SDM Forecast Study results on the current state of the market by product niche: The number of respondents reporting the burglar alarm market as “good” or “excellent” rose from 70 percent in 2014 to 77 percent in 2015. Slightly less believe 2016 will offer a more robust state of the market — 70 percent, although 34 percent predict it will be “excellent.”

The monitoring segment fared better, with 79 percent overall reporting the state of the monitoring market to be “good” or “excellent” in 2015 and 72 percent predicting the same in 2016 (with almost half predicting it will be “excellent”). Not surprisingly, confidence in the home control/home entertainment markets is also on the rise, at 65 percent positive in 2015, up from 58 percent in 2014. Forty-two percent believe 2016 will be an “excellent” year in that niche, with a 70 percent overall positive outlook.

Petrow says her company’s RMR was up about 12 percent to 14 percent in 2015 over 2014, according to preliminary numbers. “We had a good year. We are not totally closed yet for 2015 but all numbers indicate that we will surpass 2014 and we are anticipating that in the budget for 2016.”

SDM Forecast Study respondents generally concur with this assessment; a healthy 69 percent of dealers and integrators reported increased RMR in 2015 over 2014. (See chart, page 82).

Manufacturers who offer interactive service products were also bullish on 2015/2016.

“AES Corp. performed well in 2015 as the need for technology at the end-user level continues to evolve,” says John Milliron, vice president of sales for North America, AES Corp., Peabody, Mass. “The industry climate appears to be better now than it was in 2014…. AES expects continued growth in 2016. The strength of our business partners in the marketplace coupled with exciting applications and products that generate RMR will be the primary drivers.”

Larger companies such as ADT reported a “terrific” year in 2015. “On the dealer side we grew just under 5 percent year over year on the strength of higher productivity with our existing dealers…. In terms of both growing and retaining business, an awful lot has to do with the expansion into home automation. We have increased our Pulse offering take rate to just under 60 percent when a year ago it was just under 40 percent. It increased 20 percent in a year,” Vogel says.

According to Parks Associates, Dallas, the professional alarm business had a good 2015. “That was the result of multiple factors,” says Tricia Parks, CEO and founder, Parks Associates. “No. 1 there was a bit of a housing recovery, including new starts, which we haven’t seen a lot of since 2010. No. 2, you had a higher volume of moving households and specifically into owned homes. Third we had a clearing out of the foreclosures. The adjacency of smart homes as offered by Comcast, AT&T and others tipped some households on the fence over into professional monitoring. Lastly, there was a pent-up demand for renovation or replacements from people who had been putting it off. This year went up in actual numbers and even more in sold replacements.”

Nearly 6 million professionally monitored homes had smart home control in 2015, according to recent Parks research.

But this pent-up demand now being met and foreclosures cleared out also means those factors won’t be there in 2016 and there will be more of a levelling out, Parks predicts.

Another good market indicator comes from the acquisition side of the industry. “Buyers are paying top dollar right now,” Russell reports. There may be ups and downs, but the overall outlook is rosy. “The economy is not going to be fantastic this year because it is an election year and the stock market is doing its dance. But there are not any great economic fears. There is plenty of capital out there right now to buy companies at very good multiples. The banks are lending.”

However, Russell and others suggest the outlook may not be as healthy for small dealer companies, particularly ones that haven’t fully gotten on the interactive services bandwagon or are half-hearted about it. On the other hand, those that are enthused about interactive services report the best results, regardless of size.

“We had a great year,” says Marvin Smith, president, Orlando Emergency Signal, an independent dealer based in Orlando, Fla. “Our sales were up 31 percent, and 80 percent of that came from the residential market…. The biggest change has been going from takeovers and retrofits to more new home sales. We are doing more new installations than in the past. The other change has been remote connectivity. More and more that is just the expectation.”

This is the wave Mishoulam rode to a double-digit percentage growth over 2014, he says. Although he describes his company as a “larger small-size” dealer, he reports a 10 percent increase for 2015 and is optimistic for 2016. “As we came out of the recession I think we are starting to come back in a larger way. As the market has changed we have tried to change with it with interactive services. That is what is driving this business right now. New construction is certainly on the uptick. There are more new housing starts, especially here in Chicago.”

Greg Rhoads, automation director of marketing, Leviton Manufacturing, Melville, N.Y., agrees. “With homes finally starting to be built again in the past year or two, things are improving and those projects planned in 2015 are going to be executed in 2016.”

In an October 2015 report on electronic security products, commissioned by the Security Industry Association (SIA), The Freedonia Group, Cleveland, Ohio, reported, “Through 2019, demand for electronic security products is projected to rise 7 percent annually to $16.2 billion. Strengthening construction expenditures are expected to drive demand following the recession-impacted 2009–2014 period. As a result markets that are projected to experience the strongest growth in new construction — including offices and lodging, and residential buildings — will see the fastest growth.”

Comunale views the changing security space as a potential market driver more than a potential loss, even for smaller dealers. “Small dealers that continue to buy from us continue to grow. It is still a healthy space. We heard for years that we have penetrated the residential space in the area of around 25 percent. Potentially with DIY and connected home we have the ability to try to grow that to a 50 percent penetration rate. A rising tide lifts all ships. There is a lot of growth left in the security space.”

The inhibitor is affordability, Parks cautions. “For the upscale homes, the top 20 percent to 30 percent, if they wanted security they tend to have gotten it. You really need to break through to that next level of socioeconomic households and affordability remains an issue. Can that be fixed? Great question. If you had told us [a decade ago] that everyone would be paying $150 a month for their mobile phones we wouldn’t have thought they could afford that. But they are. It is also possible the marketplace just has an inherent top. Parks Associates doesn’t forecast professional monitoring going to 30 percent or beyond in our forecast period through 2021. However, getting there represents strong growth given that only about 18 percent had monitored security at the end of the recession going into 2012.”

Competitive Pressures

One of the biggest potential roadblocks to growth on the security side, particularly residentially, is increased competition from two fronts that are not only inundating the market, but doing it much less expensively.

The average price of a traditional residential security system, according to SDM2016 Industry Forecast respondents was more than three times the price of the mass market offerings, with a median price of $1,200 for traditional systems versus $99 for mass market systems. DIY providers topped the list of greatest competition this year, with more than a third of dealers naming them as worrisome.

“What has happened is, home automation went mainstream, meaning there is [less] money in it for the dealer,” Jentoft says. “At the recent CES show there were all these products that were a free app. How do you make money selling things that are free?”

It’s a growing concern for SDMMarket Forecast responders as well. In the 2015 study, just 4 percent listed “protecting profit margins” as a future challenge. This year, 14 percent named it as a challenge, bumping it 10 percentage points to the number two spot (after “increasing sales” at 22 percent).

But where some see competition, others see potential opportunity. “We are starting to see MSOs, cable and satellite companies really accelerating and having real success entering the security market, mainly on the residential side,” says Tom Mechler, applications design manager for intrusion, Bosch Security Systems Inc., Fairport, N.Y. “For the traditional dealer that is certainly a risk but also an opportunity, in my mind. There is the risk of outside force, yes, but there are these strong companies that are just blanketing the airwaves, which gives us all more exposure to the customer and the benefits we can bring to them.”

The key is to focus on better service, says Jim Corbett, partner, United Alarm Services, Brookfield, Conn. “I lost five accounts to Comcast and AT&T, and got four back because they do such a bad job at service.” But he adds that he sees an unfair advantage to these cable companies, who are able to play in the security space, but not the other way around. “I have cable in my house, and a security system,” he says. “I am paying the cable company for cable, which is essentially subsidizing them to be in competition with me. I can’t sell cable in my town, yet they can do alarms for free. Is that fair competition?”

These providers are increasingly becoming a part of the industry — like it or not — and many manufacturers of interactive products view them as customers just like any other dealer, albeit a significant dealer.

“Our deployment customers who range from ADT to Comcast with their Xfinity offering are starting to promote their subscriber numbers,” says Greg Roberts, vice president of marketing, Icontrol Networks, Redwood City, Calif. “ADT’s Pulse is over a million and a half and Xfinity was over half a million. We are starting to see that take hold in the market.”

Inside the industry pressures are there as well. In a recent Parks Associates study, the company asked dealers about their top challenges to business. (See chart, page 86.) Overwhelmingly, they responded “deceptive sales practices from competitors,” with nearly 50 percent listing that as one of their top two challenges.

“I’m not sure what to make of it,” Parks says. “Is that a sign of competitive pressure or are there a lot more deceptive practices going on? It is No. 1 by quite a bit. I don’t doubt that some of that exists, but it definitely shows that competition is fierce.”

Smith sees this first-hand in his business, along with another trend that he says hurts the smaller guy. “What I see hindering our growth is larger companies giving away systems or those that engage in unethical sales tactics. Companies that go door-to-door and convince homeowners that they are there to upgrade their current system (but are really there to sell a different system) affects the consumer’s trust and possibly pushes them more towards the DIY market…. Then there are those that are giving away systems, which also devalues what we are selling and installing. If customers see they can get a system for free, they question why.”

Mishoulam, too, has experienced deceptive competition. “We’ve seen companies go door-to-door and say ‘X’ company is out of business, which is deceptive. I have never really understood this. How can you [the homeowner] entertain changing your service to someone who just knocked on the door and told you something like that?”

This is one of the dangers of those trying to fight the practice, Vogel says. “It is a careful balancing act. We want to ensure we properly represent ourselves so that we don’t alarm customers by misrepresenting ourselves. When a competitive dealer tries to suggest they are representing a different company like ADT it is a bad mark on the industry. But on the other hand, the more we publicize it, the more we could impact the ability to go into a neighborhood that has had a spike in crime and [legitimately] sell door-to-door. But we won’t tolerate unethical behavior if it is impacting our customers, brand or business.”

Although her business is almost all commercial and government, Joey Rao-Russell, president and CEO of Sonitrol/Kimberlite Corp., Fresno, Calif., agrees that deceptive practices hurt the industry overall. “People buy from companies they trust. What these practices do to us as an industry is break that trust in our ability to provide a professional service…. It goes hand-in-hand with DIY, which is eroding what we have built as an industry for the last 50 to 100 years as being the ones to protect you. As an industry, that is a problem.”

Deceptive practices occur with the outside competitors, as well, particularly in their advertising messages and online reviews by customers, Mishoulam says. “You see these Angie’s List reviews of these DIY companies that claim, ‘I installed 15 windows and a smoke detector in three hours.’ That is physically impossible.”

Corbett has had multiple sales calls where the customer saw something on a commercial that wasn’t realistic. “One guy was actually told people don’t break into basement doors. That is the kind of thing happening because they only care about the RMR.

“Our job as a legitimate dealer is to educate the consumer about how things really work. You see these ads where police show up in one minute and that is not realistic. When we are in front of the consumer we bring those points up. ‘You saw that commercial on TV? Well let me tell you how it really works.’ Once you educate the consumer there is zero threat, but I was able to get in front of that customer. If I don’t, I see it as a bit

of a threat.”

Competitive pressures abound, and aren’t likely to abate any time soon. If anything there will be more and more coming into the security market. “The influence of companies like Google, Apple, Samsung and new start-ups in home automation are continuing to challenge the market to innovate and create new solutions that not only solve problems in the smart home market but continue to add value to the security and alarm piece of the equation, such as smarter peripherals with multi-sensing functionality,” says Lisa Turner, global strategic products manager, intrusion, Tyco Security Products, Westford, Mass.

This creates some uncertainty along with opportunity, Petrow adds. “I would say the biggest threat to our industry is not knowing how some of these new entrants are going to position themselves in the market. If you look at Google or Apple, we are really just a rounding error to them. We have no influence. They can change laws tomorrow with the power that they have. They are big. They are really big.”

She compares it to Uber in New York City. “How much was a taxi medallion worth five years ago versus now? People thought that couldn’t happen, but then a startup came in and totally destroyed the value of a cab medallion. When you see change like that, the risk to the industry is not recognizing that and not figuring out where you fit in that new landscape.”

Industry Efforts

Figuring these things out is top of mind for many integrators this year and last — from small, to medium to the “800-pound gorilla” in the room, ADT.

“Philosophically, perhaps we are now a 100-pound gorilla that is getting back in shape,” Vogel says. “We are a 140-year-old start-up business that just went public three years ago. Now it is about moving fast and furious to grow our dealers’ profitability by earning customers for life in their markets. We are doing this by taking advantage of our dealers’ entrepreneurial spirit and their willingness to be a presence in the market, not as the gorilla, but as a local company. Security is our core business, not AT&T’s.”

They are doing this, he adds, by meeting the competition head-on where they are most prevalent. “We have made available to our dealers a microsite to take advantage of online activities, and we have signed a national agreement with our friends at Yelp to provide that platform so our dealers are very much aware of what ratings and reviews can do for their business, both on the upside and the downside. We have dramatically increased our training, resources and partnerships in the digital space, which helps to balance our predominately ‘feet-on-the-street’ market approach. We are leveraging referrals. We have relationships with both USAA and State Farm to take advantage of where and when consumers are looking for security and home automation. If you are not there, you can’t win,” he adds.

The biggest opportunity and the biggest threat are one-in-the-same for 2016, says Anastasia Bottos, COO and chief strategy officer for Alarm Capital Alliance, Newtown Square, Pa. “Dealers who are able to evolve with the industry and offer customers the technology and customer experience they are demanding will be successful. Those who do not, will see increasing customer attrition and have a difficult time competing in the space long-term.”

Large dealers have the resources and financial capacity to do a lot to help themselves. But smaller dealers are getting on board in the past year, too.

“I see a healthy mix,” says Mike Hackett, senior vice president of sales and marketing and co-founder, Qolsys Inc., San Jose, Calif. “The larger dealers can invest a lot of money into Google search engines and move product that way. But even our smaller dealers are saying to themselves, ‘we have to have a website.’”

Change on the smaller end may be slower, however. Almost 60 percent of respondents to the SDM Industry Forecast Study reported having a social media presence in 2015, up just two percentage points from the previous year. But nearly 60 percent of those who don’t, have no plans to add it in 2016 either.

Still, whether it is a website or some other online presence, there is a shift to wanting to “up their game” and improve how they look to the consumer.

Orlando Emergency Signal’s Smith is in that group. “I think each year we do more, we advertise more. We also generate a lot of leads through social sites like Angie’s List….We not only focus on exceptional service to separate us from larger companies, we are happy to provide a 12-month contract. We don’t feel the need to lock them in to grow our business because history has proven that exceptional service means that our customers don’t leave us.”

Short-term or no-contract monitoring is something that is increasingly popular with the Millennial and DIY markets, who may be renters or simply don’t want to commit. (See sidebar, page 78.)

Howard Avin, vice president of sales and marketing, Nationwide Digital Monitoring, Freeport, Long Island, N.Y., says smaller dealers may actually have an edge when it comes to reputation. “The small and mid-sized dealer has always survived because a lot of people would rather do business with a local company than a conglomerate. It is true there is more competition, but no matter what we do we won’t keep them out, so it is better to latch on and ride the wave as best we can.”

Mishoulam is trying to take advantage of the opportunity the Comcasts of the world bring. “I think their advertising is actually good for the alarm industry. As they spread out their tentacles and advertise, we can offer everything they can and there are a lot who still want to turn to a local company. A lot of dealers our size are referral-based. We advertise on the Internet. You can’t discount these cable companies. They are certainly taking a percentage of the market and they are in our backyard. But if people are out there getting competitive quotes, we just do our best if we get that chance to bid on the same job and focus on our service.”

More and more dealer networks, industry association help, and other resources are available to dealers today. “Seeing that residential side and the rise of DIY installations and monitoring, it seems like the dealer networks that are out there should give the alarm industry some advantages over the typical Silicon Valley startups,” suggests Steve Schmidt, engineering manager, Underwriter’s Laboratories (UL), Northbrook, Ill. “A lot of these are neat gizmos, but the novelty of being able to watch the dog during the day wears thin after a while. The alarm industry is in a good spot with the pieces that are in place to differentiate themselves in terms of the quality of their service and ability to help people in ways the newer entrants might find challenging.”

Rao-Russell has noted a very positive trend in the industry recently. “It has been refreshing to see the collaboration and open sharing of a lot of the industry. Once upon a time we had our perspectives and we were very married to those and not open to new ideas, and I think it has been good to see those changes as we are more open to evolution and embracing opportunities…. [I think] we are recognizing that though we are in competition with each other, there is a much bigger challenge coming from outside the industry from the DIYs and the Googles. They have created challenges for us, but also had a positive outcome in that they opened us up to working together and sharing best practices.”

Icontrol Network’s Roberts has seen this recently, too. “We absolutely see them banding together. The reason I think we are seeing that trend now is because there was tremendous reluctance from the independent dealer to adopt these new smart home technologies. The industry now is looking to determine what are the ways for dealers to offer smart home technology as part of their security offerings in a way that doesn’t disrupt their business, so they can stay in business?”

Petrow, who is also the current president of the Central Station Alarm Association (CSAA) says her organization is committed to more and more education for the dealers. More than that, the organization is in the process of reinvention, as well.

“I just came back from a long-range planning meeting where we discussed ‘Who are we and what do we do as an association?’ People everywhere are reframing their businesses and what services they provide. The dialogue is incredible. We are not who we were and we will never be that again. It is about how we reinvent ourselves.”

Jentoft recommends focusing back on the basics — and the differences — of the traditional security market, which has worked hard for years to overcome false alarm issues and be a trustworthy source of safety and security. “If home automation has become a consumer electronic product, what you end up with is that security becomes more important and a greater differentiator than that home automation piece, which is free. We have to get back to basics because what was unique isn’t unique anymore. That is why video verification and police response will become more important, because that is what is left.”

THE RISING SUNSET

2016 presents a significant and unique opportunity for dealers. The home market has had a huge adoption of radios in recent years, and if a system is more than three years old it will have to be replaced or upgraded this year, due to the impending sunset of 2G on AT&T, which will cut off the service after December 31, 2016. Many, if not the majority of existing cellular-based alarm systems are on AT&T.

“I think there will be a rush to do the conversion of the cellular communicators,” Flink says. “This is the last year 2G will work. At the same time there is this exponential growth in connected services. We are starting down a path where non-connected panels will decline.”

These two events are going to connect in interesting ways. Since the last sunset in 2008, the entire landscape of security has changed. “Blood is in the water right now,” says Shawn Welsh, senior vice president of product line management and marketing, Telguard, Chicago.

“Everybody knowns the 2G sunset is really a ‘jump ball’ across the industry. It is an opportunity for things to change hands if it is not handled. The risk is much higher than before. Interactive services were not around in a real way in 2008. The number of devices connected by cellular was pretty small. We’re talking millions of units versus hundreds of thousands. Last time they procrastinated and were able to get it all done in a month. This time with the density, they can’t wait that long.” That is why this sunset is not the same as the one in 2008, Welsh adds.

Some dealers are farther along in this process than others. “Larger companies tend to be more proactive in upgrading,” Napco’s Sheffey says. “Everybody recognizes that this period of 2G sunset is different than the last, where everything happened at the same time. Then, consumer cellphones were changing, too. What is happening now is all consumer technology has already changed, so when the dealer goes back to the consumer they are saying ‘Why?’ They don’t understand that the 2G sunset that happened years ago for them is happening now with security and they think, ‘Why should I pay?’”

Large companies are able to offer incentives such as free radios, or discounts. But smaller dealers don’t have that kind of margin. Telguard launched a new program in February to help smaller dealers through their Telguard Freedom program. “It’s freedom from Sunset. We are giving them the hardware for free, paying for the installation and including for a fixed, monthly rate interactive services and all that we offer.

“We have a lot of technology and services we are building to help them be successful at doing that,” says Jay Kenny, senior vice president of marketing, Alarm.com, Vienna, Va. “People have to upgrade these aging accounts and dealers now have an opportunity to upsell or create a higher value account in that process.”

Many dealers see the cellular surge as a positive selling technique even beyond the sunset. “It is an opportunity for any dealer,” says Corbett at United Alarm Services. “People are always switching over to cable or Internet-based systems, but in my opinion they don’t work well in the alarm world. We convert about 90 percent of those systems to radio. There is a huge opportunity to increase revenue and give customers better security at the end of the day…. We have a lot of customers where their cable phone lines are pretty bad because [the companies] don’t know what they are doing with wire. It is a big opportunity for us.”

Whether it is a cellular sunset, adding advertising, educating customers or anything else, dealers are focused this coming year on changing with the times, something Avin has confidence they will succeed in.

“I have been in this business for a long time, since 1975,” he says. “Dealers have always survived, always found a way of doing more business. I do not see that changing. There may have to be a change in marketing or sales techniques, but they always find a way to get customers and keep them.”

Hybrid DIY – A Growing Market?

If the coming generation of security buyers isn’t interested in long-term contracts or having a professional installer come into their homes, where does that leave the traditional security dealer? In an effort to play in that world, some dealers are looking more to a hybrid approach, allowing customers to purchase online and/or offering to monitor their self-installed security system. This is a very new market, and one that isn’t without its dangers. But those who are looking at it see it as grooming a future traditional customer, which could have a big payoff.

SDMrecently polled online visitors to find out whether they had or were considering offering a DIY system or option. More than 40 percent said no, and another 28 percent said they were considering it but hadn’t yet committed. Videofied together with USA Central Station Alarm Corp. has an offering called DragonFly Security that uses a hybrid approach. “DIY is a mushy term because it means everything and nothing,” says Keith Jentoft. “This is self-installed but professionally monitored, so it still fits into the RMR business model sold by dealers. It allows even the smallest dealers to play in the DIY marketplace.” (See www.SDMmag.com/dragonfly-security.)

This trend is brand new, and therefore the numbers are skewed, says Pat Comunale of Anixter. “We do see some dealers doing DIY, but it is a very small base. We have projected to have reliably robust growth but not exceeding 7 percent or 8 percent of the total.”

Dave Mayne of Resolution Products agrees. “I see more dealers creating that type of DIY offering today. But it is probably premature to say that will be the new standard. Dealers today are for the first time investing in building that as part of their platform or offering and there are several large players in that space.”

For example, ADT just released a hybrid DIY service called Canopy at the latest CES show.

“Canopy is about this idea that both up-and-coming and well-established tech companies are introducing devices to improve the home experience,” says Jim Vogel of ADT. “We want to make it easier to attach our products to those devices. We know that there are DIY products out there where the customer is still looking for protection by ADT. Not only do we want to attach our devices to their devices, we want to attach our services to their devices.

“Dealers appreciate what ADT is doing for renters, knowing that at some point they will have a family and settle into a new home, and that is where ADT will be first to mind if we already have a relationship with them.”

Vector Security’s Pam Petrow agrees. "What I see DIY and MIY being is a stepping stone for people. There has never been that before. It gives them a chance to understand the value of security and the benefits earlier, which is great because I think that will ultimately grow the market.”

Vector is ramping up to do hybrid DIY. “Right now we are doing the installs. Our DIY offering won’t be out until a little later this year, but today they can buy it online and we will come out and install it. We are still vetting products to find one we think has that level of ease with the installation and is more false-alarm proof. You can’t just take a traditional panel and throw it on the wall. You have to make it much easier for a customer that doesn’t do this every day.”

For the time being, Howard Avin of Nationwide Digital Monitoring predicts this will remain in the realm of the medium to large dealer, for the simple reason of staffing. “You need two to five people in an office to set it up and send it out. I could be wrong, but I don’t believe that is the marketplace for the small to middle size dealer.”

Jim Corbett of United Alarm Services agrees. “If we don’t install and service it, we are not going to monitor it. It is not worth the aggravation.”

Chuck Mishoulam of Alert Protective Services said, “Most of the customers we are interested in are still more the traditional type of people and like to put the security aspect back onto us.” But he can see the future potential market.

“We have looked into monitoring DIY, but haven’t pulled the trigger on doing anything. It is easier said than done to do it right.”

A Different Sales Approach: Millennials Versus Boomers

There is a sharp distinction between the desires and drivers at the nearly opposite ends of the age spectrum for potential security buyers. Increasingly Millennials are making their presence felt in all areas, from the election to how they want to get their security. And they are a very different group than the previous generation of security consumers.

“I’m 50 and a lot of the security industry is closer to my age or older, than to my younger relatives,” says Dave Mayne of Resolution Products. “That generation tends to not want to have people into their homes. They live in apartments and they don’t want people to come do service work the way we grew up expecting that. There is an isolationist mindset, ironically driven by social media. They don’t want to schedule around someone else. If they can have it shipped to them, they would rather do it that way.”

One of the things Joey Rao-Russell of Kimberlite/Sonitrol has noticed is that selling to Millennials takes a different type of technique. “The sales person has to be more technologically oriented. They have to be able to talk and interact with these people, who want to see how it looks on their tablet. I have some wonderful older salespeople that have been with us for many years who, let’s just say they are not going to play on their phones.”

At the same time the demographic that buys a professionally installed alarm system is getting older and fewer, says Videofied’s Keith Jentoft. “If you are selling the same thing, there are the same amount of dealers selling to fewer people, which is declining over time. The Millennials and the people coming up are tech savvy and don’t want a professional installer in their home. They just want faster police.

“If you are going into it now, you had better have a good strategy for the Millennials because the growth over time is there. My generation is getting old, fat and dying out. You want to grow a business over time. If you don’t have a Millennial solution that is at some level a self-install, you are in trouble.” (See “DIY Hybrid Approach?” on page 77.)

On the opposite end of the age spectrum, the Baby Boomer generation, which has been the traditional market for professional alarms, may be getting on, but that doesn’t mean they aren’t ripe for a different kind of approach.

“There are many opportunities in the medical alert arena,” says Howard Avin of Nationwide Digital Monitoring. “There is a huge population that is getting older and they may not care as much if someone breaks in to steal something, but they are concerned about when they don’t feel well and can’t get up or there is a fire or carbon monoxide issue. When dealers are targeting the over-50 crowd, that should be in their bag of tricks to switch to something more than just burglary.”

This is a market Chuck Mishoulam of Alert Protective Services is very interested in for the near future. “One thing we are interested in getting into is PERS. The central stations now are more ramped up to handle that and this is a market that is just going to get bigger.”

Technology Factors

Being security technology experts is still the main focus for dealers and integrators, of course, and there are definitely some trends they are seeing lately. Commercially and residentially alike, they are seeing video everywhere. Whether it is video for verification, home video systems that let the user independently verify an alarm while on a phone call or text with the monitoring center, or IP-enabled video integrated with access control and other security technologies, video surveillance is widely seen as a major focus.

“There is an amazing change from 10 years ago where a lot of the discussion centered around ‘Big Brother’ to today where people want and expect cameras to be everywhere,” says Michael Flink of ADI Global Distribution. (See “Hand in Hand: Partners Through technology” on page 103 in this issue.) “They want video. We are starting to see an early trend around home video surveillance as well.”

Video benefits the industry in several ways, Resolution Product’s Dave Mayne says. “Where there is downward pressure on RMR, as you start to add more video, it raises the value to the consumer back up. There is the opportunity for video analysis — not just sending pictures but almost a more accurate motion detector. We are going to see more of that over time.”

Joey Rao-Russell of Kimberlite/Sonitrol agrees. “All points are starting to intersect. Video and analytics, as well as some of the automation pieces coming in and smarter devices…. Customers want more visual and tactile information.

“The millennials and their drive for technology and connectivity are producing innovation and change our industry hasn’t seen in many, many years. Each year it is expanding. In 2015 I saw many more commercial customers asking for notices on their phones and cloud services.”

This speed can present problems, however. “There is a lot of technology out there coming out very quickly without the normal vetting process, whether that is UL or whatever to make sure it is reliable,” Vector Security’s Pam Petrow says. “Some of these new products don’t have the standards we are used to. We have to be careful that we are close enough to getting the technology to our customers that we are staying on that edge but not so over it we are potentially hurting the customer.”

Still, no dealer can afford to ignore the new stuff. “We try to keep up with the newest products that are out there as far as interactive services,” says dealer Chuck Mishoulam, Alert Protective Services. “Whatever is new we try to stay on top of and embrace it, if it something we can try to sell. We can’t look backwards. We have to look forward.”

Technology, especially communication technology, continues to push the alarm industry forward, says Tom Mechler of Bosch Security. “We are seeing much more smartphone connectivity with push notification; POTS (plain old telephone service) continues to go away; alternate communication continues to accelerate. Those are the technologies dealers need to be on top of or they will get left behind.”

Jay Kenny of Alarm.com agrees. “I think there are key opportunities this year to create a higher value account by adding data. Accounts that log into a mobile app and have at least one device attached have much better attrition profiles than those that don’t and there is a ton of consumer interest and opportunity to capitalize on that. We believe there is a pretty significant opportunity for dealers to drive upsells and create enterprise value for their business by upselling their current install base. This is a meaningful opportunity where historically there wasn’t that opportunity.”

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!