Strong & Balanced

To view the full table (in PDF format) of the SDM 100, click on the link at the bottom of the article.

When the floodgates of demand for security finally opened in 2004, the industry’s largest companies – acting as a barometer of the health of the industry – were ready to market and sell, closing out that year with 9 percent overall growth in gross revenue. It was a stunning success following the SDM 100’s meager 2 percent growth during 2003.

Last year, the industry’s largest firms — ranked here on SDM Magazine’s 16th annual SDM 100 – performed exceptionally well, illustrating that the market is strong and balanced, and that it provided ample opportunities in most segments.

The objective of the SDM 100 is to measure consumer dollars captured by electronic security service providers. The majority of SDM 100 firms offer sales, installation, service, and monitoring. (A very few are considered non-traditional alarm companies in that they provide sales and installation only or monitoring only.)

Collectively, the 2005 revenue for this group increased by 4 percent to $6.7 billion. However, the showing of individual companies is much more telling of their performance. (No. 1, ADT Security Services, at 2.6 percent growth, under-performed compared with many of its peers and, as such, skewed overall growth rate.)

For example, among companies with which two years of revenue could be compared, 89 percent improved their revenues, while only 10 percent decreased and 1 percent was unchanged. Individually, this is the best performance by SDM 100 companies since 1997.

Further, 40 of the 100 firms achieved double-digit growth in 2005. (View performance data in the table that begins on page 60.)

Security executives described the 2005 market in terms that ranged from stable to outstanding. Even residential got a boost in 2005, although primarily through bundled systems rather than stand-alone burglar alarm systems.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

“Security system sales were improved in 2005 versus 2004 in every key market segment: residential, small business, commercial and integrated systems,†stated ASG Security, Beltsville, Md., which moved up from No. 22 to No. 16 this year. “Residential systems sales were extremely bountiful due to an exceptionally active real estate market. Commercial sales continued to be strong in the areas of access control systems and CCTV, in particular. Fire system sales remained steady and tracked with new construction growth in 2005.

“We experienced very good growth in the area of very large and integrated systems in the public and government sector with project wins like RFK Stadium (Home of the Washington Nationals) and Ft. Meade Army Base,†ASG went on. The firm acquired five security companies and opened new branch operations. But just as important, it more than doubled its organic residential sales and increased commercial sales revenue by nearly 30 percent.

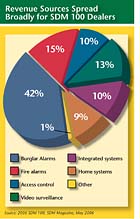

Firms on this exclusive report are ranked by their total gross revenue from security system sales/installation, service, leasing, and monitoring. They are also re-ranked by other indicators, such as recurring monthly revenue (RMR), and residential and commercial installations.

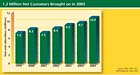

ASG, which operates a central station and increased its account base by nearly 14,000 subscribers, is indicative of many others that benefited from above-average growth in recurring monthly revenue. The SDM 100, which many people outside of the industry identify with as the installation and monitoring segment of the industry, added 1.2 million subscribers and improved RMR by a significant 11 percent in 2005 over 2004. Dealers noted that the additional recurring revenue from remote video monitoring services has started to be counted, especially as video surveillance remains the hottest item among all product categories.

But as these traditional security dealers delve into higher-end commercial markets, there they meet the systems integrators – both parties seem to be crossing boundaries these days.

“We feel the market remains strong and have noticed an increased interest in CCTV and biometric readers,†notes Sonitrol Tri-County of Farmington Hills, Mich., No. 79. “We are seeing increased competition from building control companies, like Siemens and Johnson Controls, who are offering access control, CCTV and intrusion detection as part of a complete package for a company’s building automation system.â€

While there continues to be some blurring of what was once considered two distinct industries, there is no doubt that the SDM 100 will remain a dominant market force for the remainder of 2006 and beyond – especially as monitoring services take on a more important role in society.

Watch for the June issue for SDM’s Up-and-Comers in Security – ranking the next tier of security firms just following the SDM 100!

Editor’s Note:

Questions about the SDM 100 must be sent in writing: SDM Magazine, Attn. Editor, BNP Media, 1050 IL Route 83, Suite 200, Bensenville, IL 60106. Questions and comments also may be faxed to the Editor at (248) 502-1031, or e-mailed to stepanekl@bnpmedia.com.

How to Purchase the SDM 100 Directory

Wouldn’t it be useful to have more information about each of the 100 firms ranked here? The 2006 SDM 100 Directory includes contact names, mailing addresses, telephone numbers, Web site URLs, branch office locations, product buyer names, installation data, revenue sources, and more. The SDM 100 Directory comes in Microsoft Excel format. To order the SDM 100 Directory, visit www.sdmmag.com and search under “Resources” for “Industry Research,” or contact Heidi Fusaro @ 630-694-4026 or by e-mail to fusaroh@bnpmedia.com.Side bar: a guide to reading the SDM 100

The 2006 SDM 100 ranks U.S. companies that provide electronic security systems and services to both residential and non-residential customers. This ranking is based on information either provided to or estimated by SDM. Ranked companies were asked to submit either an audited or reviewed financial statement, or a copy of their income tax return showing total gross receipts for the stated period. A vast majority of the firms ranked are privately held.

The main table, which begins on page 60, ranks 100 firms by their 2005 total gross revenue. The firm with the highest revenue is ranked as No. 1, and so on. For each of the 100 companies, the following information is provided, from left to right:

- Current year rank, which is based on total 2005 gross revenues. (If two firms have identical revenues, before rounding, then the number of subscribers is the second determining factor for ranking.)

- Previous year rank. If the firm was not previously ranked, then no number appears in this column.

- Company name, as used in the marketplace, and headquarters location.

- Total gross revenue in millions of dollars. This number represents total revenue in calendar-year or (the company’s) fiscal-year 2005 from security system sales/installation, service, leasing, and monitoring. An e following the revenue indicates it is an SDM estimate.

- Percentage of growth or descent from 2004 to 2005, where applicable.

- Number of subscribers (recurring-billable customers) that each firm counted at year-end 2005.

- Amount of recurring monthly revenue (RMR) as reported to or estimated by SDM. This figure reflects RMR on Dec. 31, 2005.

- Number of system installations (units) in 2005, residential.

- Number of system installations (units) in 2005, non-residential.

- Number of full-time employees.

- Number of business locations, including headquarters location.

To find a firm by name, use the alphabetical index on this page.

Notes:

No. 1 – ADT Security Services Inc.’s subscribers and RMR are estimated by SDM.No. 4 – HSM Security was SDM’s 2005 Dealer of the Year.

No. 6 – Vector Security Inc. was SDM’s 2003 Dealer of the Year.

No. 8 – Guardian Protection Services Inc. was SDM’s 1999 Dealer of the Year.

No. 11 – Bay Alarm Company was SDM’s 1998 Dealer of the Year.

No. 20 – CPI Security Systems Inc. was SDM’s 2000 Dealer of the Year.

No. 24 – Mountain Alarm was SDM’s 1996 Dealer of the Year.

No. 25 – Safeguard Security and Communications Inc. was SDM’s 2002 Dealer of the Year.

No. 31 – Kimberlite Corp., doing business as Sonitrol of NW Los Angeles/Ventura Co., Sonitrol of Bakersfield, Sonitrol of Fresno, Sonitrol of Modesto, Sonitrol of Stockton, Sonitrol of Oakland, Sonitrol of So. Alameda Co., Sonitrol of Berkeley/Richmond, Sonitrol of Contra Costa Co., Sonitrol of San Francisco, Sonitrol of Napa/Solano Cos., Sonitrol of Marin/Sonoma Cos.

No. 33 – Matrix Security Group Inc. also does business as SafeGuard Security in North and South Carolina. All figures are for Matrix and SafeGuard combined.

No. 34 – Approximately 15 percent of First Alarm’s revenue stems from its Security and Patrol Div., as it directly relates to alarm company activity. Total company revenue is $25.92 million.

No. 39 – SDM’s 2001 Dealer of the Year. The consolidated revenues of Trans-American Security Services (the parent holding company of Trans-Alarm and Automated Entrance Products) for 2005 is $15,864,234. The $10,970,248 of revenues reported for the SDM 100 represents the sum of revenues received from alarm and monitoring services. The remaining are revenues from integrated systems and related services and will be reported on SDM’s 2006 Top Systems Integrators Report.

No. 41 – Supreme Security Systems Inc.’s number of subscribers is estimated. Due to a computer conversion, total subscriber count is not available.

No. 52 – Doyle Security Systems Inc. was SDM’s 1997 Dealer of the Year.

No. 56 – Koorsen Fire & Security Inc. does not include fire alarm sales and service. Total company revenue is $17.97 million.

No. 64 – Custom Alarm was SDM’s 1995 Dealer of the Year.

No. 76 – Security Equipment Inc.’s total 2005 revenue is $14.49 million, of which $6.1 million represents the alarm and monitoring business segment and $14.5 million represents the integrated systems business segment and will be reported on SDM’s 2006 Top Systems Integrators Report

Links

- SDM100 Tables

- SDM100 Tables

- SDM100 Tables

- SDM100 Tables

- SDM100 Tables

- SDM100 Tables

- Laura E. Stepanek

- Laura E. Stepanek

- Laura E. Stepanek

- Heidi Fusaro

- Heidi Fusaro

- Heidi Fusaro

- Table: Alphabetical Index to Companies

- Table: Alphabetical Index to Companies

- Table: Alphabetical Index to Companies

- Table: Alphabetical Index to Companies

- Table: Alphabetical Index to Companies

- Table: Alphabetical Index to Companies

- Table: Rank by Recurring Monthly Revenue

- Table: Rank by Recurring Monthly Revenue

- Table: Rank by Recurring Monthly Revenue

- Table: Rank by Recurring Monthly Revenue

- Table: Rank by Recurring Monthly Revenue

- Table: Rank by Recurring Monthly Revenue

- Table: Rank by Residential Installation Revenue

- Table: Rank by Residential Installation Revenue

- Table: Rank by Residential Installation Revenue

- Table: Rank by Residential Installation Revenue

- Table: Rank by Residential Installation Revenue

- Table: Rank by Residential Installation Revenue

- The 15th Annual SDM 100

- The 15th Annual SDM 100

- The 15th Annual SDM 100

- The 14th Annual SDM100

- The 14th Annual SDM100

- The 14th Annual SDM100

- The 13th Annual SDM100

- The 13th Annual SDM100

- The 13th Annual SDM100

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!