Barnes Discusses Alarm Company Valuations at Conference

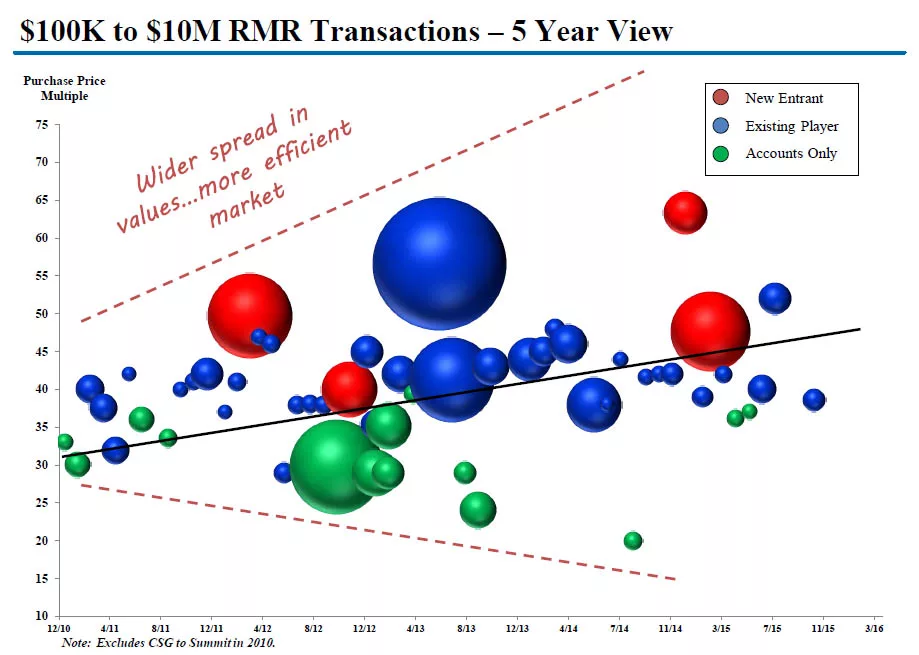

Attendees at the Barnes Buchanan Conference always look forward to Michael Barnes’ “bubble charts” showing the transactions that took place over the past year. In 2015, RMR in dealer program transactions traded at a weighted average multiple of 36 times, while RMR associated with alarm company operations traded at a weighted average multiple of 50 times (the latter of which was overwhelmingly driven by the 50 times multiple paid for Protection 1 and ASG Security by Apollo).

PHOTO BY SDM STAFF

The 21st annual Barnes Buchanan Conference — which aligns the security alarm industry with the financial sectors interested in the recurring monthly revenue (RMR) model — imparted a positive outlook on industry performance and countless options for making money. Held the first week in February at The Breakers Hotel in West Palm Beach, Fla., the conference was hosted by Barnes Associates, St. Louis, Mo., and Buchanan Ingersoll & Rooney, Pittsburgh.

This year’s conference featured six different sessions — from issues affecting alarm company operators such as cybersecurity and competition, to investment trends in the security business. However, the one session most attendees came to see was Michael Barnes’ two-hour Industry Overview. Based on a compilation of research from Barnes Associates, supplemented with additional research including SDM’s Industry Forecast Study and SDM 100, the overview examined four areas: industry growth; industry structure including the competitive landscape; operating metrics among security companies; and acquisitions/market values.

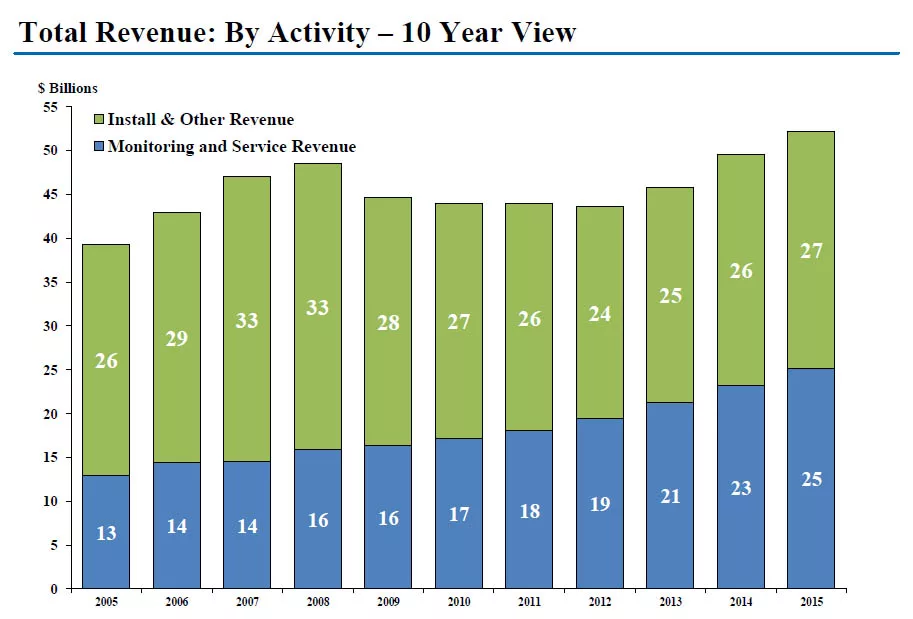

“In fact, another good year with growth up 5 percent in terms of total revenue for the industry,” Barnes pronounced, adding that total revenue for U.S. security alarm companies in 2015 had settled at $52 billion. “We’ve rebounded nicely since 2012, which was when the recession kind of ended for the industry...”

Barnes said that during the mid-1990s, the industry’s overall revenues experienced a 7 percent compound annual growth rate (CAGR). In the early 2000s the growth rate picked up to about 8 percent CAGR, until 2008 when the alarm industry — for the first time in its history — actually had a decline in overall revenues and then remained flat from 2009 through 2013. Total industry revenue since rebounded to about a 6 percent CAGR with three good, solid years of growth, he said.

“Five percent is robust, everybody feels good about it…but the reason we think that we didn’t hit a higher growth rate was [due to] one segment of the market. It looked like, from what we could tell, the very large system integrators segment stayed basically flat,” Barnes said, which contributed to the decline from 8 percent growth in 2014.

Barnes also showed the growth rates for the revenue segments of installation and monitoring/service. Over the most recent 10-year period industry revenues from installation (and related services) fell to their lowest levels and reset to about the same volume they were in the mid-2000s, while RMR never slipped because ongoing installation activity was more than enough to replace attrition during that time. RMR grew 8 percent in 2015; installation revenue grew 3 percent.

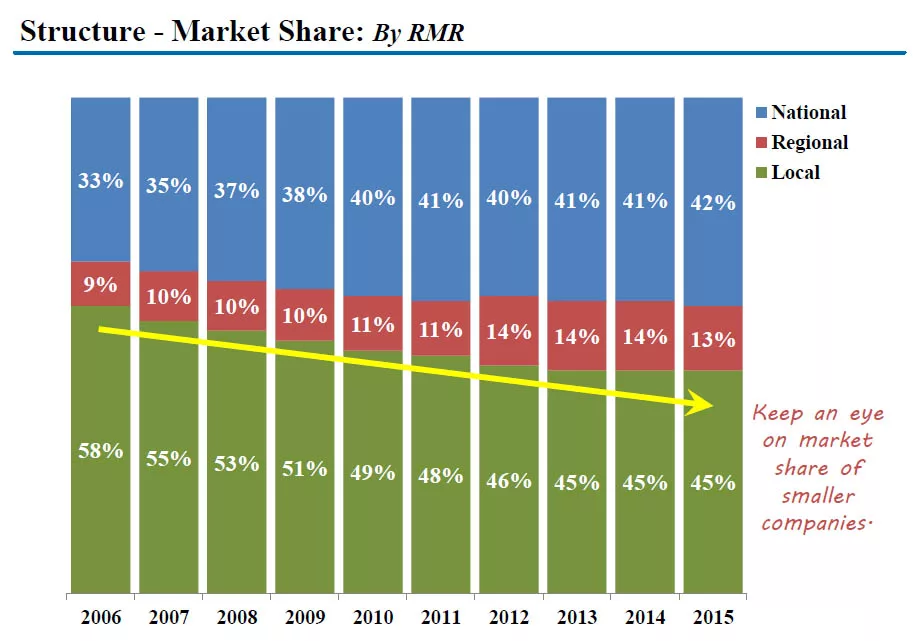

In describing the structure of the alarm industry, it was clear that not very much had changed. In terms of market share, Barnes said, the national providers including ADT (itself holding 19 percent share of RMR), Tyco, Vivint, Stanley, Monitronics, Protection 1 and the MSOs (cable and telco operators providing security) capture 42 percent share of the RMR market. “Regional” security dealers have 13 percent share of market; and 8,000 to 12,000 local companies together hold about 45 percent share of market.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

Local dealers’ share of market, which has been steady for the past three years, is down from 58 percent in 2006. “I think I’m finally willing to concede that the industry’s changing. It’s getting tougher for the small player,” Barnes said, referencing factors such as cybersecurity requisites, giant competitors, and the increasing complexity of security technology. Despite the hurdles, vast industry consolidation is not a given, and there is still plenty of room for small players to remain very competitive, he noted.

Most security professionals want to know how the MSOs (multiple system operators) are performing, yet so little information about them is available because they are not releasing it. “We’ll put a stake in the ground; this is where we think they are, plus or minus,” Barnes said. “Here in the U.S. (not counting Rogers in Canada who’s doing very well) we think there are about 1.7 million accounts today, which roughly translates to about $69 million, maybe $70 million of RMR — roughly a 5 percent share of the industry — and adding at least 60,000 accounts a month.”

Will companies such as Google or Apple someday compete in the security marketplace? “I think the answer is, probably not. They’re all looking at the industry, and Google has an investment in Nest, which is doing business with Vivint and ADT,” he said. “What they’re intrigued by is how sticky all that recurring revenue is, but they also really like the value of the services.”

However, Barnes thinks their take on it is that the security industry is too small, too complicated, too tough to execute, “and I don’t see any of them making any strategic moves any time soon,” he concluded.

What might be compelling is the vast amount of data and images that are generated by security sensors and systems. “Alarm systems are pretty good at capturing a lot of that data, and maybe that data has value. So if Google could come up with some fancy way of using that data and monetizing it in other ways, maybe they’d look at our industry and say, ‘Maybe the systems should not only be free, but maybe the monitoring should be free, too. Because we could then use all that data and package it and resell it.’ I’ll leave that for the younger generation to figure out, but I don’t think we’re going to see a big swing there,” he said.

After looking at the performance of various operating metrics, Barnes concluded that, overall, the operating environment today for the average alarm company is better than it was last year — with a lower creation cost, lower attrition, slightly higher margins, and a nice growth rate. “So it’s a good time to be in the industry,” he said.

Barnes spent time demonstrating why it is important for investors to study an alarm company’s steady-state cash flow, and he presented some examples based on the previously detailed metrics. “We think it’s a much better indicator than EBITDA because of all of the accounting measures we talked about before. One company could be capitalizing a lot of cost; the other company could be expensing them all. They’re both doing the same thing; they look completely different on an EBITDA basis, but in a steady-state they wouldn’t.”

He presented a chart that mapped two performance indicators of alarm companies over time. “If you go into an alarm company and only look at two numbers, these are the two numbers we’d look at: I’d want to know how much steady-state cash flow per dollar of RMR you’re driving, and I’d want to know your growth rate.” The takeaway is, “The average alarm company is doing as well today, generally speaking, as they’ve done in most years in the past,” he said.

With those factors as a backdrop, Barnes moved into discussing market values. “Generally speaking, the overall market characteristics are, as they have been for years and years and years, stable and liquid. There is really not a good alarm company out there that can’t put themselves up for sale and have a number of suitors.”

He said, however, that buyers are getting more demanding in knowing what they’re buying; they’re willing to pay more for certain things and a lot less for others. “So we’re seeing the spread has widened between the highest prices realized and the lowest prices. Also…transaction cycle times are longer, so if you’re thinking of putting your company up for sale you’ll want to add a month or two to the process.”

Barnes explained that there has been an increase in capital across the market, but he is unsure about how long it will last. “For those of you that borrow from the industry’s lending club, that’s a robust club…. There’s lots of money out there. It’s just a great time to be a borrower. I don’t think if you’re borrowing less than $200 million you’re feeling a whole lot of pressure on interest rates, but you’re going to feel some,” he said. The equity markets Barnes described as a bit more discriminating in what they’re buying.

In looking at valuations for both mergers and acquisitions of entire companies as well as dealer program purchases, in 2015 the industry saw $77 million of RMR (representing 5 percent of the market) traded at a weighted average multiple of 45 times RMR. Compare that with 2014, in which $46 million of RMR (5 percent of the market) was traded at a weighted average multiple of 39 times RMR. What is interesting, Barnes noted, is that there were the same number of deals in 2015 as in 2014, but the deals got bigger and were highly weighted by the Protection 1 acquisition.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!