State of the Market: Security & Monitoring 2018

Technology changes, major shifts in the market and evolving customer expectations bring a wealth of opportunity the commercial and residential security markets.

“Both on the residential and commercial side, the way we think of dealers will change within the next two to five years,” believes Joey Rao-Russell, president & CEO of Kimberlite Corp., a Sonitrol franchise.

2017 was a good year for the economy. The housing bubble has almost entirely recovered; the stock market saw record gains; and new construction was on the rise. In November, single family home building surged to a 10-year high, according to the Commerce Department, while ConstructConnect reports commercial construction enjoyed modest gains. All of these elements are highly favorable to the security industry — and manufacturers, dealers and integrators definitely felt the positive impact of these trends.

However, for dealers and integrators, the divide between a good year and a great one was largely dependent on several factors: what part of the market they sit in; how prepared they were to move quickly toward new technology and business models; how much pressure they felt from competition; and other factors, such as changing RMR models, the cloud, new monitoring trends and more.

“We had another stellar year for growth,” reports Daniel Herscovici, senior vice president and general manager for Xfinity Home, a business unit of Comcast, Philadelphia. “We are happy with the direction of business and the momentum in this industry.”

Many saw a tailwind effect from the strong advertising that companies such as Comcast, ADT and others have been pushing into the market.

“Our alarm business has continued to grow,” says J. Matthew Ladd, president, The Protection Bureau, Exton, Pa., a Security-Net integrator. “A lot of that is the way technology is becoming more user friendly and also the advertising done by some nationals that get clients interested in products and services.”

Integrators that have a mix of residential and commercial security work point to connected technology advancements and upgrades as the biggest driver on the residential side, while commercially there is a continuing trend toward both integration and security as a service offerings.

“Commercially we probably grew about 15-20 percent,” says Chris Wetzel, executive vice president and founder, Intertech CI, Pittsburgh, another Security-Net integrator who has both residential and commercial clients. “We probably saw an increase in residential of about 30 percent. “Those numbers would reflect automation and some of the other things we do in the residential market.”

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

Howard Fischman, president and owner, Knight-Watch Security Systems Inc., Middletown, N.Y., does about 60/40 commercial/residential. “Our numbers increased by 25 percent last year overall,” he says. “This year the first month’s projections are over 20 percent. We haven’t seen a downturn. From my perspective things have bounced back. Then again, we are into so many different systems we were able to meander the course.”

Joey Rao-Russell, president & CEO of Fresno, Calif.-based Kimberlite Corp. (featured on this month’s cover) describes 2017 as “a balanced year.” Kimberlite is an employee-owned independent Sonitrol franchise, with 94 percent of its business coming from commercial. “We had strong sales, but we also had some things that affected attrition as well, such as compression in the marketplace.”

One trend Rao-Russell notes is on the upswing is the movement of residential dealers coming into the small commercial space, driven both by competition and pricing pressure from MSOs and DIY players, as well as small commercial owners looking for the same connected and interactive services they now enjoy at home.

Research firm Parks Associates, Dallas, says the security industry overall experienced “modest growth” in 2017. “Parks Associates estimates that the percentage of U.S. broadband households with a security system grew less than 1 percent from the year prior — 27.1 percent in 2016 to 27.7 percent in 2017,” says Dina Abdelrazik, research analyst. However, the good news is this translates to an additional 1.3 million broadband households with security, and the bulk of the figure is attributed to professionally monitored security.

From the central station monitoring perspective, business was booming in 2017, says Sharon Elder, vice president of sales, National Monitoring Center Inc., Lake Forest, Calif. “The opportunities that presented themselves in 2017 were really amazing in opening up the market space for our dealers to be able to operate in. It provided us with this great opportunity to bring them new services that could increase their RMR, attachment rates and reduce attrition.”

Michael Marks, co-founder, Perennial Software, Chagrin Falls, Ohio, notes a similar experience. “2017 was a great year for the alarm monitoring industry. We saw significant growth throughout our customer base, large, mid-size and small security companies. The industry has been on a great run the past seven years, and 2017 was another great year.”

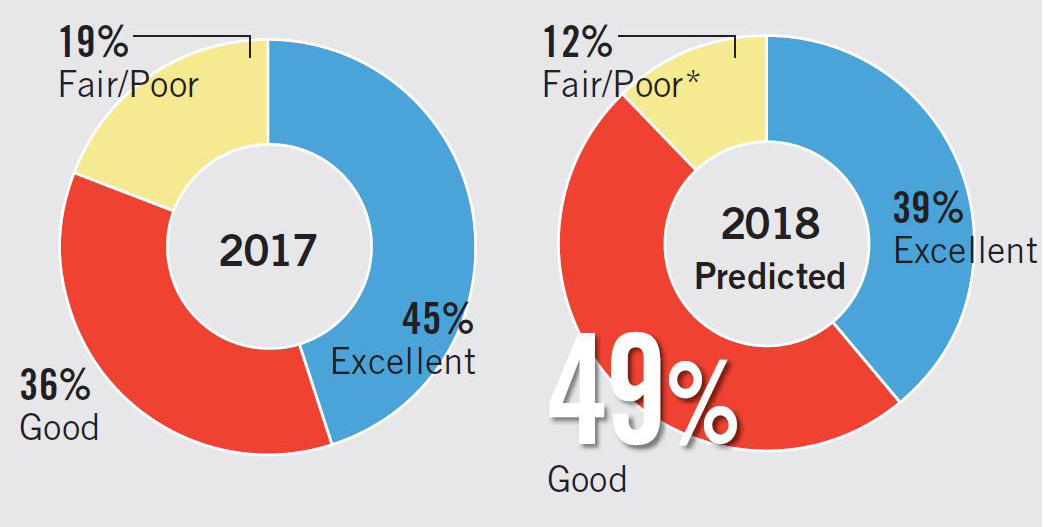

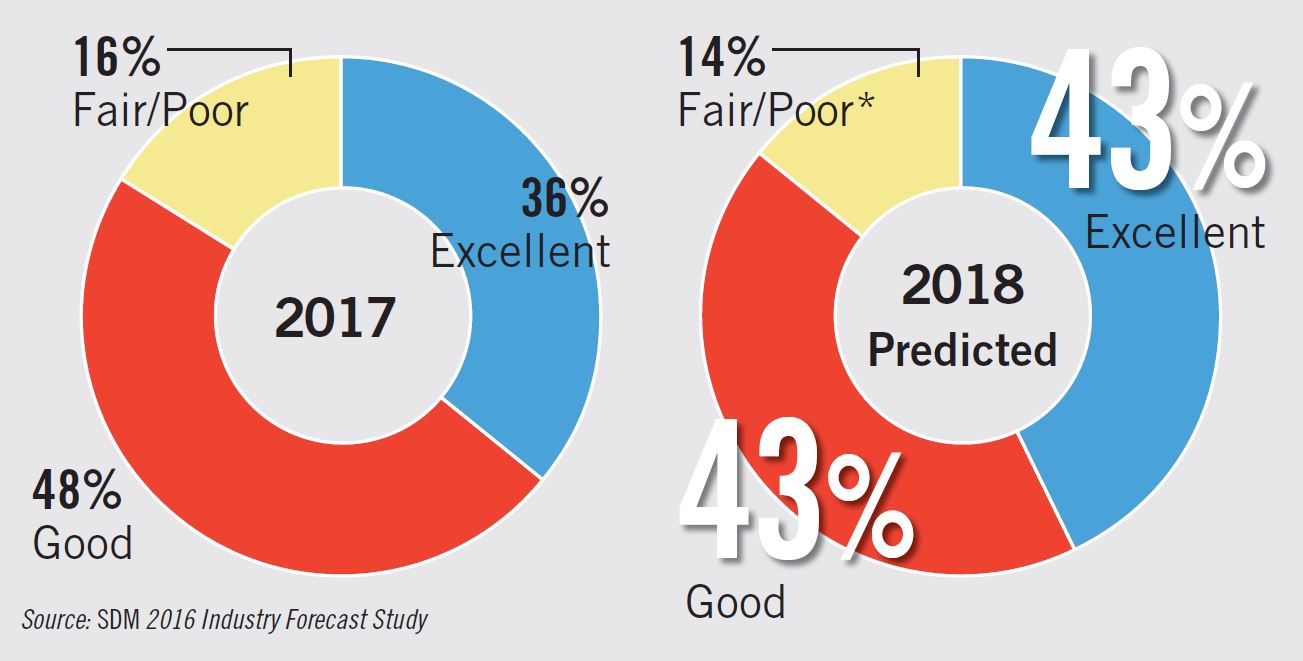

From manufacturers to security dealers and integrators and central stations, virtually everyone interviewed for this article had a good to great year, which is mirrored by the outlook of respondents to SDM’s annual survey. The 2018 Industry Forecast Study, conducted in November 2017, found that, looking at current sales in the intrusion alarm category, the number of respondents categorizing current sales as “very good/excellent” rose sharply from 30 percent to 45 percent, and overall good to excellent rose to 81 percent from 77 percent last year. (See chart, page 61.) The monitoring category saw a similar trend, with those describing it as good to excellent at 84 percent, versus 73 percent last year.

Even more are hopeful for 2018, with 86 percent predicting good to excellent sales in monitoring and 88 percent expecting the same for intrusion alarms. Read on to learn some of the trends, technologies and reasons for this optimism in the residential, commercial and monitoring spaces.

Residential Trends

There is no doubt that some of the biggest changes in the security market are happening on the residential end. From the explosion in connected services and IoT, to an influx of new entrants into the market — including DIY and MSOs — there is a lot going on.

Parks Associates estimates that 76 percent of new, professionally monitored security systems had interactive services in 2017. “A number of market developments and trends are impacting the security industry,” Abdelrazik says. “Traditional security providers are facing increased competition from point solutions such as the all-in-one cameras. While the emergence of smart home products extends the value of a security system, it also increases competition, as smart devices are often sold independently of a traditional security system. Many are self-installable.”

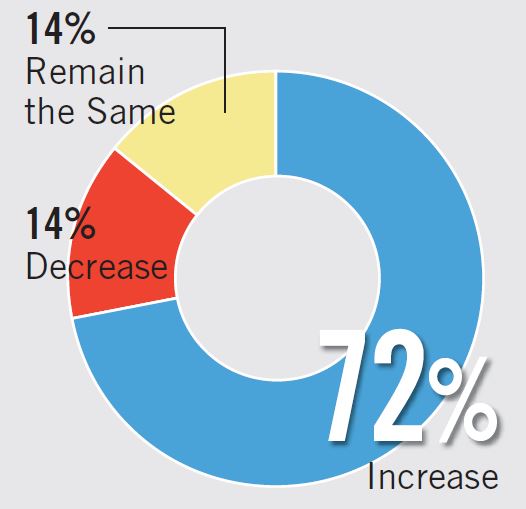

With all the new options out there, expensive monitoring fees, long-term contracts and the “traditional” way of selling an alarm system can be an uphill battle. In fact, fewer SDM Industry Forecast respondents reported that their RMR went up last year. Although still a healthy majority at 72 percent reporting an increase, 83 percent last year reported an increase, and the percent reporting a decrease doubled from 7 percent to 14 percent. (See chart on page 66.)

Those professional security dealers doing the best in this space are either the large, nationally recognized names, the new entrants, or dealers who have taken the “if you can’t beat ’em join ’em” approach to business.

“To push the needle beyond current market adoption, alternate approaches such as ad-hoc monitoring, self-install no-contract solutions and customizable solutions will need to be embraced,” Abdelrazik says.

Most of the growth in the residential intrusion market has come primarily from interactive services in recent years, says Steven E. Paley, president and CEO, Rapid Security Solutions LLC, Sarasota, Fla. “Before the development of a lot of these technologies, intrusion was probably the biggest thing. Dealers vigorously went after intrusion because of the monitoring associated with it and the RMR. … Now any person with a smartphone wants a system and to be able to manage it on the phone. It is a big driver.”

This is a reflection of what is happening in the residential market: security is becoming one piece of the larger home automation drive — instead of leading with security, many dealers have to start out with the connected, IoT features and try to sell security.

“We sell the sizzle now, not just the alarm,” Ladd says. “We are selling an integrated automation system to control lights, locks, temperature. We don’t walk in and give a keypad demo anymore. The demo is the phone or iPad. … You have to grow with the times. You can’t do it the old-fashioned way.”

Manufacturers are doing their part to help dealers do just that, offering more and more connected products, and even starting to help out with the DIY approach.

“We will be introducing a more mass residential alarm panel that will be ultra-easy to install and very cost effective,” says Jorge Hevia, senior vice president of sales and marketing, NAPCO Security Technologies, Amityville, N.Y. “The challenge right now for most dealers competing against DIY is they may be highly leveraged because they have to invest in equipment. We are trying to launch something cost effective that enables them to ease that burden.” While the product can also be self-installed it will be professionally monitored, keeping the RMR for the dealer, Hevia explains.

Another new approach dealers are finding helpful in competing in this market is by becoming “residential integrators” themselves. “Many DIY security systems and products continue to be available direct to the consumer. There is an opportunity here for dealers to show their customers the value they can provide by integrating these systems professionally,” says Keith Daum, director, product marketing, Anixter, Glenview, Ill.

“The residential side is starting to grow large for us because we are doing the integration,” Fischman says. “I actually see more shift toward home automation/smart homes. We are putting money into training for that, getting product in. The area I see the most growth in is home control, sound and home automation.”

Alice DeBiasio, vice president and general manager of residential security Americas, Honeywell Home and Building Technologies, Melville, N.Y., predicts that the rapid changes in the market aren’t going to slow down anytime soon. “With low-cost providers entering the market, we may see more commoditization of security,” she says.

For traditional residential security dealers, the shifting sands have sometimes felt more like quicksand, but more and more, the market is shaking out to separate those who are thriving on these changes, those who have made the decision to close up shop or be acquired, and those that see the more traditional small commercial space as a better fit for them.

Commercial Trends

While not nearly as volatile as the changes on the residential side, commercial security and monitoring has been going through a slow sea change of its own in recent years. Integration is nothing new, but what has changed is the way it is accomplished, and the opportunities that presents — particularly for integrators that operate in the SMB space.

“It is not brand new, but one of the biggest impacts I have seen has been the ability to take your basic access control systems and implement alarm monitoring through the system with some form of integration,” Ladd says. “I have seen a tremendous amount of improved integration on the manufacturer end. Everything is IP, and now you have the capability to send certain alarms out to a central station but also utilize the two-way capabilities of the burg panel.”

Integrating technologies enhances the prospect of predicting and preventing life safety and security events, says Steve Schmidt, program manager, UL, Northbrook, Ill. “There are a host of new market entrants focused on this integration, and it will become a disruptive force.”

The trend of residential dealers coming into the small commercial space is not lost on manufacturers, either. NAPCO has just launched a business version of its Starlink Connect, Hevia says. “The typical residential consumer is realizing they can do everything we can do, for free. Where we think there is a higher potential for RMR for dealers is in commercial. “A small business owner may be willing to pay $100 a month because it saves them a lot more than that. We can monitor a restaurant’s refrigerators to make sure they don’t lose thousands of dollars’ worth of food, or take video of the back door because businesses lose inventory that way. There are millions of small businesses across this country who are multiple-unit singular owners, and we think this is something that has a lot of value.”

And they are paying attention. Technology advancements like these are making things easier and a little less intimidating for a residential dealer to start contemplating the commercial market.

“It makes sense that they would get into small commercial,” Paley says. “A lot of these guys started 40 years ago as a family business and built up a nice RMR base. Now the pace of business and competitors are such that you aren’t going to go out and roll out RMR like you used to. Dealers who aren’t ready to sell out need to find other ways of doing things. Almost any solution today that you can provide can generate an RMR opportunity if you put your head around it.”

There has also been a shift in expectations on the commercial side, she adds. “They are more interested in user interfaces, in what we can provide, not only in security but also security as a service, help with human capital, etc. They are looking for more well-rounded services, not just a door sensor anymore.”

Rao-Russell cites the example of a Subway restaurant customer that has teenage employees working after hours. “They have a camera that sends a push notification to the owner whenever those back doors are open during the day so he can see if the employees are hiding in the back and not working,” she says. After-hours the camera serves as verification if there is a break-in. “Customers want these interactive services that help them manage their business as well as their security.”

Energy consumption is another driver on the commercial side, Fischman says. “If you can help them cut their bills down, that is what they want to hear. If you can show they are saving money in the long run, they are more open and willing to spend money on it now.” Something as simple as monitoring the lights to make sure an employee doesn’t leave and forget to turn them off overnight can make a big difference, he says.

Another trend affecting the commercial market, not just for dealers but for integrators as well, is the cloud, or security as a service (SaaS) model. “More and more people do not want to manage things for themselves,” Rao-Russell says. “Their IT people are doing too much already. This is the greatest opportunity as an industry that we have right now. There are lower installation costs on technology such as access control with a cloud-based service attached. It is a win-win all the way around.”

Almost the polar opposite of the DIY trend on the residential side, small commercial is much more interested in “do it for me,” Paley adds. “What our clients are really looking for is they want to outsource all this crap. They don’t want a piece of hardware or software; they just want to know someone is managing it for them.”

And what is pulling all these service-oriented offerings together — both on the SaaS commercial and the connected residential — is the ability of central stations to deliver on these promises.

Monitoring Trends

An increase in sensors, IoT devices and other things that provide monitoring opportunities is a vital part of the growth in the security industry. A recent report by Frost & Sullivan found that IoT is bringing about a “new era of connectivity” in both business and residential markets. The total sensors market in security and surveillance applications was worth $6.3 billion in 2016, the report states. That market is expected to nearly double to $12 billion by 2023.

Analyst Ram Ravi further notes in a press release, “Cloud networking, a revolutionary two-way interactive service delivery platform, is expected to create a technological explosion in the homes and buildings services market. This will enable [dealers and integrators] to adopt new business models to provide attractive cloud-based services through a secured network.”

Colorado Springs, Colo.-based Bold Technologies is already seeing the effects of this trend, says Rod Coles, CEO. “From our perspective the industry performed very well and grew from 2016 to 2017. A lot of people were more inclined to look at new products and contemplate or make a switch from on-premises to cloud solutions. For us personally, the last two quarters we experienced some of our best growth. Over 70 percent of our sales in the last quarter were cloud sales, up from 25 percent during the same time last year.”

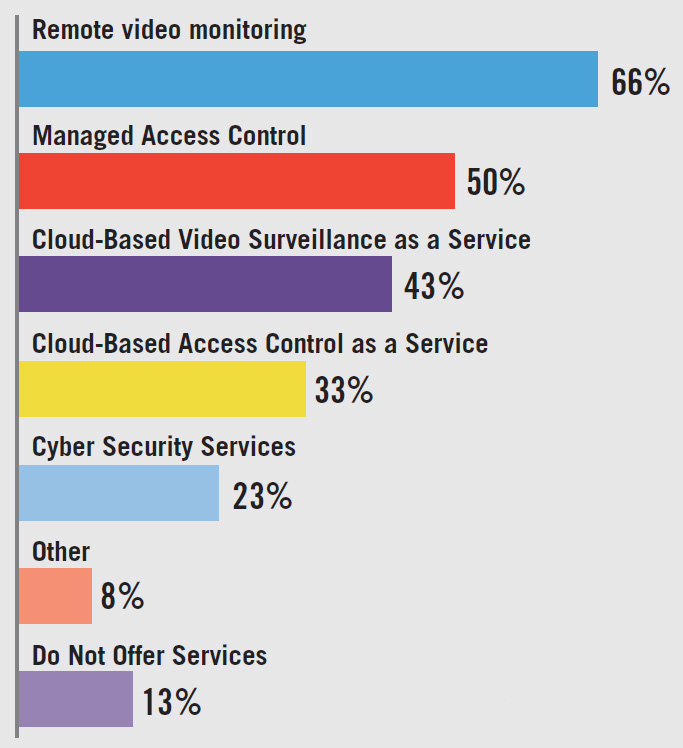

SDM Forecast respondents reported that 43 percent currently offer cloud-based video surveillance as a service, while a third offer cloud-based access control as a service. Fifty percent offer managed access control (up from 41 percent last year). Remote video monitoring topped the list at 66 percent, a trend noted by both third-party and dealer-owned central stations as well.

“Video monitoring services are growing at a faster rate than traditional monitoring services,” says Paul Garms, director of regional marketing – intrusion, Bosch Security Systems Inc., Fairport, NY. “Video analytics built into the IP camera have made video monitoring services a far more appealing option today than a few years ago. By adding further analytics in the cloud, monitoring centers are now able to deploy a more practical and affordable solution.”

This trend really opened up in 2017, Elder says. “Up until this point the challenge has been, ‘I have an Avigilon camera in the field and it is not integrated with anyone.’ In 2017 those channels opened up hugely between I-View Now and SureView. That channel takes away that problem. Both residentially and commercially … as a central station, for the first time I can really say, ‘Whatever you need in video I can totally deliver that.’”

Technology trends such as these do present some challenges, particularly for smaller, independent dealer-owned central stations. Video monitoring in particular is a whole different skillset, Paley says. For many dealers, the choice is to invest heavily in upgrading their own station, or look to third-party options that have the resources they lack.

“Today, companies that were doing their monitoring in-house are losing the ability to offer any type of video services, area of refuge, personal emergency services or all these other things that endear you to your client,” Elder says. “They need to work with a solid third-party central station in order to keep that engineering and automation at such a high level that they can compete with the ADTs of the world.”

Intertech’s Chris Wetzel is one that made this decision. “For many years we had our own central station that we maintained,” he says. “We made the decision to move those services to a third party and take advantage of a lot of what they are providing in the way of additional services and automation. It has made it easier for us to grow.”

Elder describes monitoring as a vital relationship between the dealer and the central station. “There is a tremendous amount of value and responsibility on both sides. We touch that consumer so frequently, much more than the alarm company will ever do.”

Matthew Brandon, national sales manager, AvantGuard, Ogden, Utah, is very optimistic about the future of third-party central stations. “Being in a position to say that you can monitor virtually anything that can send us a signal is the biggest opportunity for us. From GPS tracking devices to drone technology, we have the resources and technology to grow in many different directions.”

Other dealer-owned stations are boosting their own capabilities, despite some challenges.

“We are moving our receivers more to the cloud instead of the conventional rack-mounted,” Ladd reports. “This provides higher security, better communication and more enhancements to our clients.”

Rao-Russell says her company feels the pressure on the monitoring side, despite all the new technologies and services they are able to offer. “We used to just buy phone lines, a couple of stations, computers and automation software. That was an investment for 10 years. Now I have an employee in my office that just keeps track of pass-through services like AlarmNet, interactive services and third-party cloud services. The business model has definitely changed and we have to be adaptable to that.”

She says this has led to some compression on the monitoring side. “We used to get $70-$80 on monitoring. Now we can still get that but with full total connection. Even though you are still getting the same amount, it is costing more to provide that. The margin is compressing.”

Still, Rao Russell is very positive about the changes in monitoring overall. “The monitoring side is where the growth is coming from. If you look at the last five years we have had material growth in RMR. We don’t have customers accepting a 20 percent increase per year, but they are buying cloud access or camera monitoring.”

Don Young, CIO of Boca Raton, Fla.-based ADT (SDM’s 2017 Dealer of the Year) and vice president of The Monitoring Association board of directors, agrees. “As more organizations continue migrating to IP-based technologies, we feel that monitoring of non-traditional systems such as access control, video and networks will account for expanded growth.” ADT recently rolled out a cyber security monitoring offering, which is another up-and-coming trend to watch.

New entrants are also a disruptive force, Parks Associates’ Abdelrazik says. “Expensive monitoring fees and long-term contracts are cost barriers to the average consumer. Low-cost monitoring solutions such as Ring Alarm are coming to disrupt the monitoring market with $10 per month monitoring and no long-term contracts. [These types of solutions] may contribute to growth by expanding the market from the bottom by addressing price sensitivity.”

Another monitoring trend the industry is starting to grapple with that may be a factor going forward is the concept of “monitoring on demand” in the residential space. This allows a customer that wouldn’t normally be a monitored account to choose when they want monitoring — for a two-week vacation, for example — and provides a more flexible model for the consumer. However, many central stations and dealers are resistant to this idea.

It is starting to germinate, however, says Michael Chiavacci, general manager, Interlogix, Lincolnton, N.C. “Two years ago you never heard of monitoring on demand being offered. But you are hearing about it now as end users want their homes monitored while they’re on vacation or away for business. Dealers willing to supplement their traditional product offerings with some type of monitor-it-yourself or monitoring-on-demand service are likely to see an increase in this business.”

SDM asked in 2017, “How would you rate the current state of the market and the potential for sales in the intrusion (burglar) alarm market?”

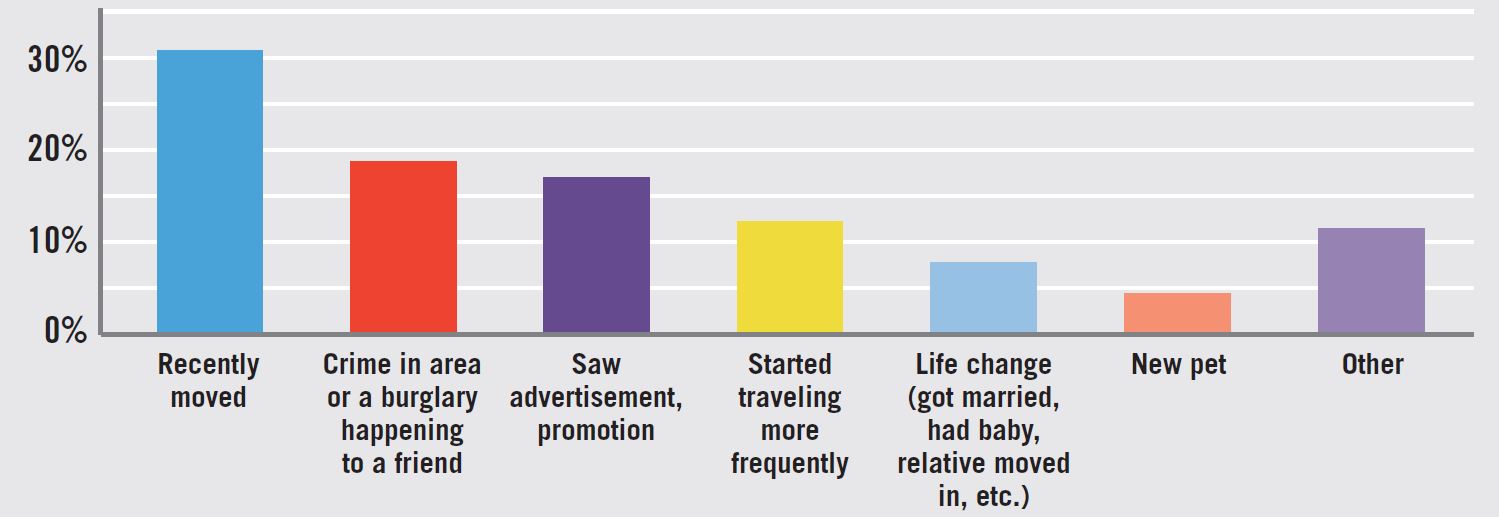

U.S. broadband households that acquired a home security system in the past year

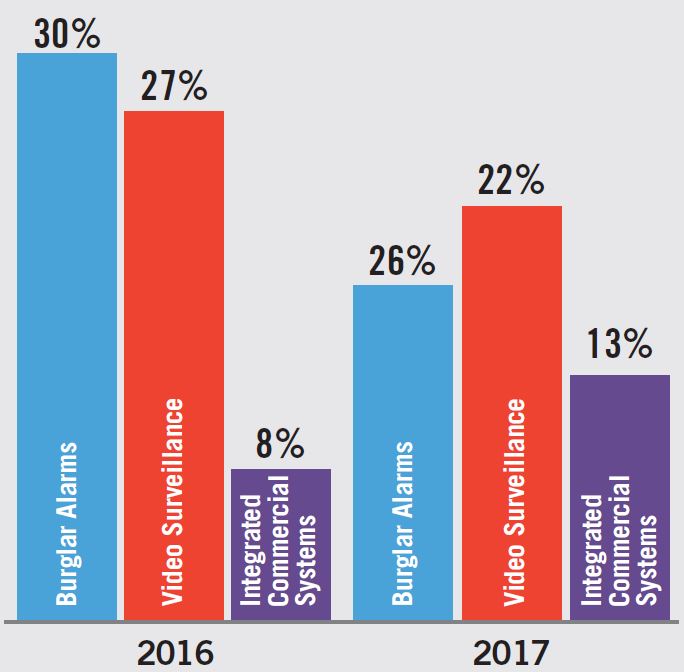

Dealers and integrators were asked which services their company offered to subscribers in 2017.

SDM asked in 2017, “How would you rate the current state of the market and the potential for sales in the monitoring market?”

SDM asked, “What percentage of revenue will have come from the following products and services?”

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!