2018 SDM 100: Security Dealers Prevail

While growth was not quite as robust as the prior year, SDM 100 dealers still managed to grow RMR by 4.2 percent last year, despite the many disruptors now present in the channel

As the security business expands and matures it is creating a more complex universe in which traditional security dealers — who have performed virtually in a silo since the dawn of the modern electronic security industry in the 1850s — now must operate. The disruptive forces swirling in their atmosphere are producing new technologies, new competitors, and even new types of customers at an accelerated rate. Despite the many changes the security channel is undergoing today, it continues to prevail precisely because of dealers’ keen awareness of the needs of their respective markets.

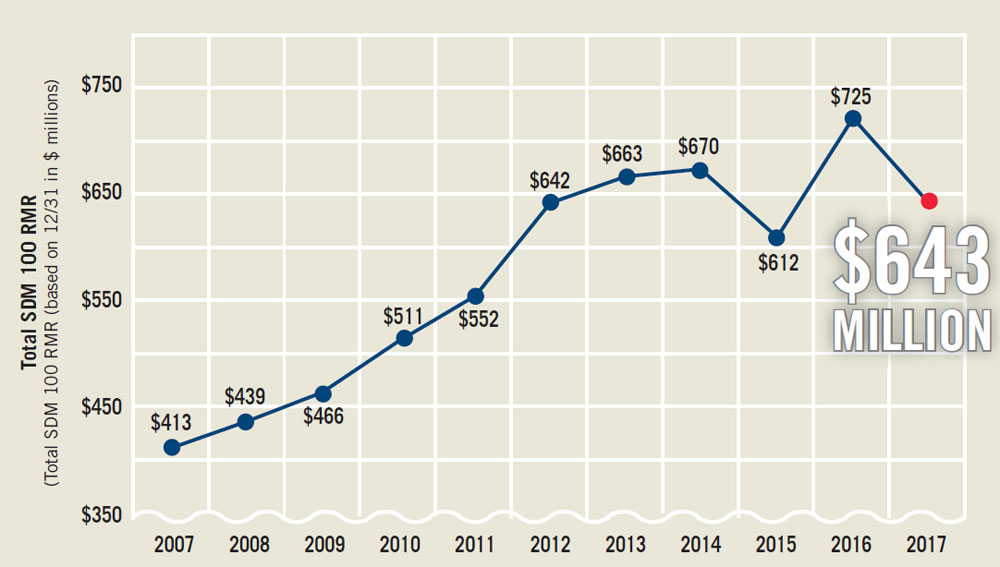

Evidence of their resilience is the 2018 SDM 100, a ranking by recurring monthly revenue (RMR) of the largest U.S. security installation and monitoring companies. Collectively, the SDM 100 security dealers grew their RMR 4.2 percent, from $618 million to $643 million last year (see chart on this page for further clarification). Among the top 100 there were 88 dealers who individually improved their RMR rate in 2017 over 2016.

“Our industry is experiencing a significant evolution as many ‘early disruptors’ to the category become more mature such as the Internet of Things, DIY, and new industry competitors,” observes No. 5-ranked Guardian Protection Services. “Rather than one particular item transforming the industry or our business, Guardian sees the collective influence of all these elements coming together to both increase the market awareness of our products and services, as well as increase our challenge of how to break through in a crowded marketplace.”

Breaking through in a crowded marketplace may prove to be too tough a challenge for some, however, as this year’s SDM 100 data and commentary offered some warning signs. While dealers gained in RMR and total annual revenue, they lost ground last year by a few other measures: Residential sales declined 2 percent, from $105 million to $103 million, and total subscribers fell 5 percent, from 13.9 million to 13.2 million. (Editor’s note: Dramatic changes from year to year often are caused by one or more large companies being added or removed from the SDM 100, or by larger companies that report a figure such as sales revenue one year but not the next; every effort is made in this report to explain and normalize such differences by removing these companies from the aggregate calculations. For example, Johnson Controls Inc., which was ranked in 2017 but not in 2018, was removed prior to performing the calculations above and elsewhere in this report, unless otherwise noted.)

In addition, 2017’s RMR growth rate of 4.2 percent was well below 2016’s RMR growth rate of 9.8 percent.

“Sales volume is still robust, but becoming much more competitive due to new entrants,” says No. 33, EMC Security. “The residential market is very price-sensitive. New and existing customers are interested in new connected services, which helps drive increases in recurring revenue. Commercial spending is up, due to new construction projects, especially in multi-family housing. ...”

EMC Security, along with several other SDM 100 companies that specialize in residential, were successful in 2017. But a significant number of other dealers experienced weakness in their residential markets.

Looking for quick answers on security topics? Try Ask SDM, our new smart AI search tool. Ask SDM →

“The residential market seems to be staying flat and we have not seen much growth, but this is what we saw in 2016 as well,” states No. 91, Fleenor Security Systems. “The commercial market is growing and expanding with many new opportunities this year and I believe it was a little better than we saw in 2016.”

Very few if any security dealers mentioned weakness in non-residential markets, even though there are many challenges in that segment, too, including the gradual shift to a services model, higher wages due to a shortage of technical labor, pressure on margins, and the continued need to keep training staff on subjects such as cyber security and emerging technologies.

When asked how they expect 2018 revenues will compare with 2017, 90 percent of security dealers on the SDM 100 predict that their revenue will improve, while 10 percent expect the same results as last year.

Charts and Graphs

A Pivotal Point in the Industry’s Progress

It is a great time to be in the security alarm industry. As the data around the SDM 100 indicates, the industry’s larger players are growing, and there is plenty of support for the rest of the industry doing equally well, across virtually all segments. Larger players, smaller players, commercial-market oriented, residential-market oriented, and a host of different business models all are showing broad-based gains. Additionally, the technologies that support this growth are improving in capability, at lower costs, and enabling a broadening array of valuable applications — all the hallmarks of a well-functioning industry with a substantial opportunity.

Underlying these favorable developments and dynamics, however, is an increasing undertone of worry among industry participants. So why the concern?

Size, Technology & Complexity

We tend to hear the concern voiced around three issues. The industry is something like three times the size it was 20 years ago. With size comes attention — particularly when what you do is highly valuable, has recurring revenues, sticky customers, utilizes evolving technologies, and employs a talented and productive labor force. The likes of Google, Amazon, Apollo, Blackstone, Johnson Controls, Comcast and Stanley are here for a reason. The industry and the opportunity are big enough to warrant their attention. The concern is that these large players bring resources and capabilities that yield competitive advantages that other participants can’t match. Or, that they alter the economics through using the industry as a tool for leveraging other aspects of their business.

Secondly is a concern around technology. The march of progress is inevitable, and arguably accelerating. These developments are likely to be materially impactful if your business uses sensing, video, processing, telecommunications, and Internet-based technologies, which of course are the cornerstones of the industry. The concern is that a player will gain a technological exclusivity around a “killer application” that others can’t match.

Lastly is the issue of complexity. Running a security alarm business never has been easy. It can be execution-sensitive, labor-intensive, with a two-part pricing model (installation fees/RMR) and a confusing accounting dynamic. It also requires capital to grow. Complicated. The concern is that with changes in the competitive landscape, a broadening of the type and nature of the products and services offered, and the pace of evolution in technology, operations have crossed over into being complex, and requiring a higher order of skill in managing their outcome.

A Consensus View?

These issues occupied a large amount of the discussion at our annual Barnes Buchanan Conference, which included a wide array of industry participants and stakeholders. An emerging consensus, one which this author shares, is that a broad range of industry participants will continue to be successful. That is, the future is not only for the large or the few. The arguments supporting this view are lengthy and nuanced, but mostly key off a couple of basic precepts.

Ultimately, bigger is not necessarily better. Smaller, highly focused operations can often achieve parity in overall performance and economics, particularly through lower attrition rates and customer origination costs. There is also evidence that many end users favor dedicated, specialty providers for security-related products and services and the expertise to select what is most appropriate. Lastly, there is no indication that any of the newer players are materially ignoring the fundamental economics of the industry in order to accomplish some unrelated objective, nor that they can or have achieved some game-changing cost advantage.

On technology, there is a continued confidence in the depth of the industry’s established and emerging manufacturers, service providers, and distribution channels to stay ahead of the curve and prevent any direct-to-end-user gaining a competitively unchallenged capability.

Somewhat surprisingly, it is the last issue that seems to be taking its toll and is likely to continue to do so. The largest consistent factor among players not succeeding in this market appears to be related to managing the associated complexity in the new environment.

It is clear that this is a pivotal point in the industry’s history. What is less clear — and there is a wide diversity of opinion — is how to best position oneself in this market and maximize the opportunity. My guess is there are a bunch of right answers. — Contributed by Michael Barnes, founder of Barnes Associates Inc., an advisory and consulting firm that specializes in the security alarm industry. Barnes Associates is also the co-sponsor of the annual Barnes-Buchanan Conference.

SDM 100: Its Purpose & Approach

The SDM 100 has been published since 1991. Its primary objective is to measure consumer dollars gained by security companies, in order to present an account of the size of the market captured by the 100 largest providers. SDM 100 firms are ranked by their recurring monthly revenue. RMR is the revenue associated with the contractual agreement between a security company and its subscriber — derived from customer billing for services such as monitoring, contracted service/system maintenance, security-as-a-service/managed/cloud solutions such as interactive services, and leasing of security systems — and is typically the basis for valuation of a security company. RMR is the language of security company executives and is meaningful in comparative analysis among industry peers. Of the 100 security dealers ranked, 38 of them earned more than $1 million in RMR in 2017.

How to Purchase the SDM 100 Directory

Wouldn’t it be useful to have more information about each of the 100 companies ranked here? The 2018 SDM 100 Directory includes contact names, mailing addresses, telephone numbers, website URLs, branch office locations, product buyer names, installation data, revenue sources, and more. The SDM 100 Directory comes in Microsoft Excel format. To order, contact Heidi Fusaro at (630) 518-5470 or by e-mail to fusaroh@bnpmedia.com.

Recurring monthly revenue (RMR) in 2017 for SDM 100 companies is down 11 percent, but this is primarily due to the un-listing of Johnson Controls Inc. (JCI) in 2018 due to a lack of publicly available financial data on its security installation and monitoring business. (Listed in 2017, Johnson Controls reported $107.4 million in RMR, which is not reflected on this year’s report.) Absent JCI, the SDM 100 grew RMR 4.2 percent. Eighty-eight of the 100 companies ranked on the SDM 100 experienced RMR expansion in 2017. Stand-out companies among the top 10 in RMR growth are: Vivint Inc.,14.9 percent; Bay Alarm Company, 9.7 percent; and CPI Security, 13.9 percent.

Source: 2018 SDM 100, SDM Magazine, May 2018

Year when revenue was posted

Based on responses from, or estimates of, 99 companies.

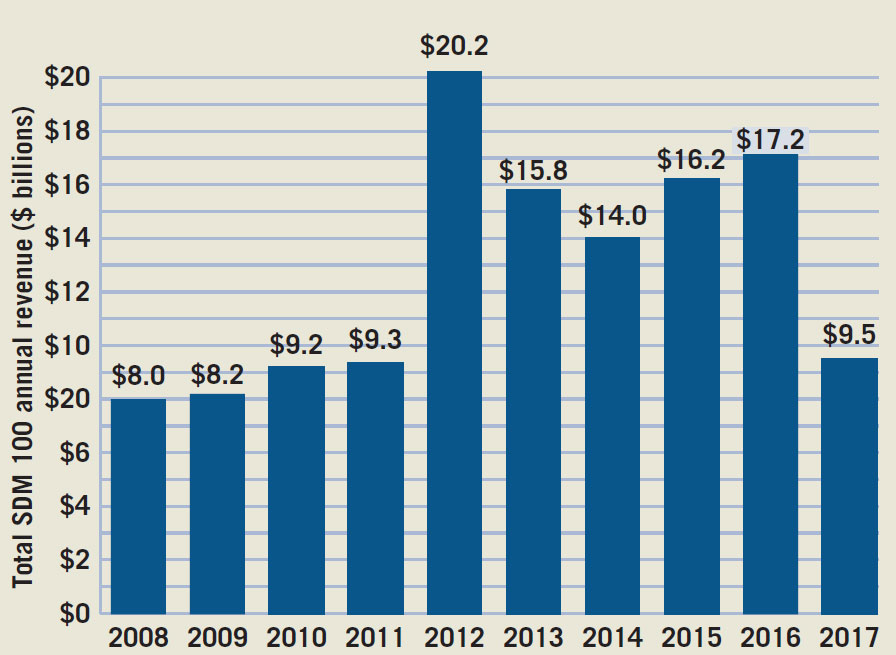

Total annual revenue for the SDM 100 companies was $9.5 billion in 2017, a 45 percent decrease compared with 2016. However, the decrease is primarily due to the un-listing of Johnson Controls in 2018 due to a lack of publicly available financial data on its security installation and monitoring business.

Source: 2018 SDM 100, SDM Magazine, May 2018

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!