2016 SDM 100: Home Run

The 2016 SDM 100, a group of the top security companies ranked by RMR, continues to knock the cover off the ball when it comes to selling into both residential and non-residential markets, providing hosted and managed services, and monitoring.

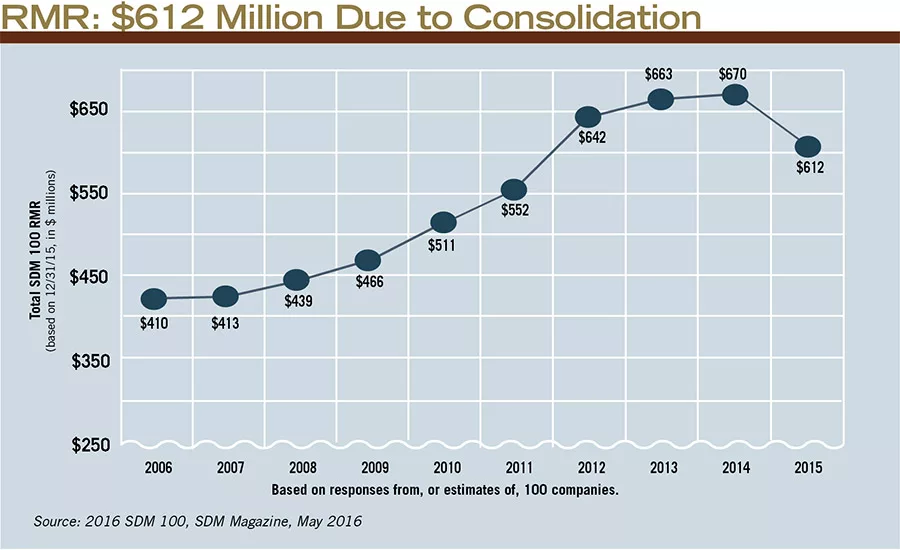

Eighty-four of the 100 companies ranked on the SDM 100 experienced RMR growth in 2015; however, because of major shifts in the ranking due to numerous acquisitions last year, total RMR dropped from $670.1 million to $612.5 million. Among the top 10 companies ranked in 2015, only six are ranked again in 2016 — missing are Protection 1, ASG Security, Diebold, and Stanley (the last not ranked due to a lack of publicly available information). With these companies removed from the calculation, the average rate of 2015 RMR growth was 10 percent.

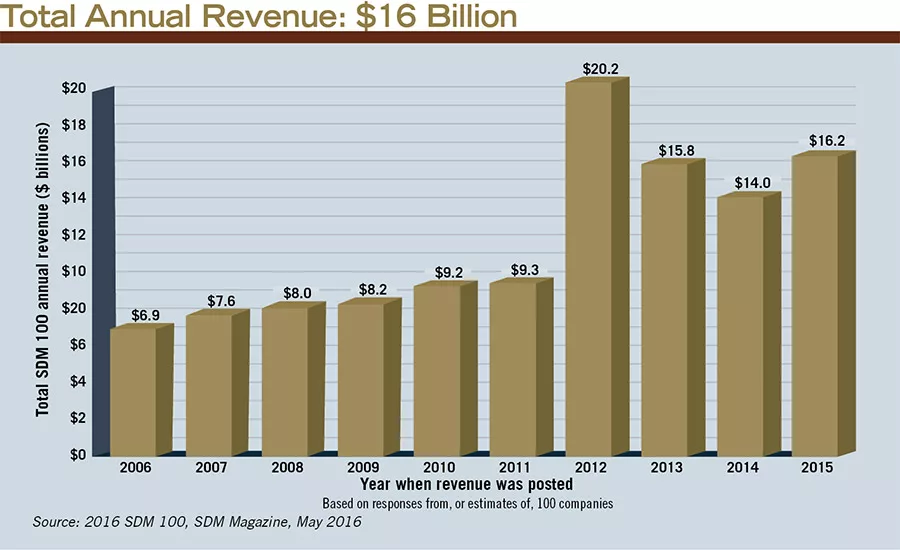

Total annual revenue for the SDM 100 companies was $16.2 billion in 2015, amidst many significant changes on this year’s report, including the removal of Protection 1 and ASG Security, as they were acquired by Apollo Global Management; the removal of Diebold Security, as it was acquired by Securitas; and the omission of Stanley Convergent Security Solutions due to lack of publicly available financial data. Both Protection 1 and ASG effectively will become part of ADT when Apollo’s acquisition of ADT is finalized.

2016 SDM 100 Rankings

In 2015 we celebrated the 25th anniversary of the SDM 100 and honored eight companies for being ranked on the first SDM 100 Report in 1991 and all of the reports thereafter. (The eight security companies are ADT, AFA Protective Systems, Alarm Detection Systems, American Alarm & Communications, Bay Alarm Company, Guardian Alarm Co., Guardian Protection Services, and Per Mar Security Services.)

One year later, we are observing a shake-up in the SDM 100 clubhouse. Among the top 10 companies, four were or will be (when finalized) part of an acquisition. The biggest change of ownership: In May 2015, funds managed by affiliates of Apollo Global Management LLC purchased Protection 1 (last year ranked No. 6) and ASG Security (last year ranked No. 10), which it merged with P1. Then in February 2016, Apollo purchased ADT and announced plans to merge it with Protection 1.

“The combined company will be a market leader with a powerful brand and scale resulting in an enhanced overall customer experience,” says Timothy J. Whall, who is president and CEO of Protection 1 and will be the CEO of the combined business following the closing of the transaction expected in June 2016. He remarked that Protection 1’s “robust commercial presence will speed ADT’s expansion into the commercial sector….”

Another major transaction was Securitas’ acquisition for approximately $350 million of Diebold Inc.’s North America-based electronic security business, announced in October 2015 and completed in February 2016. Diebold Security last year ranked No. 7 on $14.2 million RMR on Dec. 31, 2014. The new Securitas Electronic Security will be led by Tony Byerly, president, and will report to the 2017 SDM 100.

As if that weren’t enough change, Johnson Controls and Tyco entered into a definitive merger agreement under which Johnson Controls will combine with Tyco, and will together provide building products and technology, integrated solutions and energy storage, the companies say. However, because this announcement occurred in January 2016 and is not yet complete, both Johnson Controls and Tyco Integrated Security are ranked on the SDM 100 this year.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

The companies that were acquired (plus Stanley Convergent Security Solutions, which is not ranked here due to unavailability of financial data for the integration division) contributed approximately $108 million toward the SDM 100’s total RMR last year. Because these entities are not ranked this year due to their acquisitive circumstances, the result on RMR and subscriber numbers was negative. Total SDM 100 subscribers fell from 14.3 million to 12.6 million, and RMR dropped from $670.1 million to $612.5 million in the 2016 SDM 100, due to the removal of Protection 1, ASG Security, Diebold Security and Stanley Convergent.

However, this is not indicative of the performance of the SDM 100 group of companies last year. In fact, when removing those companies that were involved in acquisitions from the calculation, the average rate of RMR growth between 2014 and 2015 among the remaining security dealers is a significant 10 percent, following a 3.8 percent hike the previous year. Further, 84 of the 100 companies ranked on the SDM 100 reported improved RMR in 2015.

Because only six of the top 10 companies ranked in 2015 are ranked again in 2016, this caused a significant shift in rank for those beneath them. Guardian Protection Services, for example, rose from No. 9 to No. 6; and Interface Security went from No. 12 to No. 7. In addition, ranked for the first time or returning after an absence are: Safe Home Security Inc., Johnson Controls, Red Hawk Fire & Security, AMP Security, Universal Protection Security Systems, and several others.

The majority of SDM 100 companies expressed that their sales and financial performance were outstanding in 2015; some even said it was record-setting.

“Our National Accounts team continues to knock the cover off the ball exceeding budgeted performance in sales bookings, installation revenue, service and monitoring,” describes No. 5, Vector Security. “Our organic residential growth continues to build. We have taken the momentum from the 2014 residential initiative and spring-boarded into 2015; increasing ARPU (average revenue per unit) by 26 percent and driving to an adoption rate for interactive services at 83 percent for our branch business and 87 percent from our authorized dealer.

“We continue to struggle with our Dealer Division as competitive pressures from other dealer programs have driven up payment multiples to numbers we feel are not sustainable. As a result, we have pulled back in this area, which does impact our unit and RMR growth, but we feel is strategically the right position for Vector Security,” the company notes.

EMC Security, ranked No. 36 with just under $1 million in RMR, says its best growth in 2015 was in new construction projects, especially in residential sectors. “Existing customers continue to drop phone lines [and] upgrade to cellular and connected services,” the company reports.

“The market was strong — we had our best year ever,” recounts Mountain Alarm, ranked No. 32. “Fire alarm systems were the strongest part of our business, followed by our DIY business.”

A considerable number of SDM 100 dealers mentioned the competitive pressure they are under. For example, “[It] continues to get more difficult with the emerging cable companies,” says Security Force, ranked No. 40. “Cable companies and DIY entrants continue to chip away at market share,” says Ackerman Security Systems, No. 19.

“Competition remains high,” says No. 6, Guardian Protection Services. “We continue to try and increase market penetration through expanded product offerings and services. Our chain account business, as well as our authorized dealer network, continues to grow. We also continue to see gains in our new construction business with new housing starts and expansion of our network of builder partners.”

Not all of the dealers were as equally impressed with market conditions generally or the residential markets in particular. “The market vacillated between steady and declining performance in 2015. Residential was generally down the entire year while commercial exhibited sine wave activity,” says Supreme Security Systems, ranked No. 51.

SDM 100: 2015 Performance Statistics

| 2011 | 2012 | 2013 | 2014 | 2015 | |

| Total recurring monthly revenue | $552.3 mil | $641.9 mil | $663.0 mil | $670.1 mil | $612.5 mil* |

| Total subscribers | 13.3 mil | 18.4 mil | 14.6 mil | 14.3 mil | 12.6 mil† |

| Total annual revenue | $9.3 bil | $20.2 bil | $15.8 bil | $14.0 bil | $16.2 bil** |

| Total residential sales revenue | $170.1 mil | $171.9 mil | $184.7 mil | $139.5 mil | $136.2 mil†† |

| Total non-residential sales revenue | $852.5 mil | $947.2 mil | $714.7 mil | $1.2 bil†† | $898.0 mil†† |

| Business locations operated | 995 | 992 | 1,113 | 1,146 | 1,022 |

| Full time employees | 53,219 | 55,950 | 56,115 | 65,542 | 51,161*** |

| Part time employees | 1,037 | 1,950 | 4,846 | 604 | 6,010 |

| Acquisitions | 60 | 87 | 81 | 51 | 43 |

| Accounts gained | 34,242 | 79,269 | 125,688 | 142,863 | 51,130 |

Source: 2016 SDM 100, SDM Magazine, May 2016

The table, above, presents aggregate figures for the SDM 100 group of companies, which are ranked by their recurring monthly revenue (RMR) — an industry standard of valuation of a security installation/monitoring business. Most of the SDM 100 companies are privately held. Submitting RMR is required for ranking; other figures are not required but mostly provided. Most companies — but not all — also reported their total annual revenue, number of subscribers, installation revenues, and employees. Therefore, one should exercise caution in using this information to extrapolate industry totals or to benchmark. Note that some figures — such as total annual revenue, subscribers, and residential and non-residential sales revenue — fluctuate from year to year due to both acquisitions and inconsistent reporting by the ranked companies. For example, four of the top 10 companies that were ranked in 2015 are not ranked in 2016 due to being acquired or (in the case of Stanley Convergent Security Solutions), unavailability of public data.

* Total monthly recurring revenue, based on RMR of Dec. 31, 2015. Based on responses or estimates from 100 companies.

† Based on responses from or estimates of 96 companies. Not included: Kastle Systems Int’l; SSD Alarm Systems / Kern Security & Fire / Alpha Alarm & McNeill Security; VTI Security.

** Total annual (2015) revenue from electronic security system sales, installation, service, leasing, monitoring, and sales of subscriber accounts, as reported to or estimated by SDM. Based on responses from or estimates of 100 companies.

†† Based on responses from or estimates of 85 companies. Note: Some companies either did not choose to report this figure or did not have sales/installation revenue to report in one of the categories.

Not included in Residential Sales Revenue are: ADT; Tyco Integrated Security; Monitronics International; CPI Security Systems Inc.; Guardian Alarm Company; Kastle Systems International; Electric Guard Dog; SafeTouch; RLC Security Inc.; SSD Alarm Systems / Kern Security & Fire / Alpha Alarm & McNeill Security; Redwire / Sonitrol of Tallahassee, Bay, NW FL, EC FL; World Wide Security & GC Alarm Inc.; Alarmco Inc.; Universal Protection Security Systems; VTI Security.

Not included in Non-residential Sales Revenue are: ADT; Tyco Integrated Security; Monitronics International; CPI Security Systems Inc.; Guardian Alarm Company; Kastle Systems International; Electric Guard Dog; SafeTouch; RLC Security Inc.; SSD Alarm Systems / Kern Security & Fire / Alpha Alarm & McNeill Security; Redwire / Sonitrol of Tallahassee, Bay, NW FL, EC FL; World Wide Security & GC Alarm Inc.; Alarmco Inc.; Universal Protection Security Systems; VTI Security.

*** Based on responses from or estimates of 99 companies. Not included: SSD Alarm Systems / Kern Security & Fire / Alpha Alarm & McNeill Security.

SDM 100: Its Purpose & Approach

The SDM 100 has been published since 1991. Its primary objective is to measure consumer dollars gained by alarm companies, in order to present an account of the size of the market captured by the 100 largest security providers. SDM 100 firms are ranked by their recurring monthly revenue. RMR is the revenue associated with the contractual agreement between a security company and its subscriber — derived from customer billing for services such as monitoring, contracted service/system maintenance, security-as-a-service/managed/cloud solutions, and leasing of security systems — and is typically the basis for valuation of a security company. RMR is the language of security company executives and is meaningful in comparative analysis among industry peers. Of the 100 security dealers ranked, 35 of them earned more than $1 million in RMR in 2015.

How to Purchase the SDM 100 Directory

Wouldn’t it be useful to have more information about each of the 100 companies ranked here? The 2016 SDM 100 Directory includes contact names, mailing addresses, telephone numbers, website URLs, branch office locations, product buyer names, installation data, revenue sources, and more. The SDM 100 Directory comes in Microsoft Excel format. To order the SDM 100 Directory, contact Heidi Fusaro at (630) 518-5470 or by e-mail to fusaroh@bnpmedia.com.

Prediction for 2016 Revenue: Very Strong

*percentage of SDM 100 companies, based on 91 responses

More than eight of 10 (84 percent) SDM 100 companies predict that their revenue will improve in 2016 compared with 2015. Only 1 percent expects it to decline. Source: 2016 SDM 100, SDM Magazine, May 2016

SDM 100 Profit Margins

*percentage of SDM 100 companies, based on 89 responses

Fewer SDM 100 companies reported increased profits in 2015 — just 45 percent compared with 48 percent in 2014 and 53 percent in 2013. Among businesses that improved, their average rate of increase was 20 percent higher net profit in 2015 compared with 2014. Slightly more than one-third of security companies (34 percent) had no change in net profit year-over-year. Source: 2016 SDM 100, SDM Magazine, May 2016

SDM 100 Revenue Segmented by Product Categories

*includes badging systems, PERS, perimeter security/gates, IT hardware/software and other

Security companies derive their total revenue from a wide variety of product segments, including the single most sizable — burglar alarm systems, which comprised an average of 32 percent of security companies’ revenue in 2015, followed by integrated-technology systems for commercial customers (systems comprised of two or more types of products) representing 20 percent of total annual revenue. Source: 2016 SDM 100, SDM Magazine, May 2016

SDM 100 Revenue Segmented by Service Categories

Security companies derive their revenue from a wide variety of categories of service, including the most sizable — monitoring — which comprised an average of 47 percent of SDM 100 companies’ revenue in 2015. The second greatest source of revenue from services in 2015 was sales/installation, at an average of 32 percent of total annual revenue. Source: 2016 SDM 100, SDM Magazine, May 2016

Composition of a Security Staff

Sales and marketing jobs, installation, technical service, and customer service present the best opportunities for employment among SDM 100 companies. This chart shows the average percentage of each position within an SDM 100 company’s total employee base. Source: 2016 SDM 100, SDM Magazine, May 2016

A Look at Economies & Diseconomies of Scale Among Security Alarm Businesses

By Michael Barnes

Do larger security alarm companies have an advantage? This is an important question, and one with far-reaching implications. If the answer is “yes” then there is good reason to believe that the market could decidedly move toward consolidation, and potentially very quickly. If “no” then the market will likely remain highly fragmented and players of all sizes can, and will, have success.

This is also a timely question, with very large telecom multi-system operators (MSOs) now in the industry and gaining traction. The publication of the 26th annual SDM 100 reminds us how truly large the gap is between the big and small.

As you will see in the SDM 100 tables on pages 67-80, in terms of RMR ADT is 1,717 times larger than the 100th security company, and more than 26,000 times larger than a company with $10,000 in RMR. It is also worth noting that in terms of overall heft, most of the aforementioned MSOs make ADT look small.

As an advisor and consultant to the industry supporting acquisitions and raising capital, Barnes Associates was lucky that about 20 years ago a number of people suggested we could be a good clearinghouse for benchmarking data along standardized operating metrics. This program has been great for defining the performance envelope and trends. Here is what the data indicates relative to size (an indication that has not materially changed over time), across the four highest level metrics.

Not surprisingly, larger companies generally yield higher margins on the RMR and related revenues. Monitoring, for example, is a study in economies of scale. But, thank your highly skilled wholesale monitoring companies for substantially leveling the field. Smaller companies can outsource their monitoring at amazingly competitive costs, with the gap appearing to narrow. On balance, however, the nod goes to the larger player, and this relatively large differential is the basis on which many argue that “bigger is better.”

However, the other three metrics are arguably just as important, and the smaller companies tend to be the winners. On average, they originate new customers and their recurring revenues at a lower cost dynamic, and are able to achieve higher growth rates.

Additionally, they keep their customers longer. Why? First, the well-established product distribution channels allow even very small (skilled) players to match capability across most of the spectrum of system design. Second, the marketing cost advantage falls to these highly focused, local operations — in most cases. Third, smaller players are able to create a better overall customer experience, and/or better identify stickier customers, and realize lower attrition rates. In other words, diseconomies of scale. It is tougher and/or less efficient to do this at larger volumes.

Using any number of value creation analyses across these four variables, they all suggest that the playing field is actually pretty level. Both larger and smaller companies can and do generate value, with each having their relative size-related advantages.

On the surface, this suggests continued industry fragmentation. But, there are some factors to consider, which could tip the scales. First, the growth rate and customer origination cost advantage is being threatened. More of the larger players (think Vivint) are achieving amazing growth results, suggesting perhaps that the advantage was as much about a lack of large-scale marketing skill among big players than the unique capabilities of smaller ones. Second, there are hints that technology, and the evolving nature of how systems are used, may allow the scaling of a high-quality customer experience to become more manageable.

Time will tell, but for now, I suspect that the SDM 100 of next year will look a lot like it does this year — and the year(s) before that.

| Size of Company | Margin on Monitoring & Service | Gross Attrition Rate | RMR Creation Multiple | Growth Rate |

| Larger | 60%+ | 12%+ | 30x's | 8%- |

| Smaller | 50%- | 12%- | 20x's | 8%+ |

Better | Worse

About the Author

Michael Barnes is the founder of Barnes Associates Inc., an advisory and consulting firm that specializes in the security alarm industry. Barnes Associates is also the co-sponsor of the annual Barnes-Buchanan Conference. Visit www.barnesassociates.com.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!