SDM 2016 Industry Forecast: Is the Security Space Too Congested?

Results of SDM’s 2016 Industry Forecast Study, coupled with an outlook from leading integrators, show how the competitive environment will shape the security industry this year.

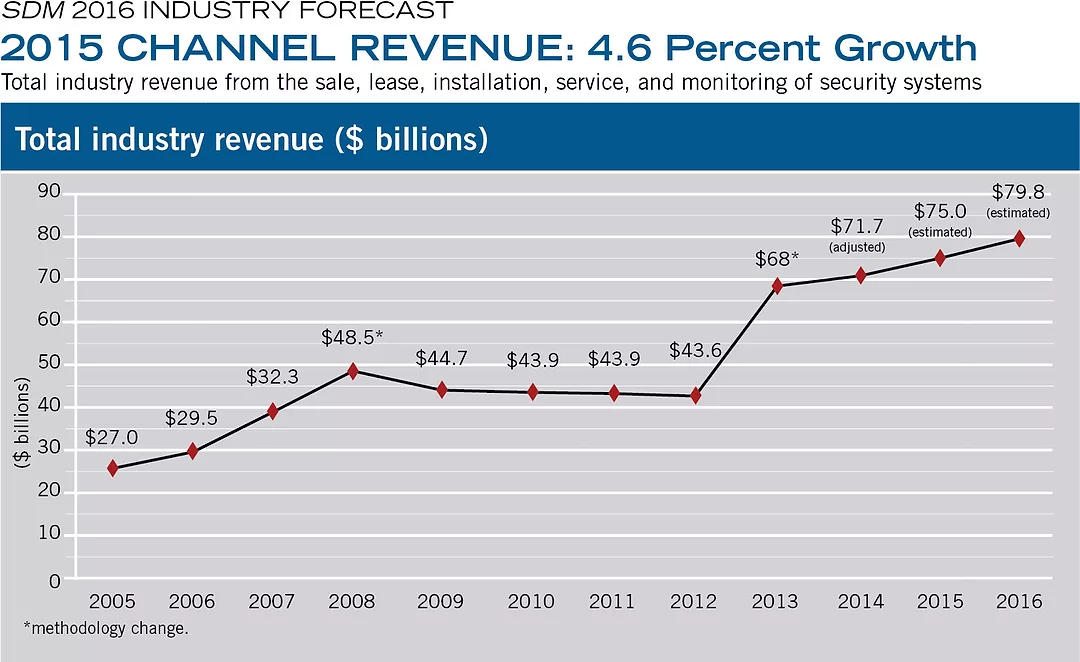

Based on SDM’s Industry Forecast Study, the total size of the security installation channel in 2015 was just under $75 billion, an increase of 4.6 percent from 2014’s $71.7 billion. Keeping the momentum going, respondents indicated they expect 2016 to offer a healthy growth rate of 6.4 percent.

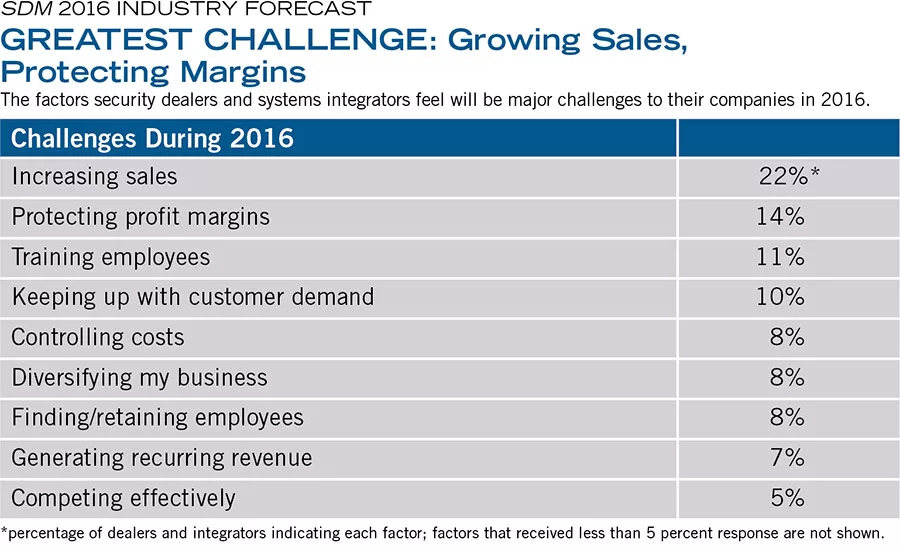

“Increasing sales” is the No. 1 challenge faced by dealers and integrators as they look out over the business landscape of 2016. The No. 2 challenge, “Protecting profit margins,” was not even among the top five last year but establishes how wary integrators have become about falling prices and rising competition.

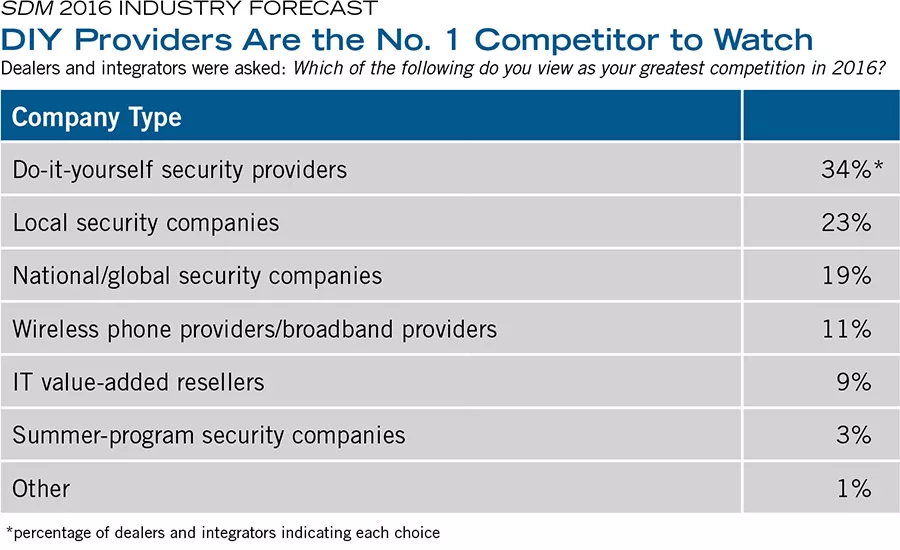

More than one-third of dealers and integrators view DIY security providers as their stiffest competition.

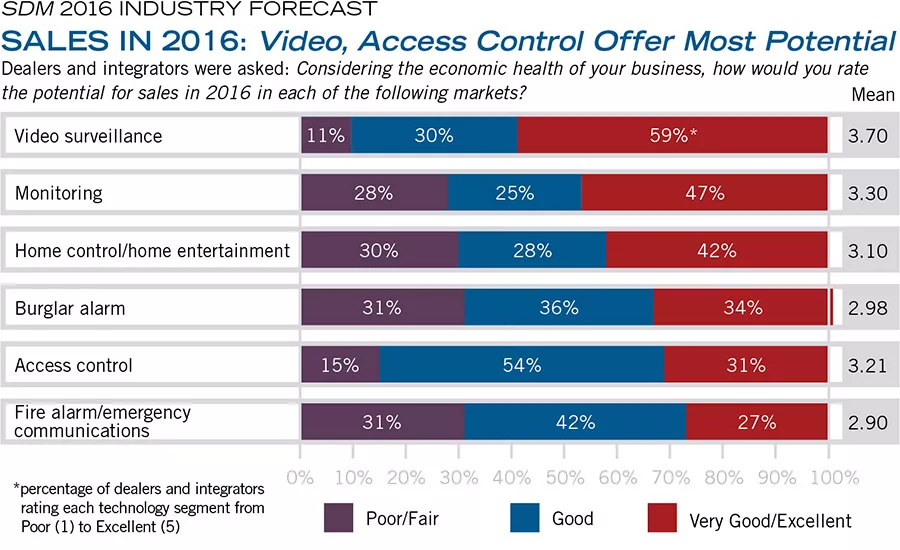

Dealers and integrators think Video Surveillance will be the most rewarding segment when it comes to producing sales in 2016. When asked to rate the potential for sales among various technology segments, they gave it an average ranking of 3.7 out of 5. The Monitoring segment — where many changes are underway in technology — closely follows, with an average rating of 3.3 out of 5.

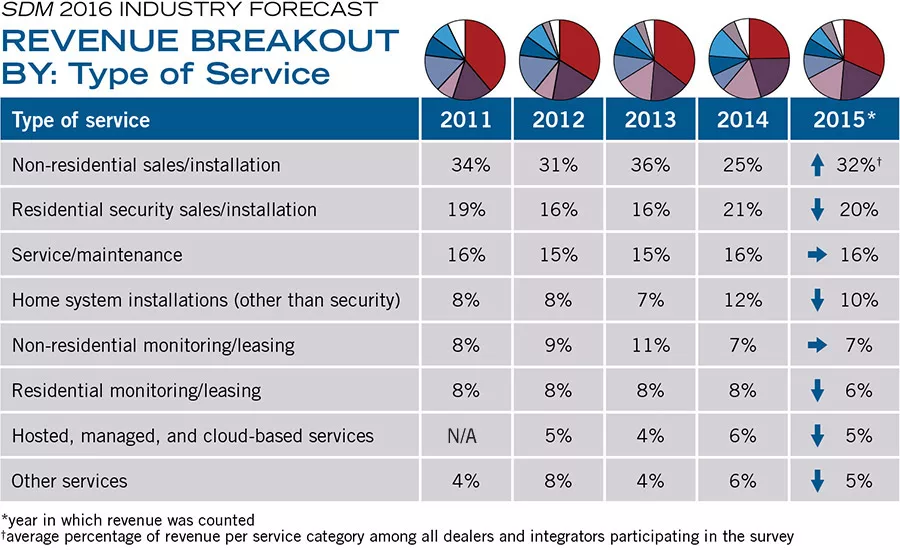

SDM’s Industry Forecast Survey tracks how dealers’ and integrators’ total revenue is distributed among types of services. Nearly one-third of their revenue came from non-residential sales/installation in 2015.

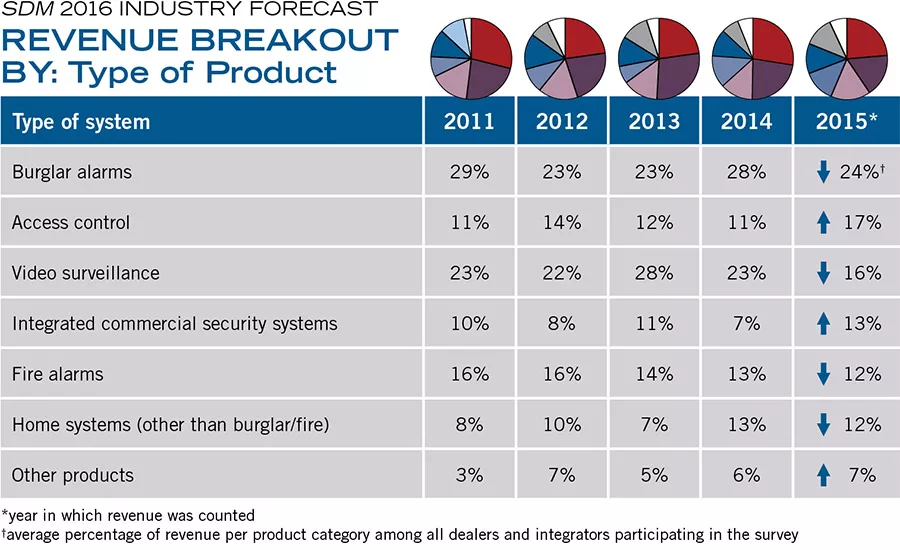

SDM’s Industry Forecast Survey tracks how dealers’ and integrators’ total revenue is distributed among types of products. The 2015 results show how the channel is diversified in its product offerings. Note the significant increase in portion of revenue from integrated commercial security systems.

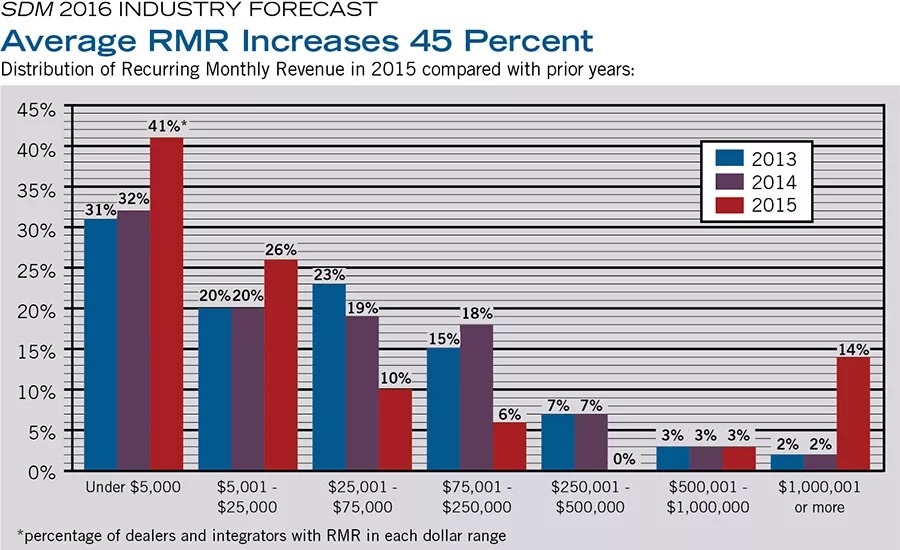

Among companies that generate recurring monthly revenue, approximately seven in 10 noted an increase in their RMR in 2015, with an average increase of 45 percent. This table shows the distribution of RMR in various dollar ranges, 2015 compared with prior years.

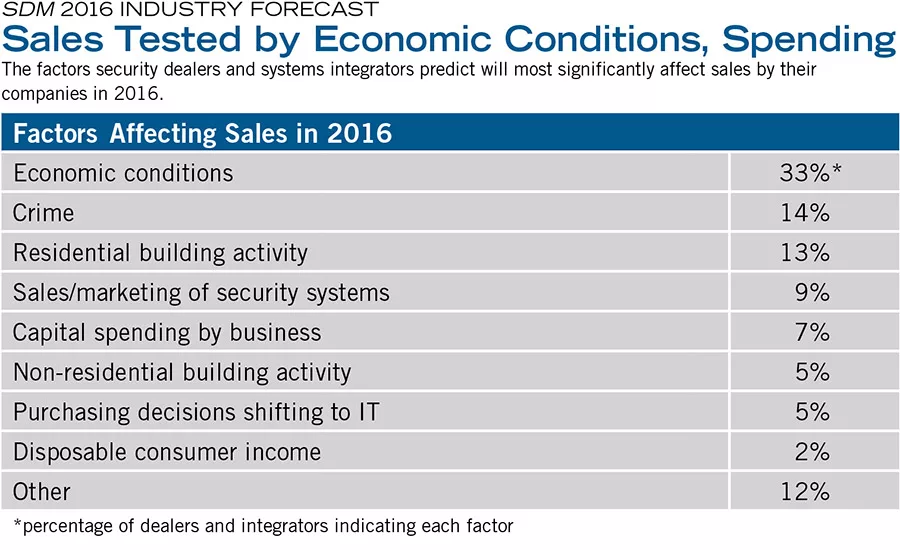

One-third of dealers and integrators expect “economic conditions” to be the top factor to significantly affect sales in 2016, with “crime” as the second-greatest factor and “residential building activity” as third, but both far behind.

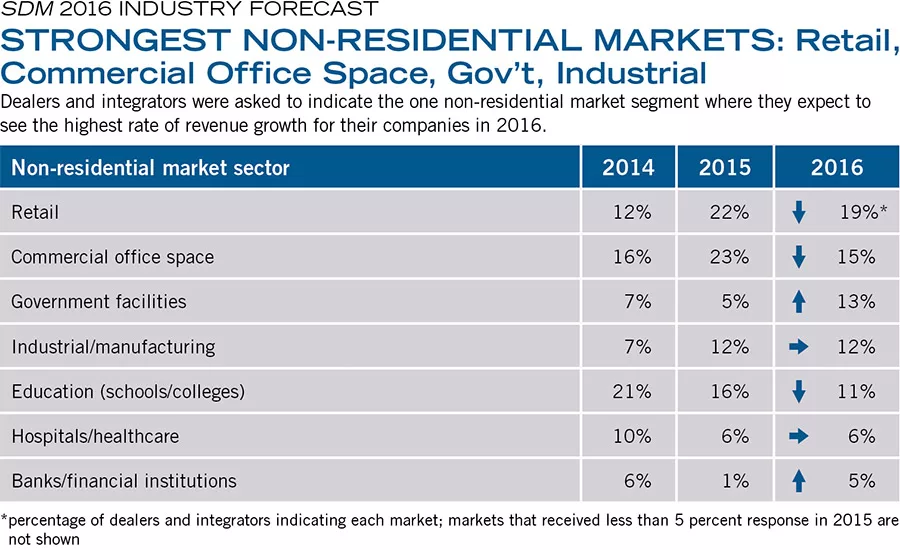

The integrator channel expects its top four most fruitful segments in 2016 to be retail, commercial office space, government facilities, and industrial. Retail, commercial office space, education, and industrial topped last year’s list.

More than six in 10 installation companies that serve the residential market rely on existing homes for both new and add-on sales. There are 117.3 million households in the United States, according to the National Multifamily Housing Council.

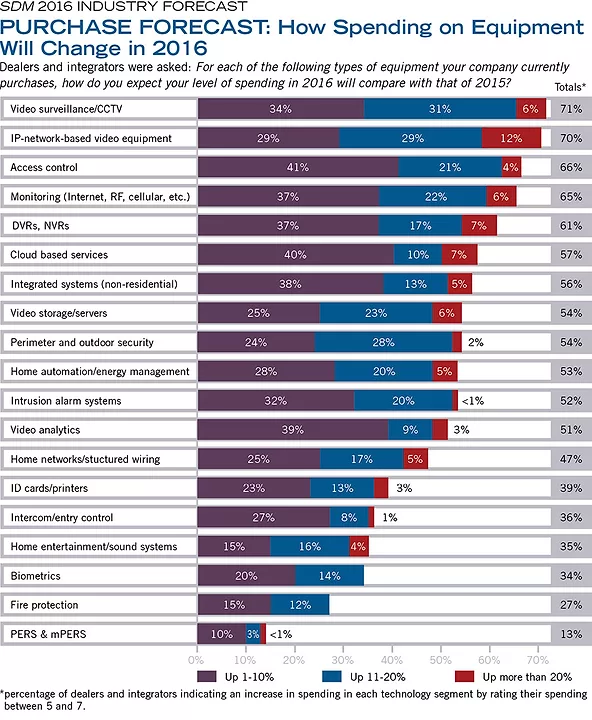

Dealers and integrators were asked to rate how their level of spending on equipment will change in 2016 compared with 2015. This table is based on a 7-point scale where 1/2 = down more than 10%; 3 = down 1% to 10%; 4 = no change; 5 = up 1% to 10%; 6/7 = up more than 10%. This table shows only the “up” responses. The top four categories with the most potential for growth in spending are video surveillance/CCTV, IP network-based video equipment, access control, and monitoring.

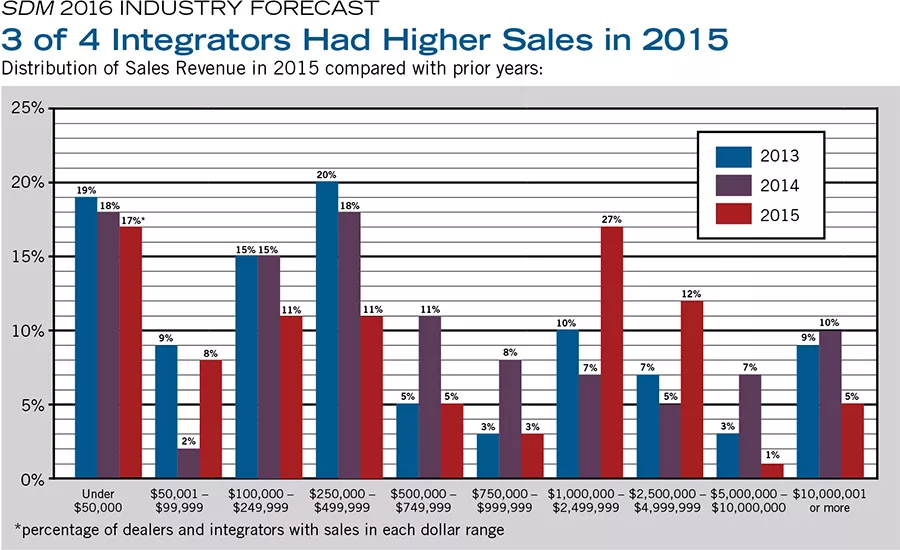

Among companies that generate new sales, approximately 75 percent noted an increase in their sales revenue in 2015, with an average increase of 69 percent. This table shows the percentage of respondents with sales in each of 10 dollar-amount ranges for 2015 and prior years. Median annual sales per company in 2015 were $500,000.

Michael T. Grady is executive vice president of Vector Security Inc., Warrendale, Pa.

Dean Belisle is a 27-year veteran of the security industry and the president of his family’s regional security and fire alarm company — ACT NOW! ALARM, in Clinton Township, Mich.

Piyush Sodha is the co-chairman and chief executive officer of Kastle Systems Int’l, Falls Church, Va.

Fasten your seat belts: 2016 is going to be a bumpy ride. It’s not because the road to improved sales, revenues and profits is pitted with potholes; rather, it’s because of the greater number drivers in the form of new competitors who are gaining speed and attempting to move ahead. Who are these competitors? Who aren’t they, ask the security professionals who participated in SDM’s 2016 Industry Forecast Study and panel.

“I think it’s probably more aggressive than it has ever been in my 33 years with the company as it relates to the competitive climate,” describes Michael Grady, executive vice president of Vector Security Inc., Warrendale, Pa. When both he and Forecast respondents were asked which companies they view as their greatest competition in 2016 (do-it-yourself security providers, local or national/global security companies, wireless phone/broadband providers, IT companies, or summer-program security companies), Grady responded that when considering both the residential and commercial markets, “I see ‘all of the above’ as being some form of competition with us on a day-to-day basis.” (See “The Panel Weighs in on Competition” on page 62.)

In a competitive environment in which more and more household names are getting into the security and connected-home business, it’s not surprising that more than one-third of dealers and integrators view DIY security providers as their stiffest competition, according to the results of the Industry Forecast Study. This is the first time that DIY competitors topped this list.

Featured on this month’s cover, Dean Belisle, president of ACT NOW! ALARM, Clinton Town-ship, Mich., sees companies such as Google and Apple, in the long run, posing the greatest threats due to their ability to create offerings that are very consumer savvy — despite whether or not these offerings are as effective as the solutions offered by the security industry.

On the commercial side, Grady says he is cautious about managed network suppliers and their ability to bundle the types of services that businesses need, including network, telecom and security. Piyush Sodha, co-chairman and chief executive officer of Kastle Systems Int’l, Falls Church, Va., agrees with Grady that the competitors to watch are those that are increasing their portfolio of services and bundling them.

Integrators who are driving on this highway crowded with competitors found that their 2015 sales performed fairly well, but that margins were squeezed. Sales increased for three-fourths of the respondents in the Industry Forecast Study. Nevertheless, respondents indicated that increasing sales and protecting profit margins top their list of major challenges in 2016.

Whereas integrators predicted one year ago that their 2015 revenue would increase, on average, about 14 percent, that prediction did not materialize. The total size of the security installation channel in 2015 was just under $75 billion, an increase of 4.6 percent from 2014’s (adjusted) $71.7 billion.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

The results for integrators on the panel were much in line with the results from the study. At ACT NOW!ALARM, for example, Belisle reports that annual revenues have grown between 3 percent and 6 percent over the past couple of years. The number of sales is up for his company, but overall sales dollars are down due to low-cost equipment and more competition.

The trend that stood out from last year’s Industry Forecast Study was how the traditional security channel is transitioning from a strictly outright sales offering to more of a security-as-a-service offering. Paralleling that trend is tighter focus on the accompanying recurring monthly revenue. Integrators explain how this shift affects their revenues in the short term.

“We used to sell the systems outright which had a much higher margin; we now have cut the margins down, but we attach a recurring revenue stream to it,” Belisle explains.

Kastle Systems also focuses on this model and will only do projects that have RMR attached to them, Piyush says, adding that approximately 75 percent of the company’s revenue is from RMR including services such as monitoring and maintenance, as well as cloud-based hosting.

Economic conditions still top the list of factors that integrators believe will have the greatest impact on sales in 2016. But based on forecasts for the housing market, for example, the economy should not dampen growth much. According to a report, “More Gains for Home Sales Despite Rising Rates” (published Nov. 24, 2015, at www.kiplinger.com), single-family housing starts are expected to rise 20 percent and multifamily starts by 4 percent; both new-home sales and existing-home sales will rise.

“The number of folks looking at homes on the market is at a high level. For new homes, it is at its highest level since 2005. The rise in employment, income and household formation is pushing up traffic,” the report states.

Nearly 7 in 10 security dealers and integrators expect 2016 to bring increased revenue compared with 2015; while only 4 percent anticipate a downturn and the remainder think it will be unchanged. Study respondents indicated they expect 2016 to provide 6.4 percent growth in annual revenues.

The Forecast Panel: 2016

MICHAEL T. GRADY is executive vice president of Vector Security Inc., Warrendale, Pa. He oversees its national accounts division and all sales for the company. Grady began his career at Vector in 1983 and was continually promoted, to his current position in 2008. Grady serves on the Loss Prevention Foundation board; is a member of the Retail Industry Leaders’ Association steering committee and is an active member of the National Retail Federation, ASIS International, national Electronic Security Association and the Central Station Alarm Association. He has completed leadership programs at Harvard Business School and The University of Pittsburgh Katz Graduate School of Business.

DEAN BELISLE is a 27-year veteran of the security industry and the president of his family’s regional security and fire alarm company — ACT NOW! ALARM, in Clinton Township, Mich. He began his career as a teenager working as an installer trainee while he attended high school and later university with the goal of attending law school. While attaining under-graduate degrees in finance and accounting, Belisle was captivated by the direction of the security industry and, upon graduation, joined the family business full-time in 1989. Belisle is NICET Level II certified as a Fire Alarm Technician. Belisle has served in many leadership roles for the Burglar & Fire Alarm Association of Michigan, most recently as its president.

PIYUSH SODHA is the co-chairman and chief executive officer of Kastle Systems Int’l, Falls Church, Va. In addition, he has been a part owner of KastleSystems since 2008. Over the past 20 years, Sodha has been the chief executive officer and chairman of several world-leading technology and telecommunication companies. Sodha is currently on the board of directors of Capital Acquisition Group, National Symphony Orchestra, and the Greater Washington Board of Trade. In addition, the Sodha Foundation, a philanthropic organization founded by Archana and Piyush Sodha, supports several community causes such as Wounded Warrior Project and Smile Train. He holds a Master of Science degree in electrical engineering from Drexel University and an M.B.A. from Wharton Business School.

The Panel Weighs in On 2015 Total Revenue

Michael Grady: We will close 2015 at about $253 million in overall revenue; 34 percent of that will come from our installation business, 28 percent will come from service, and 38 percent will come from monitoring — so pretty much of a balanced mix. Over 2014, it’s a 3 percent increase in total revenue.

We expect the same in 2016. We’re projecting to our board of directors a 3 percent increase across those three business segments, as well.

Dean Belisle: We see our annual revenues [in 2015] estimated to be right around $2.4 million. We’ve been running between a 3 percent and a 6 percent increase over the last couple of years; I would expect next year would be about the same. Our monitoring revenue is about $1.6 million out of that $2.5 million, so it’s a large part of our revenue. Our installation revenue is quite a bit smaller, comparatively.

Like anything else, margins are down. We don’t do low-cost, free systems, but our margins are pretty tight on installations. And the only area we are down in the actual sales from last year is in CCTV camera sales. We’re actually up in number of sales, but down in overall sales dollars. The cost of equipment has come down so low and the competition is up higher. We’ve also changed our model. We used to sell the systems outright which had a much higher margin; we now have cut the margins down, but we attach a recurring revenue stream to it.

Piyush Sodha: We only do projects where there’s a recurring monthly revenue; we will not do an installation, otherwise. The company is expecting to end the year at around $84 million. Twenty-five percent of the business is installation, 75 percent, approximately, is recurring monthly revenue-oriented. Year-over-year growth is approximately a little north of 7.5 percent.

The Panel Weighs in on What Keeps Them up at Night

SDM:Which one of the following factors do you think will present the biggest challenge to your company in 2016?

Michael Grady: Making sure that we keep pace with emerging technology and the ever-changing expectations of the customer.

When I do get to sleep, I have dreams of customers saying, “I saw this new product at a show,” or “I read this article today. Can we try this?” or “Is there a new technology that can provide me a solution in this area?” And believe me, that type of feedback is both important and welcome. But it is time-consuming and sometimes creates a slowdown or delay in our sales process and our ability to get back to the customer quickly with a proven solution.

So as much as we embrace emerging technology, it still keeps me up because I think as an executive team we continue to be concerned if we’re well-prepared to introduce and support those technologies.

Dean Belisle: The No. 1 thing that keeps me up at night is finding and retaining employees. In our business, we’re dinosaurs in the sense that we’re still very much hardwired systems. We like to design the larger systems that provide more detection and protection. So our staff has to be very adept at running wires, and fishing through basements and attics and walls, and things of that nature. These are difficult positions to fill in today’s market.

No. 2, all of our clients have now seen the AT&T commercials and the Comcast commercials, and they love all the bells and whistles, so it generates a lot of phone calls and a lot of interest. But it’s perceived by the consumer that it doesn’t cost anything. So once people find out the costs that go with these features, they’re not always so interested. They like to know that it’s available, and we spend a lot of time talking to clients, which is good, but it doesn’t always produce sales in the end.

On the camera side, we see with the magic of television and shows like CSI, consumer expectation is that we can do magical things with these cameras: We can see 3D images. We can look inside a van that we don’t have a view on. We can look opposite from the side a camera was facing. So sometimes the perception and the expectation that the consumer has is something that we cannot provide from a technical standpoint in the real world.

Piyush Sodha: Finding the right talent, which is fundamental to scaling the business, and I would say re-training the existing talent for all the new capabilities we are trying to push out are the heavy, heavy lift in this business. A fair bit is changing. Maybe the adoption curves on how quickly that change will be adopted by the market is not entirely clear, because when you’re doing new things you’re not sure how fast a phenomenon like the Internet of Things will take. But if your team is not in a position to ramp it, and sell it, and scale it, there’s no hope of achieving scalability. So I think our challenge is just finding very good talent, and training who we have.

The Panel Weighs in on Competition

SDM: Which of the following do you view as your greatest competition in 2016: do-it-yourself security providers; local security companies/systems integrators; national/global security companies; wireless phone providers/broadband providers; IT value-added resellers; or summer-program model security companies?

Michael Grady: Breaking it down into residential and commercial, I see “all of the above” as being some form of competition with us on a day-to-day basis. I think it’s probably more aggressive than it has ever been in my 33 years with the company as it relates to the competitive climate.

In the home, we are keeping a close eye on interactive solutions that companies like Google and Apple bring to the table. I know that that may sound a little far-fetched; maybe it doesn’t. They obviously have a huge following among the millennial generation, and our feeling is that they can enter into our business, all in, at any time. We spend a lot of time keeping our eyes and ears open to other technology sectors or companies that could create some disruption in our space, but that might not be, at this point, on our radar.

I think that we have a very attractive and successful financial model and I am confident that it’s only a matter of time before companies like these get a taste for our business and want to jump in.

On the commercial side of the business, I’m extremely cautious of managed network suppliers, especially those that are currently providing VoIP services, or infrastructure as a service, network security, and related services. I’m also concerned about these companies bundling alarm systems, video, and monitoring into a service and taking that business away from us.

As much as I feel that we are among a strong and credible group of competitors, I like to make sure that we keep an eye open for other companies possibly outside our space that are considering entrance into our marketplace.

A managed network service provider is a company providing primary and secondary networks, VoIP solutions, PCI and network security, and broadband service. We actually purchased a MNS company of that nature, whose focus is in the retail space — the IRG Group. Our two combined entities today make up Vector Intelligent Solutions.

Dean Belisle: I agree completely. I put my risk assessment as No. 1, the IT value-added reseller, No. 2 the phone providers, and No. 3, the do-it-yourself. And to some degree I’d split the residential and the commercial, as well.

I think companies like Google and Apple in the long run, in the big picture, they’re probably the largest threats. They can throw some products out there that are very consumer savvy, that have a lot of bells and whistles and are pretty to look at. They may not perform the same function that we do, but they may be perceived as providing the same function that we provide.

I think you have to break the consumer down into someone that has a high security focus and someone who has a loose, lower security focus. If you just want security because it makes you feel better and you’re not all that ramped up or concerned about it, an offering from Google or Apple is going to be fantastic.

If you’re a high security-conscious individual, I believe you’re going to seek out companies like ours who are security professionals, who have the experience and bring it to the table.

I believe the phone providers are a big threat on the residential side. But you can see in their marketing, they’ve really steered clear of the commercial. You’re far more likely to make a mistake on the commercial end than you are on the residential end, and I think that’s why they deliberately steered clear of the commercial end to date. Residential is much safer for them in regard to false alarms, client annoyance, and attrition.

I think do-it-yourself is definitely a threat. Do-it-yourself has been around forever. I think the change — the paradigm shift — is that it’s easier now. So if the client is willing to take something and put it on a tabletop, and it gives them the perceived benefit of security, and it was inexpensive and fun to play with, they’re going to give it a shot before they call us.

Piyush Sodha: We are only commercial and nonresidential focused, so I truly don’t know much of the dynamics in that world. What we see is in a commercial setting, the competition is a lot around the local providers and competing with them, and in some verticals, like our national accounts vertical, we do compete with national security firms.

An observation made by Michael earlier, which is correct, is that the people to keep your eye on are those that are increasing the portfolio of services for these large national enterprises, such as network management services, etc., and bundling those, whether it’s VoIP or others. You see three or four of these companies that actually have very good growth rates at this point in time because of bundling the telecom aspect of the services into that mix.

It’s unclear how good the margins on that business are, but that is a new breed of competition, particularly in what I would call the small retail arena. We, being very focused on large customers and commercial real estate portfolios (large buildings more than 100,000 square feet), have truly not felt too much of that. Our competition comes a lot from all the other local providers who do that at this point.

The Panel Weighs in on 2015 Recurring Monthly Revenue

SDM: Estimating what your company’s recurring monthly revenue will be on Dec. 31, 2015, how does this number compare with RMR of Dec. 31, 2014? How do you expect 2016 RMR will change compared with 2015?

Michael Grady: I’ll look at it holistically as opposed to breaking it down to residential and commercial, and say that we’re looking at a 4 percent increase, 2014 to 2015, and another 4 percent increase in 2016.

Our model has changed slightly over 2014 to 2015. We have a stronger concentration of RMR coming from the commercial sector of the business. As a result, service contracts, check and inspections, and hosted video are the types of businesses that are growing and have a much greater impact on our RMR than in the past.

The residential side of the business is still developing very nicely at a consistent pace and is providing a positive return on our RMR. The services that I spoke of a little bit earlier, including interactive or home automation has created a nice bed of recurring revenue for us.

Dean Belisle:As far as recurring revenue from 2014 and 2015, we’re up 8.8 percent. I would expect that to creep. We may hit double digits for ‘16, and it’s a lot of what Mike just explained. For us, it’s Honeywell and Total Connect services. I think the biggest factor is with the looming termination of POTS in 2017; we’re putting more and more of our clients on cellular, so that’s increasing our recurring revenue by anywhere from 20 percent to 30 percent per client. Our base residential rate is $25 a month. So if we add $10 for cellular, we’re bumping that up to about just shy of 40 percent. For 2016, I expect we’ll be double digits…somewhere between a 12 percent and 14 percent increase.

Piyush Sodha: Last year for us was a 5.5 percent increase in RMR. And I would say on the macro, I think our attrition levels held consistent with what they were in 2014. There was some price pressure, I would say, in regions that were economically challenged. The new initiatives that we took on, however, on the national enterprise level seem to have done well. If I reflect into 2016, we’re currently trying to budget around 8 percent to 8.5 percent.

The Panel Weighs in on What Factors Will Affect Sales in 2016

SDM:What is the one factor that you feel will most significantly affect sales of security systems by your company in 2016?

Michael Grady: Taking the residential market into consideration, we definitely see sales and marketing of security positively influencing our plan. We’ve introduced some new programs — do-it-yourself and monitor-it-yourself programs, home automation offerings through our Vector app will create a differentiator and some influence in 2016. Our e-commerce store, which we’ve introduced in 2015, will also get a lot of play as we move forward. So those are some of the areas of the business, coupled with an aggressive sales and marketing campaign, that we think will drive sales in 2016.

From a commercial standpoint, I think we’ll definitely be affected by the shift of the decision-making process from security and asset protection, which we’re used to dealing with, to the IT side of the world. I think that any security devices at all, that are migrating onto the network, are becoming the responsibility or the ownership of the IT departments. As a result, we are finding ourselves bringing on additional hybrid sales individuals that are going to know the network, as well as know the conventional alarm/video side of the business.

Dean Belisle: We’re a smaller company and a great deal of our work is based on referrals. So crime is a big factor in the driving force of our growth. I’d pair that up with both nonresidential and residential building activity. As we all know, when someone puts a building up for the first time, they’re far more likely to put a security system in than they are five years down the road. So those three factors are big.

I would even throw terrorism in, in the sense that when people are nervous, uncertain and scared, they want security. They want that sense of peace of mind. And it may be more of a subconscious decision, but I think it’s a factor that’s coupled with the others. It jumps right up to the top.

Piyush Sodha: The variables that seem to be at the most macro level are regional economic conditions. Commercial businesses, and the commercial real estate is a big function tied to examples that I shared earlier where Silicon Valley is having a boom, while oil companies are having a hard time in the southern part of the country. So the regional economics is the big variable.

We do work in multifamily, so I guess it could bleed over, but construction cycles are pretty important to us in terms of what happens in the marketplace. I think the awareness of just physical security will be very high in people’s minds, and I think those companies that are very intelligent about how to package that into some good solutions — particularly in major metropolitan areas — will most probably make good headway.

The Panel Weighs in on New Products & Services

SDM:What, if any, new revenue generating services or products did your company add this year?

Michael Grady:The most recent service we introduced that is generating a buzz is our e-commerce site. We’re giving the customer the ability to shop online for an alarm system. That’s new for us and somewhat outside our culture compared to the way we’ve delivered in the past. If a residential customer had taken the opportunity to ask us what we’re doing differently, we’d have to say that you can shop for and design your system online.

The second is our residential hosted video solution. That has created a positive value-add to our residential customers throughout our market in 2015. And we believe that it’s going to continue to develop as well in 2016.

In the commercial market we are generating new revenue through our device monitoring and management services offerings. As security and video systems continue to migrate onto the network, it is important to manage them like other IT infrastructure.

Dean Belisle:Two words: hosted services. Our philosophy has become — we no longer want to sell any system independently; there should be a recurring revenue stream attached to it.

In 2015, we took every product line we have and made it a hosted service. We already had it with the remote services for the alarm system; we started promoting that more and more. We attached it to every system we installed in 2015. So every client that has a security system has the hosted services for remote connect to their security system.

Every camera system we’ve done in 2015 is attached to a hosted video stream. We’re doing a lot of the service and extended service and maintaining that link to their camera systems for them — making their lives easier — and it’s the same way with access control. One of the biggest hurdles we have had in access control was the client having to maintain a computer, a database, the software, the firmware, the upgrades, and the backups. By hosting it, we’ve taken that burden off of them and done it ourselves, and the acceptance rate has been basically 99 percent. Everybody loved it and we only have a few people who don’t like this approach.

Piyush Sodha:Revenue-impacting wise, I would say our hosted video has been the needle mover in terms of just the impact it had in 2015. Along with that, we are very hopeful that this new platform that we call KastlePresence, which includes a mobile credential, is our initial indication as we have soft-sold that for a couple of months, and the interest has been very strong. We launch it officially the first week in January and we will see the results and go from there. I think that’s a big shift for us and where we sense there’s a lot of excitement.

To these new things there’s always an educational cycle, because people have been used to buying it one way or doing it one way, so there’s always that burden of teaching the industry, and we culturally enjoy doing that.

The Panel Weighs in on Sectors for Growth in 2016

SDM:What market sectors do you expect to have the most success with in 2016?

Michael Grady:In the residential market we’re going to continue to focus on developing our home automation offering. We think that’s where the greatest amount of growth is coming from.

Geographically, in addition to our East Coast footprint, we’ll be branching out into Louisiana, Mississippi, and Texas, through a recent acquisition of a company by the name of Pelican Security Network that has branch offices in Dallas, and in Baton Rouge and Shreveport, La.

From a commercial standpoint, we’re going to continue our concentration on the retail vertical. That’s where we’ve found the greatest amount of success from the national account and VIS group. Within the branch footprints, the medical industry and the educational fields have been rewarding for us, as well.

And geographically, we’re continuing to see impressive growth in the Canadian market, notably the provinces of Ontario, British Columbia and Quebec. Our strategy in 2016 is to continue to aggressively market within those specific areas of the country.

Dean Belisle: As far as geography goes, we’ll stay right here in our metro Detroit market.

As far as growing the business next year, probably the two biggest markets we’re going to see is going to be new construction — provided what Janet Yellen does with the interest rates may affect that somewhat. But if things continue where they are we’ll see new construction increases to both residential and commercial. Southeast Michigan is fairly unique because we’ve had zero construction for so long that any upturn is a big upturn for us.

And I see CCTV and hosted video being our biggest market for growth. We adopted IP video about five years ago. We went 100 percent IP video about a year-and-a-half ago. We find we’ve got a competitive advantage because we’ve got a very low, attractive price point and by marrying it with the RMR, it lets us bring that price point down. So we typically win any price battle. We’ve got the expertise to provide quality equipment. With the hosted application now, we make sure they’re online all the time. It’s always working, so they’re happy with the results.

Residentially, there’s been an explosion. Three years ago we probably would get one call every three months for a residential camera system. Today, we’re probably getting about one every day; half of our calls for camera systems are residential today.

PIyush Sodha: The verticals where we see some higher activity will be multifamily development in major metropolitan areas and the education vertical. I think we continue to believe that there is a different focus that large, professional services firms are putting on how they’re managing multi-location opportunities. So we are also investing fairly heavily to see how we do in that. What that means is sales professionals, support organization, all of that to back up the investment we have made technologically in that area. Now we’re starting to launch in that area.

An example would be law firms with 10 offices in the country or accounting firms with five offices in the country. Those are the three things that come to mind in terms of where we are finding an opportunity to spike the food a little bit.

Dean Belisle: The only thing I was going to add is we’re looking at changing our software provider and the new software provider has a cloud version, a hosted version, so I’ve been doing a lot of investigating. If you’d have asked me two months, I was dead against the cloud. I liked it for its potential down the road; I just didn’t think it was ready for prime time yet.

Then I read a book about a month ago which completely changed my mind on it. The author provided an illustration comparing the cloud situation to what we had for power at the time that Edison basically developed it. He explained that, at the time, if you ran a manufacturing plant you had to build it by a river. You had to put your equipment in order as to how those pulleys would provide the most power, being the machines closest to the waterwheel. Then when Edison developed the power plant you could put a generator in it, so you no longer had to build your plant near a river. You could build it wherever you wanted to and create your own power, and you had to hire engineers to run that power plant. Then basically they mass-produced it. They delivered it over a public network so to speak, and you could pay pennies for a kilowatt as opposed to having to maintain your own generator with your own engineers. You could just buy it as a service.

So the author took us forward 100 years and described exactly what we’re seeing today. Right now all these large companies, including our own, we have our own servers or server farms in-house. You have your own IT people which were the engineers 100 years ago. Going forward, the cloud service releases all that. You can buy it for pennies on the dollar. You can have much more computing power. It’ll always be current and you don’t need your own IT people to perform those services any longer. It’s all a fee for service. I think that’s the next step and it’s going to change everything across the board, in ways we can’t even imagine. I don’t see it as a threat and I’m not sure if it’s an opportunity either. It’s an unknown at this point, but it’s certainly a real factor.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!